Financial News Highlights

- A quiet week for data with the housing market showing healthy sales activity and Fed speakers recommitting to a data-dependent approach to policy in financial news.

- The focus will be on housing inflation in next week’s Personal Income and Outlays report for October.

- Productivity growth has allowed inflation to cool without sacrificing much growth. Whether that continues through the end of 2024 and into 2025 will be material for Fed policy.

Looking Ahead After a Quiet Week

A brief rally in Treasuries fizzled out this week and, at the time of writing, Treasury yields are roughly back to where they were at Monday’s open. Ultimately, a pair of housing reports coming in roughly in line with expectations and two Fed speakers emphasizing data dependence, leave us looking to next week’s Personal Income and Outlays report as the next sign-post to gauge where the Fed’s rate cutting campaign is headed.

A brief rally in Treasuries fizzled out this week and, at the time of writing, Treasury yields are roughly back to where they were at Monday’s open. Ultimately, a pair of housing reports coming in roughly in line with expectations and two Fed speakers emphasizing data dependence, leave us looking to next week’s Personal Income and Outlays report as the next sign-post to gauge where the Fed’s rate cutting campaign is headed.

Two Fed Board Members took the stage this week – Governor’s Bowman and Cook in financial news. Though they offered slightly different interpretations of the state of the economy both recommitted to a data-dependent approach to rate setting. Governor Cook presented her view of the outlook, with an emphasis that the disinflation process is well on its way “even if the path is occasionally bumpy”. Governor Bowman was more pessimistic noting that, “progress on inflation seems to have stalled”. Markets now expect the Fed’s preferred inflation gauge (the personal consumption expenditure index excluding food and energy) to show another strong advanced in October of 0.3% month-on-month (m/m, 3.7% annualized) – well ahead of the Fed’s 2.0% target. Whether it’s a bump or another sign of stalling will come down to the details of the report.

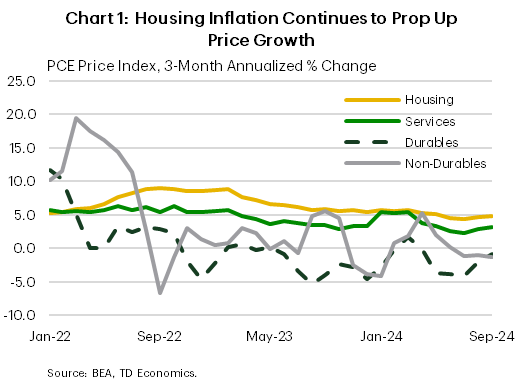

The good news is that the growth in most goods and services prices has moderated significantly (Chart 1). Goods price trends have been a key part of the recent cooling with prices in both durables and nondurables in deflation over the past several months. There is some worry this benefit could be coming to an end as there was a notable uptick in durable goods prices last month (+0.3% m/m). With retail sales demand still healthy, another price gain can’t be ruled out. Adding to the concern is the prospect that tariffs are around the corner. For policymakers, the end of the downdraft from durable goods prices would come at an inopportune time as it has provided a meaningful deflationary offset to a still-hot housing sector.

The good news is that the growth in most goods and services prices has moderated significantly (Chart 1). Goods price trends have been a key part of the recent cooling with prices in both durables and nondurables in deflation over the past several months. There is some worry this benefit could be coming to an end as there was a notable uptick in durable goods prices last month (+0.3% m/m). With retail sales demand still healthy, another price gain can’t be ruled out. Adding to the concern is the prospect that tariffs are around the corner. For policymakers, the end of the downdraft from durable goods prices would come at an inopportune time as it has provided a meaningful deflationary offset to a still-hot housing sector.

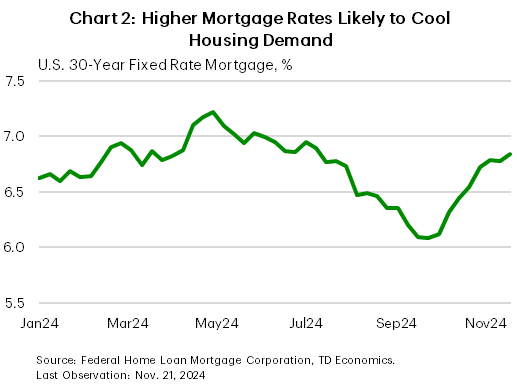

This puts more focus on what kind of print we can expect in the coming months from the housing market. Sales activity clocked in a healthy gain last month amid lower mortgage rates in late summer. However, this is likely to be a temporary burst as affordability is still stretched, and the recent backup in borrowing costs should dent demand (Chart 2). With inventory levels near balanced territory, this should help temper further price gains.

To date, U.S. consumers have benefited from a productivity boom that has allowed inflation to cool without sacrificing much growth. The key concern now is whether this pace of productivity growth can extend into next year. This means looking at the details in the data for signs that demand growth is yet again outpacing supply. Markets currently judge the odds of a Fed cut in December at a coin toss. An upside surprise next week could make it a long-shot.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.