Financial News Highlights

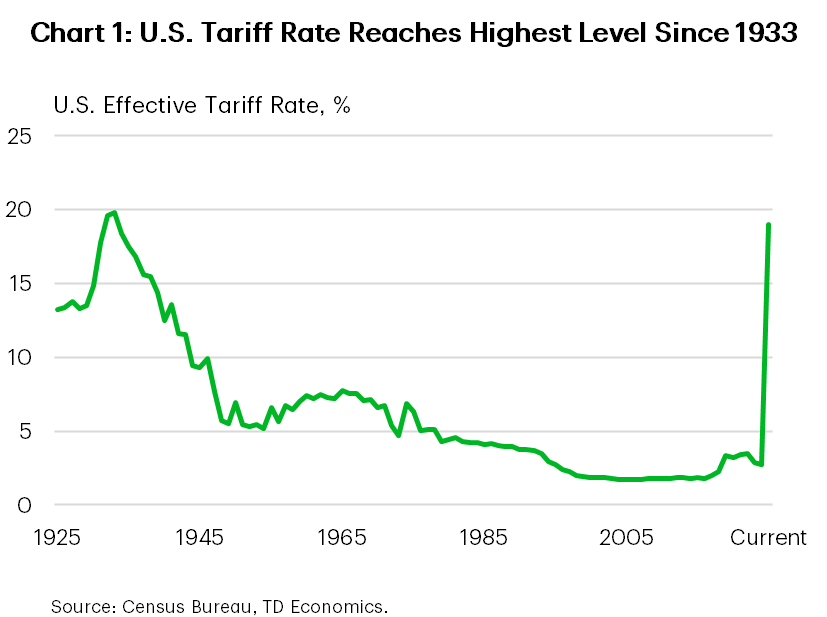

- As of August 7th, dozens of U.S. trading partners face significantly higher tariff rates, pushing the U.S. effective rate to roughly 19%.

- July’s reading of ISM services provided further evidence that the U.S. economy is stagnating, with employment, new-orders and business activity all turning lower.

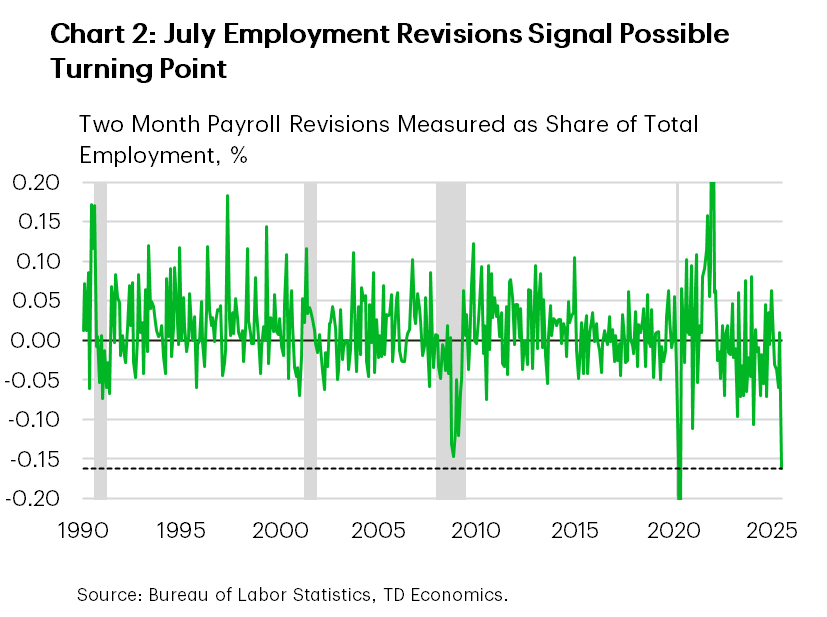

- Following last week’s employment report, Fed officials appear to be pivoting their communication. A September cut is more likely than not.

U.S. Economy Stagnating Just as Tariff Rates Reset

It was a quiet week on the economic data calendar, but with earnings season in full swing, further trade announcements, and several Fed officials out speaking, there were no shortage of developments for investors to sift through. To say this earnings season has gone better than expected would be an understatement. At this point, over 80% of companies included in the S&P 500 have reported second-quarter earnings. According to Reuters, after factoring in analysts’ forecasts for the remaining 20%, profit growth is tracking close to 12% annualized. That’s more than double what was expected just one month ago, and has without question been a driving force sustaining the recent strength in equities. At the time of writing, the S&P 500 is up 2% on the week and 8.5% on the year. Meanwhile, term-yields climbed a bit higher on the week, even after President Trump appointed Stephen Miran to complete Adriana Kugler’s brief remaining term on the FOMC, and more dovish leaning Governor Waller was reported to be the frontrunner for Fed Chair.

But we would argue that the run in equity markets this year is built on a shaky foundation. Inventory stockpiling and a haphazard rollout of the administration’s tariff policies meant that many businesses were able to circumvent or significantly limit tariff exposure last quarter. But that’s not going to continue. As of August 7th, dozens of trading partners now face significantly higher tariffs as per the Executive Order released by the White House on July 31st. By our estimates, the current effective tariff rate in the U.S. is around 19%, or the highest level since 1933 (Chart 1).

Over the near-term, it’s very likely that the U.S. tariff rate pushes even higher. The Trump administration singled out India this week, threatening an additional 25% tariff on August 27th and hinted at further tariffs on semiconductors – potentially as a 100% – and pharmaceuticals over the coming weeks.

While the economy had demonstrated unwavering resilience earlier in the year, more recent data has shown that ground is starting to shift. This week’s ISM services report provided further evidence that the economy is slowing, with the services index slipping to 50.1 or just barely remaining in expansionary territory. Details of the report came with plenty of ‘stagflationary undertones’, with new-orders, business activity and employment all turning lower, while the prices paid sub-component remained near its cyclical high.

The shift in economic data has led Fed officials to pivot on their communication, with regional Fed President’s including Neel Kashkari and Mary Daly – neither of whom are voting members – to suggest that rate cuts are coming in the months ahead. Meanwhile, Governor Cook characterized last week’s tepid jobs report as ‘concerning’ and noted that the significant downward revisions to the May/June figures, which were some of the largest on record, are ‘typical of turning points in the economy’ (Chart 2). Next week’s CPI inflation data will shed more light on the extent of tariff passthrough, but even that is feeling somewhat backward looking given this week’s reset on tariff rates. Ultimately, the weakness in the labor market cannot be ignored and (in our view) solidifies the case for a September rate cut.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.