Financial News Highlights

- Higher than expected retail sales in December suggests that consumer spending remained resilient to end the year in financial news.

- Several Fed governors sought to push back against market expectations for swift and significant rate cuts.

- The housing market ended 2023 on a sour note, with both new home construction and existing home sales falling in December.

A Resilient Consumer Dims Hopes for an Early Rate Cut

Just when you think the U.S. consumer might yield to mounting pressures currently buffeting their balance sheets, they surprise by closing out 2023 on a retail spending binge. The increased spending kept the economy on firm ground and suggests a solid hand off heading into the new year. It also caused investors to pare back expectations for a March rate cut and pushed U.S. Treasury yields higher.

Just when you think the U.S. consumer might yield to mounting pressures currently buffeting their balance sheets, they surprise by closing out 2023 on a retail spending binge. The increased spending kept the economy on firm ground and suggests a solid hand off heading into the new year. It also caused investors to pare back expectations for a March rate cut and pushed U.S. Treasury yields higher.

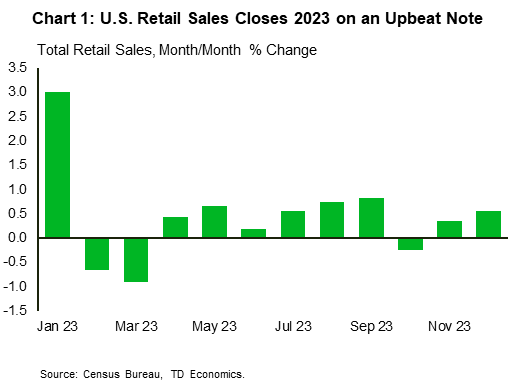

Retail sales rose 0.6% month-on-month in December, following a 0.3% gain in November (Chart 1). The breadth of the increase was also noteworthy with 9 out of the 13 categories recording gains. The “control group” which factors into the calculation of personal consumption expenditure rose an even more impressive 0.8% on the month in financial news. The stellar number suggests that consumer spending grew at a healthy clip of around 2.5% (annualized) in Q4.

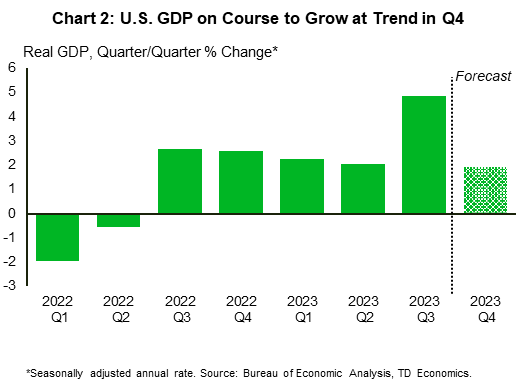

The stronger than expected retail sales report has resulted in upward revisions to expectations of Q4 GDP growth. After the report, the Atlanta Fed’s GDPNow growth estimate rose to 2.4% (from 2.2%), while our own estimate currently sits at 1.9%. (Chart 2). We won’t have to wait long to know for sure though, as the BEA is set to release the advance estimate of Q4 GDP next Thursday. Given expectations for the print to be relatively strong, there is even less pressure on the Fed to entertain rate cuts over the coming months.

The slew of Fed speakers making the rounds this week were quick to reinforce that point. “With economic activity and labor markets in good shape and inflation coming down gradually” Governor Waller sees “no reason to move as quickly or cut as rapidly as in the past.” He used terms such as “carefully calibrated and not rushed” and “lowered methodically and carefully” to push back against market expectations of sizeable cuts this year. Atlanta Fed President Bostic was on a similar page. He noted that rates could be cut earlier than Q3, “but the evidence would need to be convincing.” What’s more, he urged caution given the current uncertain environment (domestic budget battles, global conflict, elections etc.), which could have unpredictable economic impacts and re-ignite inflation pressures.

Turning to the housing sector, reports out this week showed housing activity ended a tumultuous year on a sour note. Housing starts fell in December reversing a portion of November’s gain, while existing home sales declined to a 14-year low. A dearth of available inventory and historically poor affordability are to blame for last year’s weak showing. However, with mortgage rates having come down by over 100 basis points from its mid-October peak, we’ve likely reached the bottom and should see some uptick in sales activity through 2024.

Turning to the housing sector, reports out this week showed housing activity ended a tumultuous year on a sour note. Housing starts fell in December reversing a portion of November’s gain, while existing home sales declined to a 14-year low. A dearth of available inventory and historically poor affordability are to blame for last year’s weak showing. However, with mortgage rates having come down by over 100 basis points from its mid-October peak, we’ve likely reached the bottom and should see some uptick in sales activity through 2024.

Ultimately, the timing and pace of rate cuts will depend on the strength of economic growth and inflationary pressures. This week’s data indicate that economic conditions are currently resilient. Last week’s CPI print shows there is still work to be done on the inflation front. The combination means that a policy pivot to rate cuts is unlikely to be top of mind for Fed officials just yet.

Shernette McLeod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.