FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Effective today, the U.S. increased tariffs to 25% on $200bn worth of Chinese imports.The threat to extend a 25% tariff to virtually all Chinese imports “shortly” remains. This comes even as the two sides continue negotiations to reach a trade deal.

- The U.S. overall trade deficit edged higher in March to $50bn, even as the bilateral goods trade deficit with China declined to a five year low.

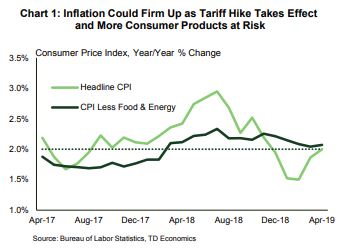

- Consumer price inflation continues to show little signs of accelerating,with both headline and core inflation around 2%. Things could change however, as tariff hikes filter through the economy.

U.S. – Tariff Talks Teeter

With few data releases, the return of U.S.-China trade tensions captured attention. Financial markets were volatile, but largely down as President Trump tweeted over the weekend that an increase to tariffs on Chinese imports would go into effect Friday. These sentiments were reiterated by other high-ranking U.S. trade officials who accused Beijing of reneging on its promises in earlier negotiations. This rhetoric threatened to derail planned high-level talks with Chinese negotiators; however the Chinese delegation only delayed the meetings rather than cancelling them.

With few data releases, the return of U.S.-China trade tensions captured attention. Financial markets were volatile, but largely down as President Trump tweeted over the weekend that an increase to tariffs on Chinese imports would go into effect Friday. These sentiments were reiterated by other high-ranking U.S. trade officials who accused Beijing of reneging on its promises in earlier negotiations. This rhetoric threatened to derail planned high-level talks with Chinese negotiators; however the Chinese delegation only delayed the meetings rather than cancelling them.

The U.S. administration officially implemented the tariff increase from 10% to 25% on approximately $200bn worth of Chinese imports on Friday. Additionally, President Trump has tweeted that he plans to levy the new 25% tariff on a further $325bn worth of Chinese goods “shortly”, a move that would cover virtually all U.S. imports from China. Even as China urged the U.S. to meet them halfway, they announced that countermeasures will be implemented, although specific details have not been revealed.

Despite the new developments, talks continued on Friday as the two sides try to salvage a deal. A sticking point for the U.S., however, is whether China will agree to implement legal changes so as to facilitate the trade deal and to make the details public. China has resisted this push, insisting that it impinges on their national sovereignty.

The new tariffs will result in a more significant drag on growth if they are sustained, impacting not only capital expenditure and consumer spending but also confidence. In a recent note, we estimate that U.S. growth could be lowered by -0.1% to -0.3% with the higher tariff. Growth could fall by as much as -0.6% if the threatened $325bn becomes a reality. The run-up in inventories witnessed in prior months partially reflected preparation by businesses for this possibility, and with additional tariffs to take effect, they are likely to pass on price increases to consumers.

The new tariffs will result in a more significant drag on growth if they are sustained, impacting not only capital expenditure and consumer spending but also confidence. In a recent note, we estimate that U.S. growth could be lowered by -0.1% to -0.3% with the higher tariff. Growth could fall by as much as -0.6% if the threatened $325bn becomes a reality. The run-up in inventories witnessed in prior months partially reflected preparation by businesses for this possibility, and with additional tariffs to take effect, they are likely to pass on price increases to consumers.

To date, inflationary pressures have been benign. Consumer prices in April rose 0.3% over the previous month and were up 2% year-on-year (Chart 1). However, the threatened escalation in tariffs could see inflationary pressures firm up. We estimate that consumer prices rose by 0.3ppts from tariffs already imposed and could rise by an additional 0.4ppts if the remaining $325bn of Chinese imports are made subject to 25% tariff (see note).

Despite the U.S.’s heavy use of tariffs to rebalance trade flows, their trade deficit edged up in March, reflecting the difficulties inherent in attempting to redirect international trade. Of note, the merchandise trade deficit with China, a special area of interest, has been declining for the past few months, and hit a five year low in March (Chart 2). This development may positively impact ongoing negotiations between the two economic powerhouses. All told, the U.S. and Chinese economies are at an important juncture. Decisions made now are likely to have significant implications for the global economic landscape in the future.

Shernette McLeod, Economist | 416-415-0413

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.