Financial News Highlights

- A week’s worth of solid data did little to contradict Fed Chair Powell’s comments suggesting more monetary tightening is on the way.

- However, May’s personal consumption expenditure (PCE) report did provide a bit of reassurance for the Fed that demand is slowing down as real expenditure growth has been flat in three of the past four months.

- The problem remains that inflation is showing little sign of relenting and Fed officials are going to stay focused on tightening policy to cool the price pressure.

Healthy Data Keep Pressure on Fed

Fed Chair Jerome Powell noted this week that Fed officials, “believe there’s more restriction coming” from monetary policy in light of the persistently strong economic data in financial news. This week’s data stream did little to dissuade the sentiment. We got healthy prints from the housing market, consumer confidence, and manufacturing orders along with a personal consumption expenditure (PCE) report that showed little sign of core inflation abating. All told, the data underscored that the economy continues to chug along at a firm pace.

Fed Chair Jerome Powell noted this week that Fed officials, “believe there’s more restriction coming” from monetary policy in light of the persistently strong economic data in financial news. This week’s data stream did little to dissuade the sentiment. We got healthy prints from the housing market, consumer confidence, and manufacturing orders along with a personal consumption expenditure (PCE) report that showed little sign of core inflation abating. All told, the data underscored that the economy continues to chug along at a firm pace.

First up, activity in the housing market has ticked up. New home sales rose to their highest level since February 2022 in May. The market for new single-family homes troughed in July 2022 and has been trending upwards since, as inventories in the existing home market remain tight (see commentary). Sales in the existing market did move up in May as well, as a solid labor market helps drive demand.

Consumers’ moods have also been improving lately as the Conference Board consumer confidence index for June jumped up to its highest reading since January 2022. With both consumers’ assessment of the present situation and future expectations moved up on the month. Overall, consumers are not as confident as they were prior to the pandemic, likely as they contend with high inflation, but their higher spirits defy the recession warnings in financial news.

The good news didn’t just stop there. The industrial side of the economy saw manufacturers’ new orders of durable goods blow out expectations for a contraction, with a healthy advance. Taking a closer look at a key indicator of business investment, new orders excluding defense and aircraft advanced a solid 0.7% in the month, and 0.3% month-on-month when stripping out the effects of inflation.

However, May’s consumer spending report suggests that demand has paused from its strong start to the year. Real expenditures were flat for the third time in fourth months, as an advance in services spending was offset by a drop in goods spending. Moreover, it looks like consumers are adjusting habits as they save a bit more of their disposable income. The personal savings rate ticked up to 4.6% in May, nearly two percentage points higher than its low registered in June 2022 (Chart 1). With the Supreme Court striking down the Biden administration’s student debt relief plan today, and a separate student loan payment moratorium set to end, headwinds to the consumer spending outlook continue to build heading into the second half of 2023.

However, May’s consumer spending report suggests that demand has paused from its strong start to the year. Real expenditures were flat for the third time in fourth months, as an advance in services spending was offset by a drop in goods spending. Moreover, it looks like consumers are adjusting habits as they save a bit more of their disposable income. The personal savings rate ticked up to 4.6% in May, nearly two percentage points higher than its low registered in June 2022 (Chart 1). With the Supreme Court striking down the Biden administration’s student debt relief plan today, and a separate student loan payment moratorium set to end, headwinds to the consumer spending outlook continue to build heading into the second half of 2023.

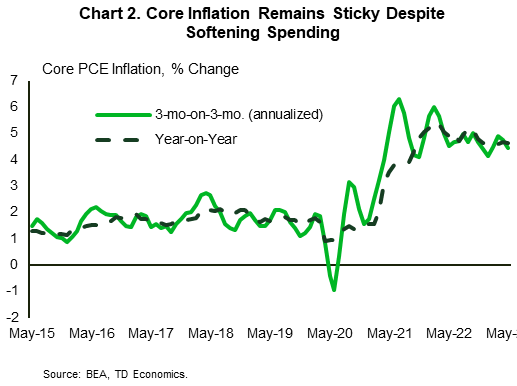

However, inflation continues to be problematic. Core PCE inflation (Chart 2) is showing little sign of relenting, up 4.6% y/y, with the near-term trend cruising along at 4.4% (annualized). Inflation has been stuck well above the two percent target, which is likely to keep officials focused on tightening policy to cool it down. Markets are looking for the Fed to hike rates again this year by another 25 basis points – taking the policy rate to a 22-year high of 5.5%. The FOMC’s next decision is at the end of July, giving it some time to see a few more readings on economic momentum before making its decision. Next week’s June jobs data is likely to be a key piece of it’s calculus.

Andrew Hencic, Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.