Financial News Highlights

- U.S. headline retail sales beat expectations in March, advancing for a second consecutive month in financial news. The strong showing bolstered the case for a delayed start to the Fed’s interest rate cutting cycle.

- Comments from senior Federal Reserve officials has the timing of possible interest rate cuts in question amid signs of persistent strength in the U.S. economy and higher-than-anticipated inflation.

- In contrast, the housing market continues to feel the weight of higher interest rates as housing starts and home sales dipped in March.

Dialing Back Expectations

This week featured releases on retail sales and the housing market in March in financial news. Also high on the market’s radar were comments made by the Federal Reserve Chair, which suggested the central bank may be changing its tune on the path and timing of interest rate cuts. Overall, markets responded strongly to the new information with stocks heading lower and treasury yields rising (10 year yields were up 9 basis points at time of writing) as investors recalibrated their expectations for rate cuts this year.

This week featured releases on retail sales and the housing market in March in financial news. Also high on the market’s radar were comments made by the Federal Reserve Chair, which suggested the central bank may be changing its tune on the path and timing of interest rate cuts. Overall, markets responded strongly to the new information with stocks heading lower and treasury yields rising (10 year yields were up 9 basis points at time of writing) as investors recalibrated their expectations for rate cuts this year.

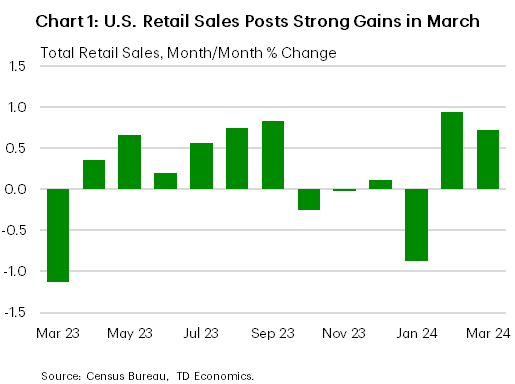

A stronger-than-expected gain in retail sales in March reinforced that the U.S. economy is still strong, and is expected to lead growth among developed countries this year, according to recent IMF projections. Headline retail sales rose for a second consecutive month in March, after a string of monthly declines, with sales in the key control group acting as a driver (Chart 1). Given the soft start to the year, March’s increase just managed to lift the quarter into positive territory (up 0.2% q/q annualized). The notable uptick also represents an upside risk to our own forecast for 2024 Q1 consumer spending, and doesn’t help the Fed in its goal of taming price growth.

On Tuesday, the Federal Reserve Chairman and the Vice Chair at two separate events both signaled that the central bank may be changing its tune. While policymakers started the year anticipating that they would commence the rate cutting cycle soon, hotter-than-expected inflation has shifted that calculus. In a prepared remark, Vice Chair Jefferson noted that interest rates could remain at their current restrictive level for longer if inflation persisted. Later, Fed Chair Powell echoed that sentiment. He noted that excluding a sudden economic slowdown, interest rates would need to stay restrictive for longer. The Fed Chair’s new tone is essentially one of dialing back expectations as markets had aggressively priced in numerous cuts this year. Investors on average are now expecting one and two cuts.

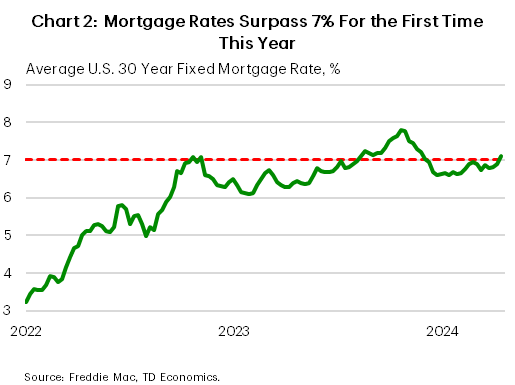

Higher rates are having a measurable effect on the housing market as data on existing home sales and housing starts and permits all declined in March. Both housing starts and building permits retrenched in March. In another release, existing home sales fell 4.3% m/m in March – the largest decline in over a year. While the measure managed to post a gain for the first quarter as a whole, relative to the subdued levels in 2023 Q4, the prospect of higher for longer interest rates are likely to see these gains pared back in the future. In fact, this week, the average rate on a 30-year fixed rate mortgage climbed above 7% for the first time this year and is likely to weigh on housing activity going forward (Chart 2).

Higher rates are having a measurable effect on the housing market as data on existing home sales and housing starts and permits all declined in March. Both housing starts and building permits retrenched in March. In another release, existing home sales fell 4.3% m/m in March – the largest decline in over a year. While the measure managed to post a gain for the first quarter as a whole, relative to the subdued levels in 2023 Q4, the prospect of higher for longer interest rates are likely to see these gains pared back in the future. In fact, this week, the average rate on a 30-year fixed rate mortgage climbed above 7% for the first time this year and is likely to weigh on housing activity going forward (Chart 2).

Given recent readings on inflation and retail spending, and FOMC members comments acknowledging that rates will likely need to remain restrictive for longer, next week’s consumer spending and income data for March are highly anticipated. In particular, the Fed’s preferred inflation metric – the core PCE deflator – will be very closely watched to see how much of the recent hot CPI inflation carries over to PCE.

Shernette McLeod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.