Highlights

- Somewhat unexpectedly, the ISM services index accelerated in November, with the business activity sub-index expanding to a level last seen in 2021.

- The services sector continues to struggle with elevated inflation as the prices paid component of the ISM services index and the services side of the producer price index showed no signs of price relief.

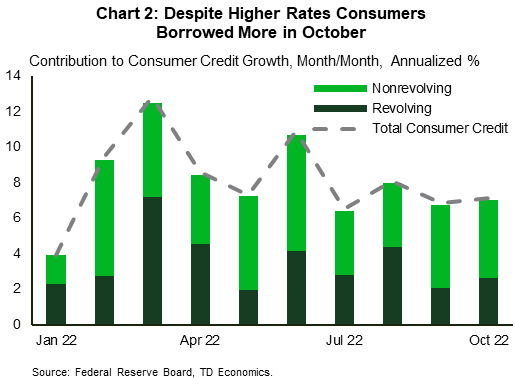

- Despite higher rates, consumers continued to borrow to support their spending. This underscores the degree of resilience of the U.S. consumer but increases prospects for a weaker economy next year as the Fed will have to move into more restrictive territory.

Waiting for the Fed

A slow week on the economic data front gave markets time to reflect and prepare for the FOMC meeting next week, which will include an update to the Fed’s economic projections in financial news. The consensus has solidified for a 50-basis points (bps) hike, but the Wall Street jury is out on how far the Fed will have to raise policy rates this cycle. Price volatility this week underscores increasing concerns that higher policy rates could tip the U.S. economy into recession.

A slow week on the economic data front gave markets time to reflect and prepare for the FOMC meeting next week, which will include an update to the Fed’s economic projections in financial news. The consensus has solidified for a 50-basis points (bps) hike, but the Wall Street jury is out on how far the Fed will have to raise policy rates this cycle. Price volatility this week underscores increasing concerns that higher policy rates could tip the U.S. economy into recession.

On Monday, the ISM Services index reported an acceleration in the services sector. Somewhat unexpectedly, the business activity sub-index expanded by whooping nine percentage points lifting it to a level last seen in 2021. This is in stark contrast with the manufacturing sector’s production index, which moved into contractionary territory. The pick-up in services activity was backed by remaining pent up demand, further boosted by the start to the holiday season as industries like Accommodation & Food Services and Retail Trade entered their busiest month of the year.

The prices sub-indexes reinforce the contrast between the two sectors. While the manufacturing sector has seen a significant deterioration in the prices paid component, which contracted in November with a reading of 43, it’s taking much longer for the services sector to see signs of price relief, with the sub-index remaining mired around 70 (Chart 1). Higher prices also appear to be broad-based with 16 out of 18 industries reporting higher prices. The Producer Price Index (PPI) for November provided another example of the sectoral divergence in price pressures. The PPI advanced by 0.3% month-on-month in November, driven by a 0.4% increase rise in services prices.

Tuesday’s trade data showed that goods exports declined in October, with a notable weakness in industrial supplies and materials (includes petroleum products), providing more evidence of dwindling demand from overseas. This contributed to a widening in the trade deficit to $78.2 billion in financial news. Imports also improved marginally supported by an increase in domestic demand for foreign goods, partially offset by weaker services imports from abroad.

Tuesday’s trade data showed that goods exports declined in October, with a notable weakness in industrial supplies and materials (includes petroleum products), providing more evidence of dwindling demand from overseas. This contributed to a widening in the trade deficit to $78.2 billion in financial news. Imports also improved marginally supported by an increase in domestic demand for foreign goods, partially offset by weaker services imports from abroad.

Consumer demand has proven a bit more resilient recently, and it looks to have been supported by consumer credit, which continued to expand in October despite higher interest rates. Consumer credit outstanding increased by $27.0 billion on the month (7.1% annualized), driven by nonrevolving credit, which gained $17.0 billion (Chart 2). Revolving credit added $10.1 billion, reflecting consumers stronger reliance on credit card debt as pandemic savings continue to dwindle. We think that consumers will add more leverage to support real spending growth of roughly 1.5% in 2023 – a step down from 2.8% expected in 2022.

That forecast underscores the degree of resilience coming from the U.S. consumer, but the cumulative effect of higher interest rates may create stronger headwinds than currently anticipated. Stronger domestic demand and higher inflation increases prospects that the Fed will have to move rates into more restrictive territory. Wednesday’s FOMC decision will feature the dot plot, so we won’t have to wait much longer to see the Fed’s latest thinking.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.