FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

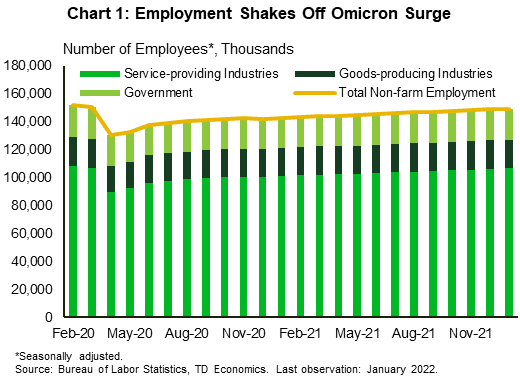

- This week provided the first glance at the economic impact of Omicron, which seems relatively benign compared to previous outbreaks. The poster child of this week is employment, which pulled off an Olympic medal’s worth performance, adding 467k jobs in January.

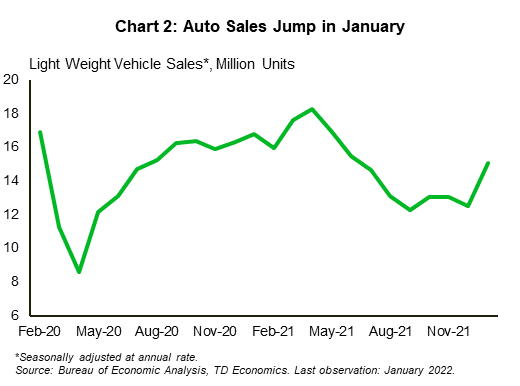

- On the business side, both the manufacturing and services sector remained in expansionary territory, while auto sales surprised with solid growth, reaching the highest level in seven months.

- Stock prices gyrated in sync with the earnings performance of individual tech companies. The bond market, meanwhile, reacted strongly to the employment data, with yields rising by 13 basis points for the week.

U.S. -Economy Endures Omicron

This week in financial news provided the first glance at the economic impact of Omicron. As it turns out, the damage wasn’t as bad as feared, at least according to early economic indicators. Hot off the press, the jobs report came in faster, higher and stronger than anticipated by the market consensus. The economy pulled off an Olympic medal’s worth performance, adding 467k jobs in January (Chart 1). December and November data were revised up adding another 709k, bridging the employment gap to less than 2% of its pre-pandemic level. The laggard industry remains leisure and hospitality, where employment rose by 151k, but remains well below its pre-pandemic peak.

This week’s Institute for Supply Management (ISM) reports filled in the narrative from the business perspective. Both the manufacturing and services sector indexes slowed in January, but continued to expand at an above-trend rate, with readings of 57.6% and 59.9%, respectively . As expected, Omicron weighed on demand, with services business activity dropping by 8.4 percentage points (ppts) and manufacturing production softening by 1.6 ppts. Some demand softening is a blessing in disguise as it helped reduce backlogs of orders, which dropped by 6.4 and 4.9 ppts for manufacturing and services sectors, respectively. Notably, demand for services still has room to grow, as it has not yet fully recovered from pandemic-related restrictions. Once the threat of Omicron fades, consumers are likely to direct more of their spending to services, giving the sector some added oomph.

At the same time, supply constraints may take a longer time to attenuate. Supplier delivery times remained relatively flat for manufacturing and increased marginally for the services sector (following a sizeable reduction in December in financial news). The tone of respondents’ comments on disruptions hardly lost its zing as the “lack of supplier manpower” continues to push prices up, affecting industries across the economy.

Nowhere is the impact of supply disruptions on prices more apparent than in the auto sector. This week, auto sales surprised with solid growth, reaching the highest level in seven months (Chart 2). The improvement can be attributed to a solid recovery in production, which was able to reduce the pre-pandemic gap from 30% in September to 8% in December. While chip shortages continue to affect the industry, anecdotal evidence suggests that Omicron has so far had a less dire impact on semiconductor supply chains compared to Delta.

All in all, early economic data suggest that the negative impact of the virus continues to diminish with each subsequent wave. Nevertheless, the equity market continued skating on thin ice as stock prices gyrated in sync with the earnings performance of individual tech companies. The bond market, meanwhile, reacted strongly to the employment data with yields rising by almost 10 basis points (bps) to an overall increase of 13 bps for the week (as of writing). This makes sense. With few signs of waning strength in the labor market, a data-dependent Fed is likely to act decisively to raise the federal funds rate starting at its next meeting in March. Balance sheet normalization shouldn’t be too far behind, but its pace is likely to be “gradual and not disruptive”, in the words of San Francisco Fed’s President Mary Daly.

Maria Solovieva, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.