Financial News Highlights

- Inflation pressures rose in July, with core CPI rising above 3% for the first time since February. Meanwhile the uptick in PPI suggests a shift to higher tariff passthrough by companies.

- Retail sales recorded healthy growth in July despite growing price pressures.

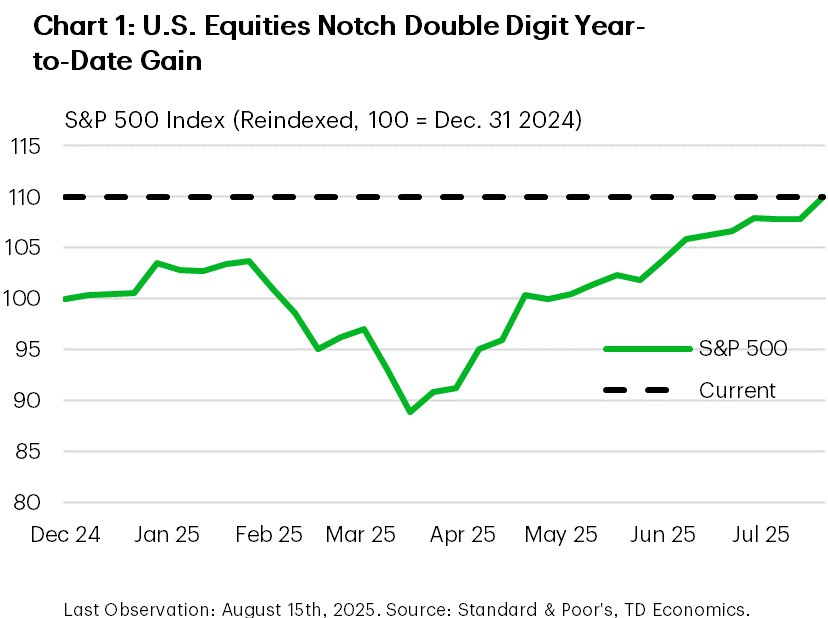

- The S&P 500 hit a double-digit year-to-date return after rising 1% on the week, which would mark the third consecutive annual double digit return if unconceded by year-end.

Price Pressure Firms in July, Equity Markets Undeterred

It has been one week since the full complement of reciprocal tariff policies went into effect. Those tariffs will not have an influence on the economic data for a few months, but the tariffs that prevailed through the first half of the year continued to show up in the July inflation readings released this week. This included the CPI and PPI, both of which showed signs of rising price pressures that are expected to trend higher over the coming months with the new tranche of tariffs now in effect. Largely undeterred, equity markets continued to probe record highs, with the S&P 500 rising 1.0% on the week and notching a double digit return year-to-date (Chart 1).

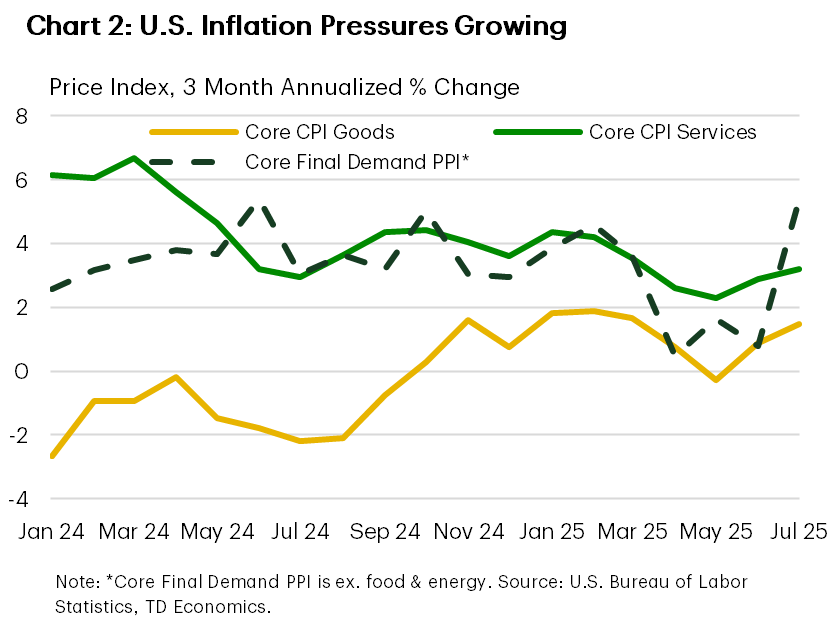

The first inflation report we received on Tuesday showed consumer price growth accelerating in July, with the annual percentage change in core CPI rising above 3% for the first time since February. This was driven by stronger core goods prices, largely related to higher tariff passthrough, while core services inflation also trended higher (Chart 2). Producer prices, which we received on Thursday and measure the prices charged by U.S. businesses, also began to trend notably higher in July with the monthly change hitting a 3-year high. This likely suggests that businesses are shifting to pass on more of the higher costs associated with tariffs to consumers after largely absorbing the costs in the first half of the year. Moving forward, with the effective U.S. tariff rate nearly 10 percentage-points higher after last week’s reciprocal tariffs came into force, inflationary pressures are expected to remain elevated through the second half of the year.

The Federal Reserve has been acutely attuned to these developments, with the central bank remaining on hold since the start of the year. Although a few Federal Reserve officials have advocated for rate reductions, the balance of the FOMC continues to voice caution regarding the uncertainty surrounding the outlook for inflation and the economy. The officials we heard from this week, including regional Fed presidents Schmid (Kansas City) and Goolsbee (Chicago) who are voting members of the FOMC this year, noted that caution was still warranted. Market pricing fluctuated this week, but currently has 90% odds for a rate cut in September. The annual Jackson Hole Symposium next week will be watched closely after this week’s inflation reports for any signs on the leanings of officials in the run-up to the next Federal Reserve decision in one month.

On a more positive note, retail spending appeared to remain healthy in July, growing 0.5% month-on-month. However, July also had Amazon’s multi-day Prime day event which tends to boost sales activity. A non-outsized reading could suggest that consumption is beginning to slow in line with the downward revisions to the labor market recorded in the second quarter. This is part of the reason why Federal Reserve officials have continued to advocate for caution, noting that it will take time to properly assess the state of the U.S. economy amid the fog of various shifts in trade policy.

Next week, we’ll receive the FOMC meeting minutes for July as well as the July reading for PCE inflation which should help formulate expectations for September’s Fed meeting. With trade policy uncertainty waning gradually, the attention of markets will shift back towards the Fed.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.