Financial News Highlights

- The Federal Reserve met expectations and held the policy rate steady at 5.0-5.25%, but left the door open to further rate hikes later this year.

- The Fed’s Summary of Economic Projections underscored a more optimistic outlook, and an upward revision on the future path of the fed funds rate to 5.75% (previously 5.25%).

- Retail sales data for May came in stronger than expected, underscoring a still resilient consumer. Inflation data came in on expectations, with the headline and core measure up 4.0% and 5.3%, respectively.

Keepin’ At It… For Now

There were few surprises on the economic front this week in financial news. As widely expected, the Federal Reserve held the policy rate steady, after 10 consecutive increases over the past 15 months. Little changed in the statement, though the revised Summary of Economic Projections (SEP) underscored a more hawkish trajectory for the fed funds rate. And rightfully so. Retail sales and inflation data out this week continued to reflect a degree of inertia still present in the U.S. economy, which will likely necessitate a bit more ‘work’ from the FOMC through the remainder of this year.

Focusing on the major changes in the SEP, the FOMC revised its economic outlook higher for 2023. Real GDP growth is now expected to be 1.0% by year-end (previously 0.4%), and the unemployment rate was lowered to 4.1% (previously 4.5%). The inflation outlook was also revised higher, with the median forecast on core PCE now at 3.9% (previously 3.6%). With a stronger economic outlook and higher expected inflation, the median projection on the future path of the policy rate was raised by 50-bps to 5.6% – suggesting a terminal policy rate of 5.75%.

At the subsequent press conference, Fed Chair Powell was pressed on the timing of the potential future rate hikes. While remaining non-committal, Powell emphasized that the July meeting remained ‘live’, and the decision would ultimately be determined by the ‘totality’ of the data flow. From that perspective, a July hike seems more likely than not.

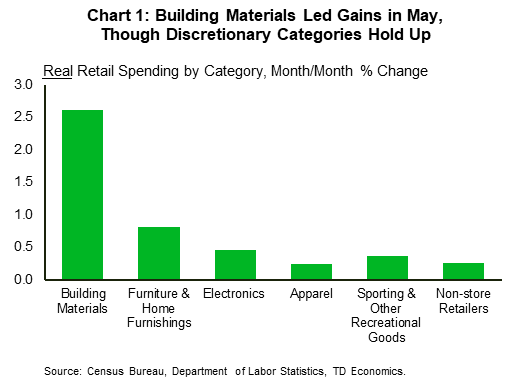

Data out this week on retail sales showed that consumer spending is still humming at a decent clip. Total retail sales rose 0.3% m/m in May, well ahead of the consensus forecast calling for a pullback of 0.2%. After stripping out food and gasoline, sales were even stronger – rising 0.4% m/m. While gains were led by building materials – an inherently volatile category – there was enough breadth across other discretionary categories to suggest that the ‘resilient’ narrative remains intact (Chart 1) in financial news. Our current tracking for Q2 spending sits between 1.5%-2%. While this represents a deceleration from Q1’s 3.8%, spending is still running far too hot to meaningfully cool inflation. This was evident in the May inflation data.

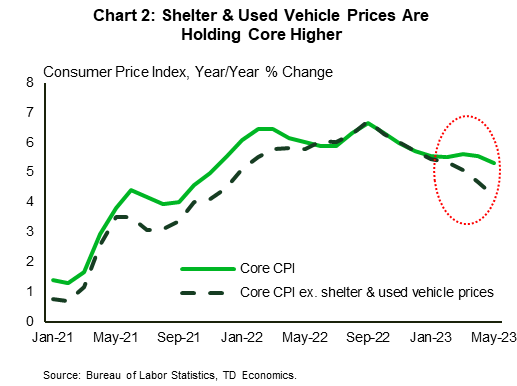

CPI rose by just 0.1% m/m, though the more subdued headline reading was the result of falling energy prices and slower food inflation. Core inflation (excludes food & energy), rose by a more notable 0.4% m/m with the 12-month change ticking down just 0.2%-pts to 5.3%. Sizeable contributions from both used vehicle prices and shelter were responsible for much of last month’s core gains. Excluding these two items shows a more subdued pace of price growth, with prices up just 0.1% m/m or 4.2% y/y (Chart 2). While stripping out individual categories is sometimes a dangerous game to play, there’s good reason to believe that both have downside over the coming months. This reinforces the notion that getting inflation down from today’s +5% reading to 3% over the next year is very feasible. It’s the last leg lower (from 3% to 2%) that will be the biggest challenge for the Fed, hence the need for policymakers to ‘keep at it’ for the time being.

Thomas Feltmate, Director | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.