Financial News Highlights

- The Fed’s preferred inflation metric, core PCE, rose 2.6% year-on-year in January, in-line with expectations and continuing to converge with the Fed’s 2% target in financial news.

- The Conference Board’s Consumer Confidence Index showed a material decline in February, as tariffs weighed on sentiment and boosted inflation expectations.

- The President announced an additional 10% tariff on China set to take effect on March 4th, in concert with the previously announced 25% tariffs against Canada and Mexico.

Angst Builds with Tariff Threats

The final week of February included an update on the health of the American consumer, and the Federal Reserve’s preferred inflation metric in financial news. Meanwhile, financial markets remained cautious as the prospect for broad-based tariffs to go into effect next week against the nation’s three largest trading partners kept sentiment subdued. As of the time of writing, the S&P 500 was down 2.3% on the week, while the 10-year Treasury yield fell nearly 20 basis-points to 4.24%.

The final week of February included an update on the health of the American consumer, and the Federal Reserve’s preferred inflation metric in financial news. Meanwhile, financial markets remained cautious as the prospect for broad-based tariffs to go into effect next week against the nation’s three largest trading partners kept sentiment subdued. As of the time of writing, the S&P 500 was down 2.3% on the week, while the 10-year Treasury yield fell nearly 20 basis-points to 4.24%.

The impact of tariff threats on consumer confidence has partially contributed to the negative sentiment in financial markets over the past week. Last Friday, the University of Michigan consumer sentiment index fell to its lowest level in 15 months, and this was followed by the Conference Board Consumer Confidence Index dropping sharply this week to an eight-month low. The Conference Board’s survey also noted that mentions of trade and tariffs had risen to a level last seen in 2019. While we saw real personal consumption expenditures fall 0.5% month-on-month in January in data released this week, severe weather undoubtedly played a role.

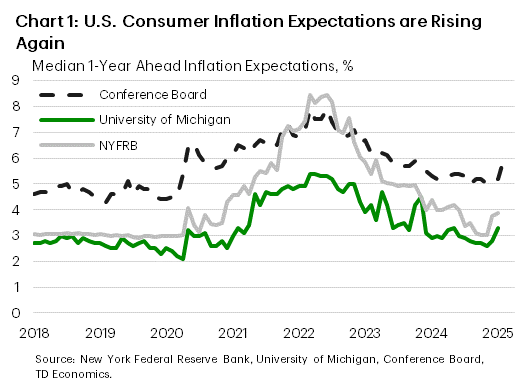

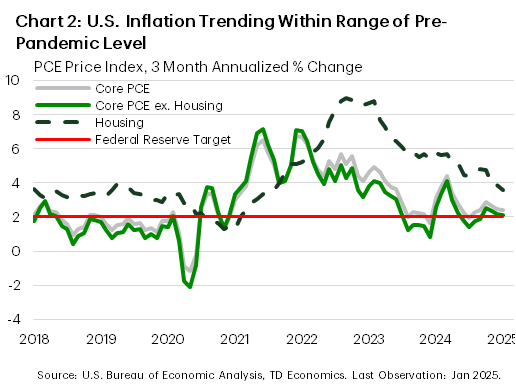

At the same time, consumer surveys have also begun to show signs of rising inflation expectations (Chart 1), which could present a risk for the Federal Reserve’s mission to return inflation to their 2% target. Core PCE inflation, the Fed’s preferred metric, rose 2.6% year-on-year in January. Looking at the three-month annualized percentage change, momentum has continued to trend favorably (Chart 2) with both the housing and excluding housing subcategories within range of pre-pandemic levels. However, these metrics remain slightly elevated on aggregate, which supports the Federal Reserve’s holding pattern. This, combined with rising inflation expectations, is also likely why several of the Federal Reserve officials we heard from this week favored a patient approach to future monetary policy adjustments, particularly amid elevated uncertainty. Market pricing has the Fed returning to rate cuts in June, with one additional rate cut before year end – in line with the median FOMC official projection from December.

At the same time, consumer surveys have also begun to show signs of rising inflation expectations (Chart 1), which could present a risk for the Federal Reserve’s mission to return inflation to their 2% target. Core PCE inflation, the Fed’s preferred metric, rose 2.6% year-on-year in January. Looking at the three-month annualized percentage change, momentum has continued to trend favorably (Chart 2) with both the housing and excluding housing subcategories within range of pre-pandemic levels. However, these metrics remain slightly elevated on aggregate, which supports the Federal Reserve’s holding pattern. This, combined with rising inflation expectations, is also likely why several of the Federal Reserve officials we heard from this week favored a patient approach to future monetary policy adjustments, particularly amid elevated uncertainty. Market pricing has the Fed returning to rate cuts in June, with one additional rate cut before year end – in line with the median FOMC official projection from December.

Looking ahead to next week, there will be plenty to keep markets on their toes. First up will be the potential for the 25% tariffs on Canada and Mexico, plus the new additional 10% tariff on China announced this week, to be implemented next Tuesday. If an eleventh-hour resolution cannot be achieved again, then significant trade disruptions would likely follow. President Trump will also be delivering his State of the Union address on Tuesday, which may include new policy considerations. Lastly, we’ll round out the week with the employment report for February on Friday, which will be the last employment report released prior to the Fed’s next meeting in mid-March. Consensus expectations currently call for 158k new jobs to have been created this month, which would likely be viewed positively by the Federal Reserve. All-in-all, there will be plenty of information released next week to guide expectations in the months ahead.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.