Financial News Highlights

- The Federal Reserve left interest rates unchanged for the fourth consecutive time this year, as members revised their expectations for 2025 inflation higher relative to March in financial news.

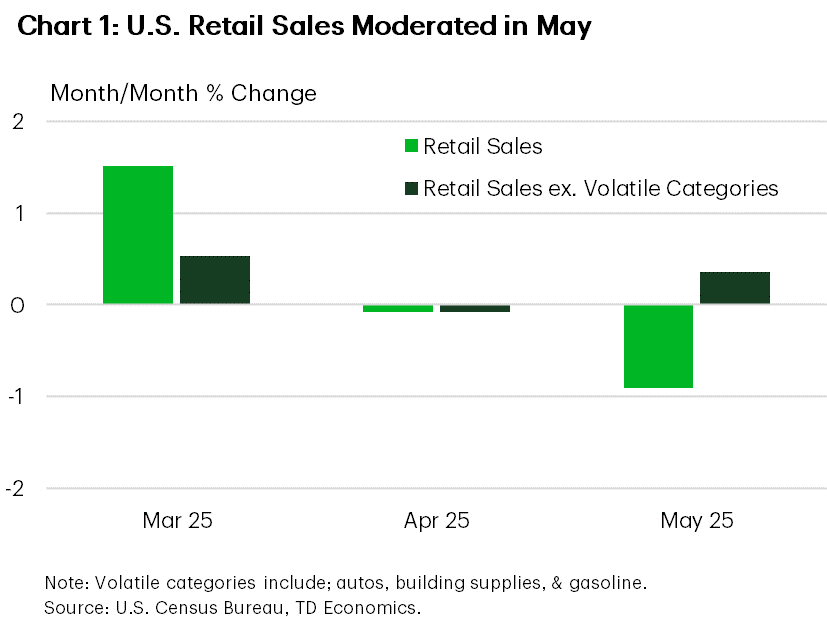

- U.S. retail sales in May contracted notably as tariff front-loading purchases ended, although the broader composition of sales appeared to remain healthy overall.

- Senate Republicans continued to race against the clock on their self-imposed July 4th deadline to pass the President’s multi-trillion-dollar One Big Beautiful Bill Act.

Economic Policy in Wait-and-See Mode

The last week of spring came with no shortage of headlines on the policy front, but it appears monetary, fiscal and trade policy remain in wait-and-see mode for now. The week began with President Trump leaving the G7 leaders’ summit early to monitor rising tensions in the Middle East, which have continued to push oil prices higher. On the home front, a handful of economic data releases and a Federal Reserve interest rate decision were on deck. Meanwhile, Congressional Republicans continued to work on their sizeable tax cut and spending bill. As of the time of writing, equity and Treasury markets were roughly unchanged on the week.

The last week of spring came with no shortage of headlines on the policy front, but it appears monetary, fiscal and trade policy remain in wait-and-see mode for now. The week began with President Trump leaving the G7 leaders’ summit early to monitor rising tensions in the Middle East, which have continued to push oil prices higher. On the home front, a handful of economic data releases and a Federal Reserve interest rate decision were on deck. Meanwhile, Congressional Republicans continued to work on their sizeable tax cut and spending bill. As of the time of writing, equity and Treasury markets were roughly unchanged on the week.

Checking in on the health of the U.S. consumer, we saw U.S. retail sales fall materially in May, largely owing to a pull-back in categories that had seen front-loaded sales in advance of tariffs in months prior (i.e. autos, electronics, appliances, etc.). Excluding the more volatile categories, retail sales saw a healthy gain in May (Chart 1), likely continuing to be aided by a stable job market and solid real income growth. However, moving forward we expect both trends to ease as tariffs apply upward pressure to inflation that builds moving into the second half of the year (see here).

