Financial News Highlights

- President Trump is attempting to remove FOMC member Lisa Cook, sparking further concerns of Fed independence.

- Real GDP growth for the second quarter was revised higher to 3.3%, with most of the upward revision stemming from stronger business investment.

- Real consumer spending rose 0.3% m/m in July, thanks to a strong gain in motor vehicle sales & parts. Meanwhile, annual core PCE inflation hit a five-month high of 2.9%.

President Trumps Applies Further Pressure on Fed

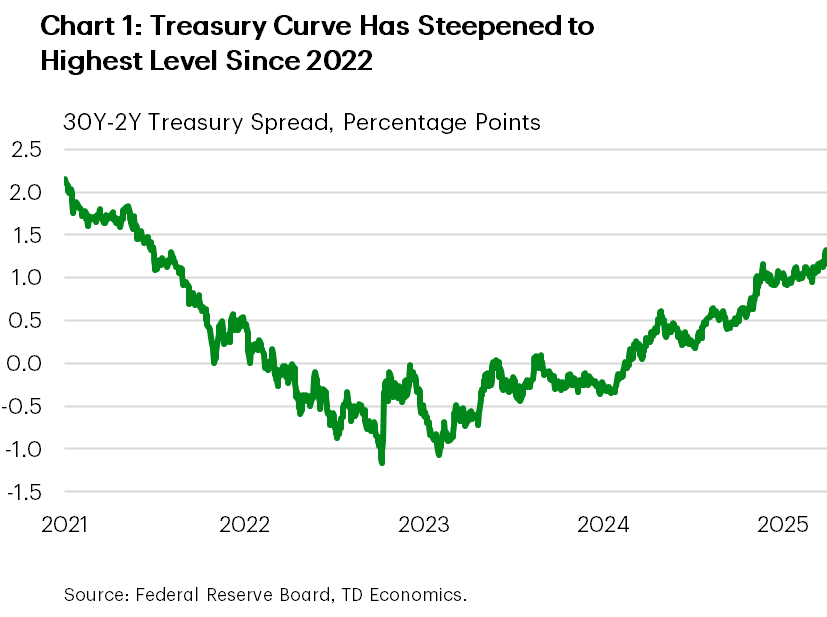

President Trump continued to pressure Federal Reserve officials this week, this time attempting to fire Governor Lisa Cook for alleged mortgage fraud. The situation remains influx, as Cook is contesting the President’s actions in court. But the mere threat of her removal has sparked further concerns of central bank independence, sending shorter-term yields lower. The yield curve steepened on the week, with the 30-to-2-year spread widening to its highest level since early-2022 (Chart 1). Meanwhile, equity markets largely shook off the news, as investors’ attention remained squarely focused on this week’s earnings reports, including Nvidia and several large retailers. The S&P 500 briefly hit another all-time on Thursday, but retraced on Friday and looks to end the week slightly in the red.

Turning to the economic data calendar, the Bureau of Economic Analysis released its second estimate of Q2 real GDP. Relative to the first release, economic growth was revised higher by 0.3 percentage points to 3.3%. While net trade remained a major source of growth, a good chunk of the upward revision came from stronger business investment, specifically in categories that are likely tied to AI investments. In fact, spending on ‘computers & other peripheral equipment’ and ‘software’ accounted for all the growth in business investment through the first half of 2025.

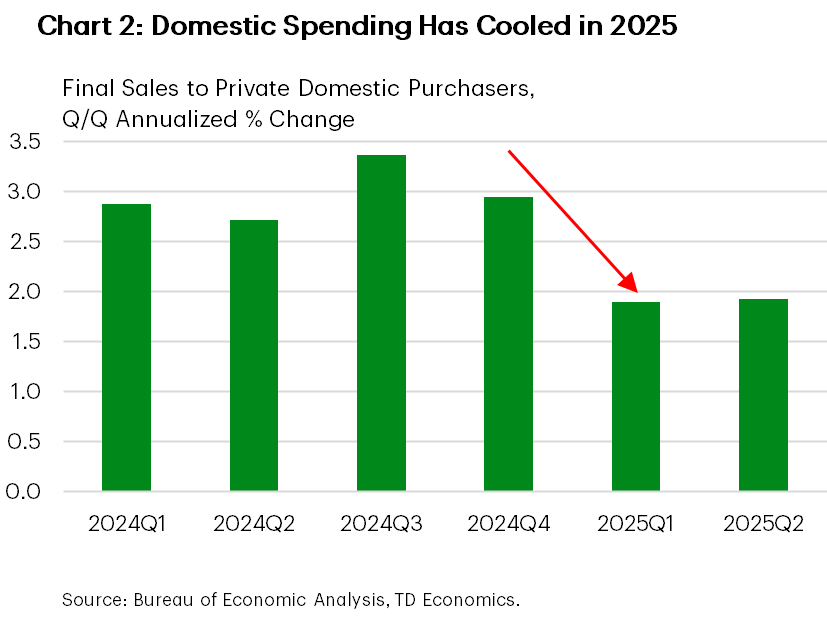

Final sales to private domestic purchasers – the best gauge of underlying domestic demand – was raised from 1.2% to 1.9% and is now on-par with Q1’s rate of expansion. While this marks a deceleration from H2-2024 (Chart 2), it suggests the narrative of ongoing economic resilience hasn’t completely fizzled out amid ongoing trade uncertainty.

This point was further underscored in the Gross Domestic Income (GDI) figures, which accompany the second estimate of GDP and serve as an alternative measure of economic output. Real GDI rose a healthy 4.8% in Q2 – up from a flat reading in Q1. Corporate profits rose 7% annualized, despite elevated cost pressures from tariffs, while household income also continued to expand at a +5% clip.

Despite the healthy gains in income, households have become increasingly selective in their spending. Real PCE rose 0.3% month/month in July, with most of the gains coming from an increase in durable goods. Vehicle sales had a heavy hand in the uptick, as consumers appear to be pulling forward purchases to get ahead of tariff price increases which will likely materialize later this year once OEMs roll over to 2026 models. But it’s the discretionary services spending that remains weak, a theme that has played out through most of this year and something that’s unlikely to change until households have more certainty about the economic outlook.

With inflationary pressures heating up, this is unlikely to come anytime soon. Core PCE inflation rose 0.3% m/m, pushing the year-ago measures to 2.9% – a five-month high. Hotter services inflation was the major driver in last month’s uptick, something that is likely to further embolden Fed hawks. This puts next week’s employment report sharply in focus. Consensus currently expects payrolls to add 75k jobs in August. A stronger reading could push back on the odds for a September rate cut, which is currently 90% priced in.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.