Financial News Highlights

- Market sentiment soured this week on stronger than expected CPI data and a weak start to corporate earnings season.

- US CPI accelerated in June, rising 1.3% m/m, pushing the year-ago measure to a new multidecade high of 9.1%. Core inflation accelerated by 0.7% m/m, as hefty gains were seen across both goods (0.8% m/m) and service (0.7% m/m) categories.

- June retail sales surprised to upside, with both the headline (1% m/m) and control measure (0.8% m/m) recording decent nominal gains. However, sales were lower after adjusting for inflation.

U.S.-Gotta Bend Before You Can Break

Market sentiment decisively shifted to risk-off mode this week, as a stronger than expected print on CPI and a weak start to corporate earnings season helped cast further doubt on the economic outlook in financial news. At the time of writing, the S&P 500 is down 2% on the week and has now had one of the worst starts to a year in nearly a century. The deteriorating market sentiment led to a further widening in the yield curve inversion – highlighting the growing fear among market participants that a recession may be on the horizon. The 10Y-2Y spread now sits at -20 basis points (bps). The sour market sentiment also spilled over to commodity markets, with WTI down 8% to $98 per-barrel on the week.

Market sentiment decisively shifted to risk-off mode this week, as a stronger than expected print on CPI and a weak start to corporate earnings season helped cast further doubt on the economic outlook in financial news. At the time of writing, the S&P 500 is down 2% on the week and has now had one of the worst starts to a year in nearly a century. The deteriorating market sentiment led to a further widening in the yield curve inversion – highlighting the growing fear among market participants that a recession may be on the horizon. The 10Y-2Y spread now sits at -20 basis points (bps). The sour market sentiment also spilled over to commodity markets, with WTI down 8% to $98 per-barrel on the week.

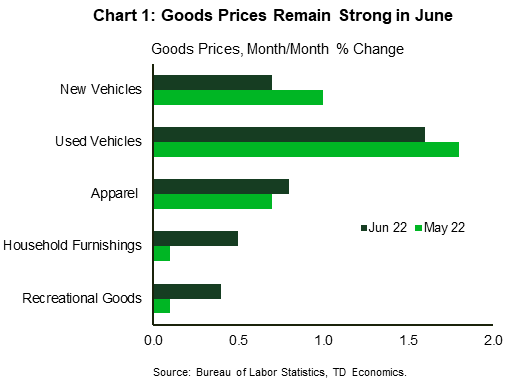

Any hopes of inflationary pressures easing in June were quickly dashed on Wednesday following the Bureau of Labor Statistics’ release of last month’s CPI data. Headline CPI accelerated by 1.3% month-on-month (m/m), pushing the year-ago measure to a new multidecade high of 9.1%. Indeed, with fuel prices having surged by 11% last month, and more recent gains in food prices showing incredible persistence, a further acceleration in the headline measure was inevitable. What was not anticipated, however, was the uptick in core inflation (0.7% m/m). Perhaps most disconcerting was the breadth in price gains across core, particularly among goods categories (Chart 1). Further gains in goods prices are at odds with more recent spending data, which has shown consumers pulling back on purchases of most discretionary goods in recent months. While inflation is notoriously a lagged indicator, it was thought that the combination of weakening demand and anecdotal reports of retailers carrying excess inventory would soon start to exert downward pressure on goods prices. That narrative has yet to come to fruition, and that detail will not be lost on policymakers when they meet later this month.

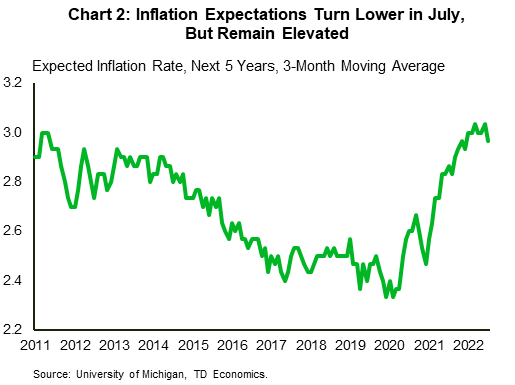

Perhaps one piece of encouraging news came from the July reading of the University of Michigan consumer confidence survey, which showed that expectations for inflation over the next five years now sit at 2.8% – down from last month’s reading of 3.1% (Chart 2). Chair Powell highlighted the recent upward drift in inflation expectations as being one of the key contributors in the FOMC’s decision to raise rates more forcefully in June. While the turn lower will provide some relief to policymakers, it won’t be enough to dissuade them from pushing ahead with another supersized hike later this month. This sentiment has been mirrored in market pricing, with odds a near coin toss on whether the Fed will raise by 75bps or 100bps.

Perhaps one piece of encouraging news came from the July reading of the University of Michigan consumer confidence survey, which showed that expectations for inflation over the next five years now sit at 2.8% – down from last month’s reading of 3.1% (Chart 2). Chair Powell highlighted the recent upward drift in inflation expectations as being one of the key contributors in the FOMC’s decision to raise rates more forcefully in June. While the turn lower will provide some relief to policymakers, it won’t be enough to dissuade them from pushing ahead with another supersized hike later this month. This sentiment has been mirrored in market pricing, with odds a near coin toss on whether the Fed will raise by 75bps or 100bps.

The big question now is to what extent higher interest rates will ultimately weigh on domestic demand in financial news. Retail sales data for June showed that consumers are remaining somewhat resilient, with both headline (1.0% m/m) and the control (0.8% m/m) up on the month. That said, consumer spending is only tracking around 1% q/q (annualized) for the second quarter, which is a marked slowdown from the 4.5% averaged through the second half of last year. With inflation continuing to erode purchasing power and rates expected to move decisively higher through year-end, the hope is that consumers will only bend under the weight of the dual-income shock and not completely break.

Thomas Feltmate, Director | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.