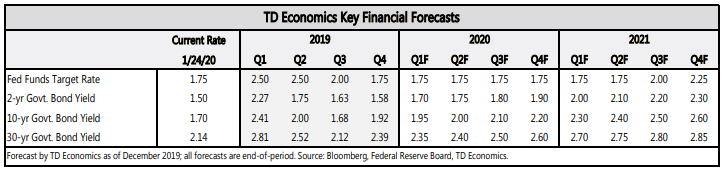

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Markets were focused on the progress of the new coronavirus in China, with few economic headlines in the U.S.. It is still early days, but it is likely the important efforts to contain the disease will crimp economic growth in China.

- Existing home sales more than recouped November’s decline in December. Unseasonably warm weather likely was a factor, but it sets up strong momentum in residential investment heading into 2020.

- Next week features the Fed meeting and our first peek at fourth quarter economic growth. The Fed is likely to leave rates on hold as it assesses the potential upside from the trade deal with China. A solid headline of around 2% growth is likely to mask softer domestic details.

All Quiet Ahead of the Fed

Markets were focused on the progress of the new coronavirus in China, with few economic headlines in the U.S. It is still very early days, with analysts looking back at the SARS outbreak in 2003 for guidance. However, the global health system is now much better prepared to contain an outbreak like this. The containment restrictions in China will hopefully help, but the disruption is likely to hold back economic growth there in the short-term.

Markets were focused on the progress of the new coronavirus in China, with few economic headlines in the U.S. It is still very early days, with analysts looking back at the SARS outbreak in 2003 for guidance. However, the global health system is now much better prepared to contain an outbreak like this. The containment restrictions in China will hopefully help, but the disruption is likely to hold back economic growth there in the short-term.

The European Central Bank left its low policy rates unchanged this week. Activity in the Euro Area appears to be stabilizing, albeit at a lower level. Christine Lagarde, the new ECB President, also set out the framework for the ECB’s first strategic review in 16 years. It will reconsider the inflation target and the tools used to achieve it. Notably it will also examine how other considerations, like climate change and environmental sustainability can be relevant to the ECB’s mandate.

Existing home sales jumped up 4% in December, more than recovering from the 1.7% decline in November. Activity was likely boosted by unseasonable warm weather in December, so we will likely see some softness in the months ahead. Overall, however, the story of 2019 was a resurgence in housing in the second half of the year (Chart 1). The main reason was rising affordability due to lower mortgage rates and accelerating income.

In fact, home sales could have been even higher if not for constrained housing supply, which is driving up prices. All in, as we outlined in our recent report, we expect existing home sales to continue to improve, but at a more subdued pace this year.

Next week will feature bigger headlines, with a Fed meeting and fourth quarter GDP data. We don’t foresee fireworks from the FOMC, which is widely expected to leave rates unchanged. This decision does not feature a forecast update, but we will be watching for the Fed’s take on the Phase 1 China trade deal. The narrative of a strong consumer and resurgent housing sector, alongside weak business investment, remains very much intact since December’s statement.

Next week will feature bigger headlines, with a Fed meeting and fourth quarter GDP data. We don’t foresee fireworks from the FOMC, which is widely expected to leave rates unchanged. This decision does not feature a forecast update, but we will be watching for the Fed’s take on the Phase 1 China trade deal. The narrative of a strong consumer and resurgent housing sector, alongside weak business investment, remains very much intact since December’s statement.

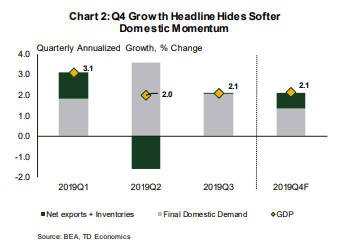

Fourth quarter economic growth is forecast to post a respectable 2.1% annualized gain on the surface. However, the details are likely to show the U.S. economy ended 2019 on a soft note. Consumer spending is tracking below 2%, and business investment is looking flat to slightly negative. Residential investment is one area expected to be quite bright, but it is relatively small. A large drop in imports is the main factor keeping growth above 2%, but that is not a positive sign for demand (Chart 2). Trade is often a trickier component to predict, so there is a bit more uncertainty than usual on the quarter’s forecast. Domestic demand should look a bit better in Q1, but overall our latest forecast calls for relatively modest growth in 2020 of around 2 percent.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.