FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Pessimism dominated markets this week, as negative headlines about U.S.-China trade relations continued.

- UK PM Theresa May announced her resignation after repeated attempts to get her negotiated Brexit deal through parliament failed.The pound fell this week as markets worry about a no deal Brexit on Oct. 31st.

- Indicators from the U.S. factory sector continue to point to a weakening trend in the face of softer foreign demand and sentiment.

Trade Woes Weigh on Markets

Global markets returned to a pessimistic mood this week, focusing on negative headlines about U.S.-China trade relations. Oil prices fell sharply on the week, as rising inventories in the U.S. had markets worried that trade uncertainty is dampening demand. Measures of manufacturing confidence across various regions were also weak. Manufacturing activity in Europe and Japan continued to contract. In the U.S., the Markit gauge of manufacturing confidence also showed a further deterioration in May.

Global markets returned to a pessimistic mood this week, focusing on negative headlines about U.S.-China trade relations. Oil prices fell sharply on the week, as rising inventories in the U.S. had markets worried that trade uncertainty is dampening demand. Measures of manufacturing confidence across various regions were also weak. Manufacturing activity in Europe and Japan continued to contract. In the U.S., the Markit gauge of manufacturing confidence also showed a further deterioration in May.

To top it all off the Brexit saga came back to the fore, as Prime Minister Theresa May announced her resignation. May had been unable to get her negotiated Brexit deal through parliament. The way forward on Brexit remains unclear, and the new Conservative leader, who should be selected by the end of July, will not have a lot of time to chart a new course before the Oct 31st deadline for Britain to leave the EU. In the meantime, the cloud of uncertainty continues to hang over the UK economy, and the increased probability of a no-deal Brexit has weighed heavily on the pound over the past week.

The sour news continued with the April durable goods orders report, which showed total orders fell 2.1% in April. Nondefense capital goods orders ex-aircraft – a closely watched gauge of business capital spending – was also down in April (-0.9%). Durable goods orders are quite volatile month-to-month, but on a trend basis (the six month moving average) orders have gone sideways at best since late 2018 (Chart 1). This is consistent with the theme discussed in last week’s Bottom Line, that cracks continue to appear in the US manufacturing sector: foreign demand has cooled, and uncertainty on the trade front weighs on business sentiment and willingness to spend on new equipment.

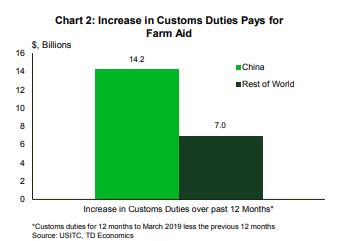

The President has recognized the impact trade conflicts are having on at least one sector of the economy. He formally announced a $16 billion aid package for farmers hurt by Chinese retaliatory tariffs on key agricultural exports from the U.S. This amount is slightly larger than last year’s aid package (around $12 billion). The combined cost of these packages more than outweighs the increase in customs duties the U.S. has collected since the Administration started ratcheting up import tariffs early in 2018 (Chart 2), erasing any fiscal benefits of the tariffs.

Amidst the headlines on ongoing trade tensions between the world’s largest economies, the minutes from the most recent FOMC meeting already seemed a bit stale. These deliberations occurred before the latest increase in the tariff rate on certain Chinese imports. The minutes showed the FOMC’s commitment to patient monetary policy, and a significant discussion on whether the recent softness in inflation is transitory, or a more persistent trend. The Committee is clearly divided on that topic, and a couple more months of data is likely to settle the debate. Inflation aside, given a building cloud of global economic uncertainty, a prolonged pause on rates seems a wise course of action.

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.