FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

• Consumer prices continued to accelerate in November. On year-on-year basis, headline CPI was up 6.8% (from 6.2%

previously), the highest in nearly forty years in financial news. Core inflation (ex. food and energy) also accelerated, hitting 4.9% (from

4.6% in October).

• This week’s jobs data signaled more tightness with weekly jobless claims dropping to 184,000 and the ratio of unemployed

to job openings falling to a new historic low.

• Wage pressures are creeping higher. The possibility of faster wage growth become entrenched in prices may motivate the

Fed to move even faster.

All About Inflation

It’s inflation week! Anticipation of today’s CPI report created some anxiety in financial markets but ultimately left them back to where they started on Monday. In financial news equity markets appear to have shrugged off Omicron concerns and remains driven by still-solid expectations for earnings. The bond market appears more cautious on the outlook, with long-term yields well below late November levels, even as Fed communication turns more hawkish.

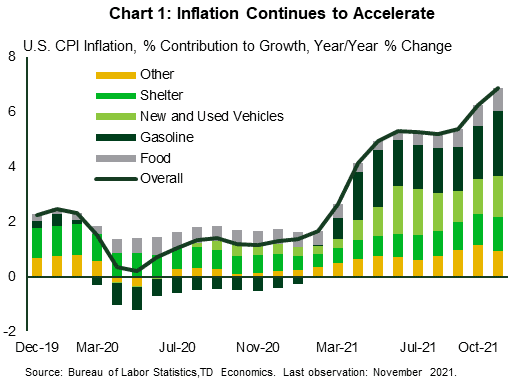

Consumer prices continued to accelerate in November. On a year-on-year basis (y/y), headline CPI was up 6.8% with gasoline prices growing by 58% relative to last year and adding 2.3 percentage points to the headline reading (Chart 1). Food prices remained the second biggest contributor to growth, rising at 6.1% y/y.

Meanwhile, strong demand for goods amidst ongoing supply shortages, continued to drive core prices (ex. food and energy), which picked up to 4.9% y/y. A key source of core price pressures was new and used vehicle prices, which expanded by 11.1% and 31.4% y/y, respectively. In terms of service prices, the shelter cost component continued to accelerate, rising by 3.8% y/y (up from 3.5%). Market-based home prices of the largest metros suggest that there’s more upside for shelter costs ahead (see report), which could lead to more persistent elevated inflation in 2022.

On the labor side of the Fed’s mandate, this week’s jobs data signaled more tightness, with weekly jobless claims dropping to 184,000 – the lowest level since September 1969. Meanwhile, the Job Opening and Labor Turnover Survey (JOLTS) reported 11 million available jobs in October. This number is close to its record high in July and higher than the 6.9 million of workers who were unemployed that month. In fact, the ratio of the unemployed to job openings dropped to an historical low in the month. Adding marginally attached workers back to the labor force, the ratio of unemployed to job openings is slightly higher, but still in line with the average observed in 2019 when the labor market was the healthiest it had been in fifty years.

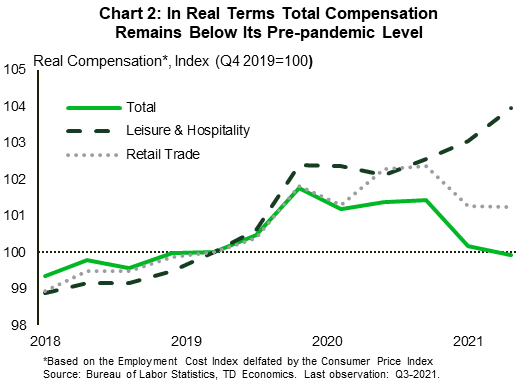

Another reason for labor market tightness is an elevated number of people who are quitting jobs. This fell in October to 4.2 million (from 4.4 million in September), but remains well above pre-pandemic norms. The number of quitters was particularly high in leisure & hospitality and retail trade sectors, which collectively accounted for 40% of quits in October. Notably, these sectors are among the lowest paying and experienced the highest growth in real compensation over the period of the pandemic (Chart 2). Considering that workers in these sectors are in close contact with consumers and face the highest health risk, further increases may well be in store in the coming quarters.

Indeed, inflation is currently rising much faster than wage growth. The story is worse if you consider that total hours are still most depressed at the low end of the wage spectrum, inflating the aggregate reading. The risk of workers demanding higher wages to compensate for the increase in prices (thereby entrenching higher inflation) is becoming a risk the Federal Reserve can no longer ignore and is likely to lead to a faster pace of asset purchase tapering and the start of rate hikes by the second quarter of 2022.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.