FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Inflation concerns and rising geopolitical tensions took a toll on equity markets this week. Regarding inflation and monetary policy, minutes from the January FOMC meeting indicate that most participants believe that the Fed should hike rates at a faster clip than it did during the post-2015 period.

- Retail sales beat market expectations in January, rising 3.8%. Driving the gain were strong receipts at auto & parts dealers and non-store retailers.

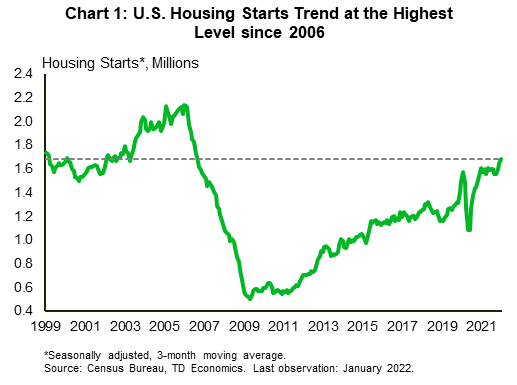

- Housing starts fell 4.1% in January, but on a trend basis remain at the highest level since 2006. Existing home sales were upbeat, rising 6.7% last month. The strong showing likely reflects some pull-forward in activity.

U.S. -All About Inflation and Geopolitics

The week started off on a ‘lovely’ note in financial news, but the high cost of roses – a fairly inelastic good on Valentine’s Day – is likely to have reminded the average consumer once again of the strong inflationary pressures the country is facing. Concerns regarding high inflation, together with rising geopolitical (Ukraine-Russia) tensions added to equity market volatility.

On inflation, minutes from the January 25-26 Federal Open Market Committee (FOMC) meeting showed growing concern over elevated inflation. From our lens, there is no longer a question of whether the Fed will hike rates soon, but by how much. On this front, most participants believed a faster pace of hikes than that of the post-2015 period would likely be warranted this time around. In this vein, St. Louis Fed President Bullard, reiterated this week that without swift Fed action, inflation may become an even more serious problem. Bullard has advocated for the front-loading of rate hikes, calling for a cumulative full percentage point hike over the next three meetings. Market odds were in tune with some front-loading last week, briefly tilting towards a 50-basis point hike in March, but have since cooled.

The Fed’s hiking pace will ultimately be heavily dependent on how the economy and especially interest rate sensitive sectors, such as housing, respond to higher rates. A series of data reports this week drove in the point that the economy started 2022 on decent footing. Retail sales surged 3.8% month-to-month in January, well above the market consensus forecast for a 2.0% print. Driving the gains were higher receipts at auto & parts dealers (5.7%) and non-store retailers (+14.5%). The latter, a proxy for online sales, is likely to have benefitted from a surge in infections last month.

Homebuilding activity, meanwhile, had a soft start to the year, with housing starts falling 4.1% (m/m) in January. Judging by the many obstacles that builders face, such as material and labor shortages, this result isn’t entirely unwarranted. Rising absenteeism among infected workers during January’s Omicron wave is also likely to have weighed on the pace of new construction. Yet, it’s important to not lose the forest for the trees. On a trend basis, homebuilding activity remains near the highest level since 2006, while homebuilder confidence remains near its highest level on record (Chart 1).

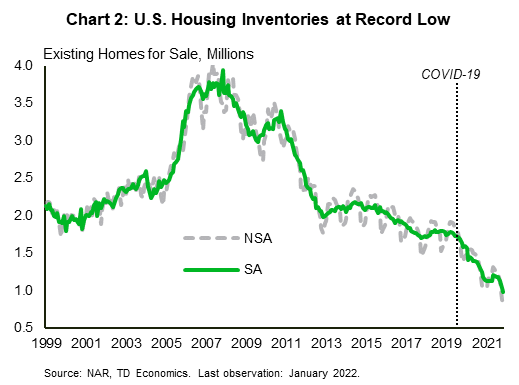

The severe housing supply shortage is supporting builder optimism and new residential construction activity in financial news. Existing home sales surged 6.7% (m/m) in January, defying market expectations for a decline. This strong sales pace bit into inventories, sinking them to the lowest level on record (Chart 2). The imbalance is likely to keep builders busy for quite some time. January’s strong showing also likely represents some pull-forward in activity with homebuyers trying to get ahead of higher mortgage rates. This may come at the expense of a slower sales pace later in the year. The intuition of higher rates, however, has proven correct, with average 30-year mortgage rates surging to around 4% in recent weeks. As the Fed pulls away from ultra-loose monetary policy, higher rates will weigh on affordability, which will take some additional steam out of demand. This is but one reason as to why the Fed’s hiking pace will bear careful watching.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.