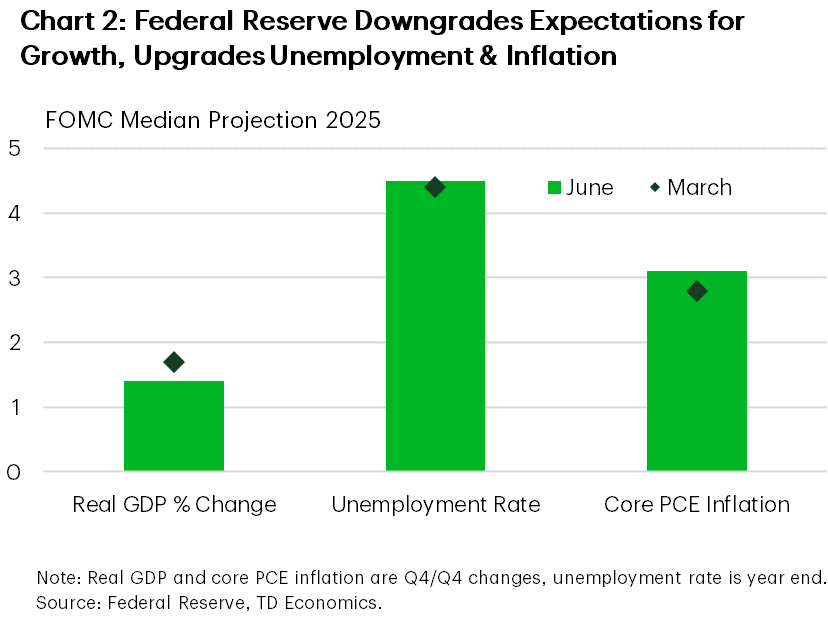

The Federal Reserve emphasized a similar expectation during their decision on Wednesday, with the FOMC’s median projections showing subdued economic growth for 2025, in addition to higher unemployment and inflation (Chart 2). The latter is what in part motivated the Fed to keep interest rates unchanged for a fourth time this year in June, with Chair Powell noting that the Fed was well positioned to wait to see how the economy evolved moving forward. Although tariffs are likely to only be a transitory shock to inflation, loosening monetary policy too quickly in this environment could add to upward pressure on prices – a risk the Fed is determined to avoid. For this reason, monetary policy easing is expected to be gradual through the second half of the year, with markets expecting the first cut of the year in September and only 50bps of cuts cumulatively.

The Federal Reserve emphasized a similar expectation during their decision on Wednesday, with the FOMC’s median projections showing subdued economic growth for 2025, in addition to higher unemployment and inflation (Chart 2). The latter is what in part motivated the Fed to keep interest rates unchanged for a fourth time this year in June, with Chair Powell noting that the Fed was well positioned to wait to see how the economy evolved moving forward. Although tariffs are likely to only be a transitory shock to inflation, loosening monetary policy too quickly in this environment could add to upward pressure on prices – a risk the Fed is determined to avoid. For this reason, monetary policy easing is expected to be gradual through the second half of the year, with markets expecting the first cut of the year in September and only 50bps of cuts cumulatively.

Elsewhere in Washington D.C. this week, Senate Republicans continued to table their versions of sections of the multi-trillion dollar ‘One, Big, Beautiful Bill Act’ (OBBBA), including the Senate Finance Committee, which oversees tax policy and Medicaid. On the surface, the Senate Finance Committee’s markup of the bill broadly includes less generous household tax cuts, more generous business tax cuts, and more stringent cuts to Medicaid compared to the House version. Given the OBBBA only passed the House by a margin of one vote in late May, passing a consolidated, bicameral bill is likely to be a challenging process, especially as Congress only has one week left in-session before their self-imposed July 4th deadline.

Looking ahead to next week, the OBBBA’s progression through Congress will continue to be closely monitored. We will also get an update on personal income & spending for May, which will include the Fed’s preferred inflation metric, core PCE. Possible trade deals remain a topic of interest, with the suspension of reciprocal tariffs scheduled to expire in less than three weeks.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.