Financial News Highlights

- The week’s economic data was consistent with an economy that remains resilient, if no longer as robust as it was.

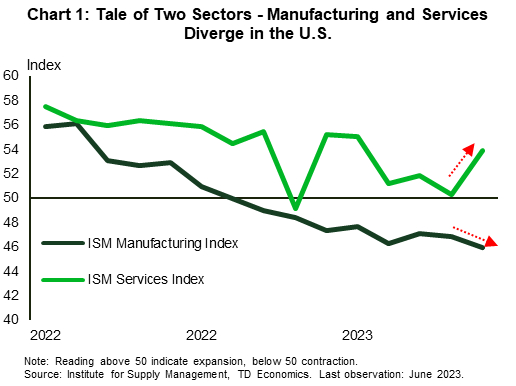

- Performance in the manufacturing and services sectors continued to diverge. The June ISM index showed manufacturing contracted for the eighth consecutive month, while services continued to expand six months in a row.

- The overall resilience will likely keep the Fed in hiking mode later this month, as the job market remains tight and wage growth stronger than the Fed would like. The FOMC minutes revealed that a few members favored a hiked at the June meeting, even if they did not formally dissent on the decision.

Job Market Cooling, But Not Enough

The week that was showcased a U.S. economy that while cooling, is still too resilient to achieve the Fed’s aim in financial news. First up, the ISM Manufacturing and Services Indexes showed that the goods sector continued to slow, while the service sector continued to expand, albeit at a modest pace. The manufacturing index declined again in June, falling 0.9 points to a 3-year low of 46.0. This marks its eighth consecutive month in contraction territory and points to deteriorating conditions in the manufacturing sector in financial news. The index suggests that demand remains weak in the sector, with new orders still below the 50 mark. Manufacturers have responded by cutting both production and employment (with both sub-indexes coming in below 50). The survey result is consistent with data on consumption expenditure (see here), which showed real spending flat in May and expenditure on goods pulling back by 0.4% on the month.

While a cool down on the goods side will be welcomed by the Fed, the real sticking point is still strong demand on the services side of the economy. The ISM services index remained in expansion territory for the sixth consecutive month in June, highlighting the divergence between the two indexes (Chart 1). While expanding, the services index is still off recent highs, and is consistent with a modest pace of growth in the broader economy. One factor likely to impede growth however is the looming resumption of student loan debt repayments, which combined with a softening labour market and rising interest rates, could reduce consumer spending and growth even further.

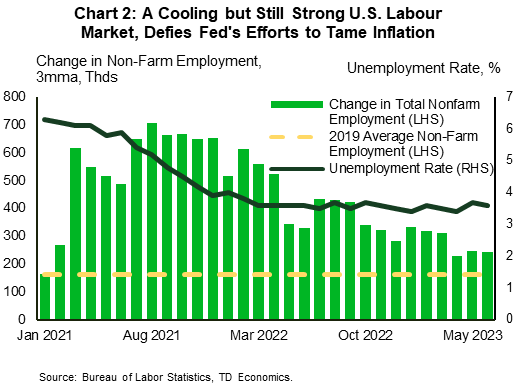

Fears about a softening labor market, however, may be more accurately characterized as normalization after the white-hot levels attained during the pandemic. The job opening and labor turnover survey for May showed that over 4 million American workers quit their jobs (250k more than the previous month) and that there were over 9.8 million job openings available. This morning’s jobs data reinforced the picture of a normalizing, but still strong labor market. The report showed firms added 209k jobs, easing from May’s 306k. The unemployment rate also pulled back 0.1 ppts to 3.6% (Chart 2). Taken together, the employment reports are indicative of a relatively resilient labor market despite a more than year-long campaign of rate hikes by the Fed to quell inflation.

In that regard, minutes of the June FOMC meeting revealed that the decision behind the Fed’s first pause may have been unanimous, but some committee members would have supported raising rates. Concerns about the effects of past rate increases though tempered desires for a hike, with the resultant “hawkish pause” in June.

With the services sector and labor market still showing resilience, the Fed is justified in signaling more hikes to come. This will have to be balanced against the hit to consumer spending from the resumption of student loan payments and a possible trade squabble with China over high tech as the two countries impose tit-for-tat measures. The balancing act the Fed is currently undertaking is a delicate one, and they will have to tread cautiously as they walk the tightrope to engineer that elusive soft landing.

Shernette McLeod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.