FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

• The ISM manufacturing index showed signs of easing supply chain conditions in financial news. Supplier delivery times shortened while

production, employment and new orders indexes all increased.

• This week’s payrolls report left something to be desired, but a pop in household employment and a rise in the labor force

participation rate are welcome signs of a recovery in labor supply.

• While the first glimmers of abating supply side issues have emerged, the Omicron variant threatens to undo the progress.

U.S. – Supply Issues Easing, but Omicron Looms

Volatility was the name of the game this week in financial news as markets whipsawed on news of the Omicron variant’s identification in the U.S., and Chairman Powell’s more hawkish stance. Inflation remains front and center as Chairman Powell retired the term “transitory” when describing recent price gains. That said, November’s data offered signs that supply chains challenges have begun to ease, offering some promise of inflation relief.

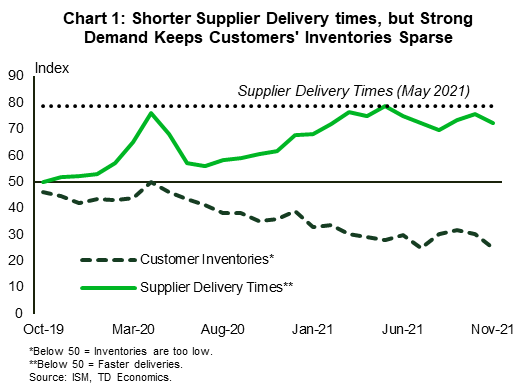

This week’s release of November’s ISM manufacturing survey gave one such signal. The report showed growth accelerating as the expansion carried on for its 18th consecutive month. The details provided further reasons for optimism. The supplier delivery times subindex remained extremely high (you have to look back to the late 1970’s to find a comparable lead time prior to the pandemic), but it pulled back for the first time in three months (Chart 1). Alone, this move doesn’t mean much, but the production, employment, and new orders indexes also all moved higher in November. An environment where production, orders, and employment growth are increasing while supplier delivery times are narrowing is a signal that some of the bottlenecks we’ve been seeing are beginning to clear.

Alas, not all of the news was good. Customer inventories continue to languish at low levels and the index pulled back on the month. This is likely a reflection of continued strong demand that has left producers trying to keep up. Indeed, this month’s vehicle sales report was a reflection of those tight conditions, as monthly sales disappointed, falling to 12.9 million units (at a seasonally adjusted annualized rate). Automotive production ticked up in October, but remains well below underlying demand, which is likely closer to 1.45 million per month. This means inventories will remain scarce for the time being.

At the same time, this week’s payrolls report showed a slowing in the pace of job growth. Markets had expected north of 500k jobs to be added to payrolls, so the 210k realized in November missed the mark.

Despite the disappointing print in the payrolls report there were several reassuring details in the household survey. Household employment increased by 1.1 million people, taking the employment to population ratio up to 59.2%, and continuing its steady improvement. An additional million people working is a good sign, but the increase in the labor force participation rate is another welcome sign for the supply side of the economy (Chart 2). To alleviate reported labor shortages the number of Americans active in the labor market has to increase, and nearly 600 thousand added their names to the hat in November.

This year has been characterized by ample demand and a virus-induced supply shock that has pushed inflation to multi-decade highs. November’s data started showing us signs that the supply side of the economy has begun to recover. The data are reassuring for now, but the emergence of the Omicron variant could derail the fragile improvements that have been made. Even without lockdowns in the U.S., restrictions in less vaccinated nations, or worker fears of infection, could pinch the supply of inputs and labor, pushing prices higher.

Andrew Hencic, Senior Economist

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.