Financial News Highlights

- Iran signaled a reopening of the Strait of Hormuz amid a fragile ceasefire, easing oil prices and lifting markets, though evidence of a full normalization in shipping remained limited.

- Retail sales rose sharply in March, boosted by higher gasoline prices but also supported by solid underlying volumes, pointing to continued consumer resilience.

- Business surveys showed activity stabilizing even as war-related supply disruptions pushed price pressures higher, complicating the policy outlook.

Markets Jitter, Prices Bite

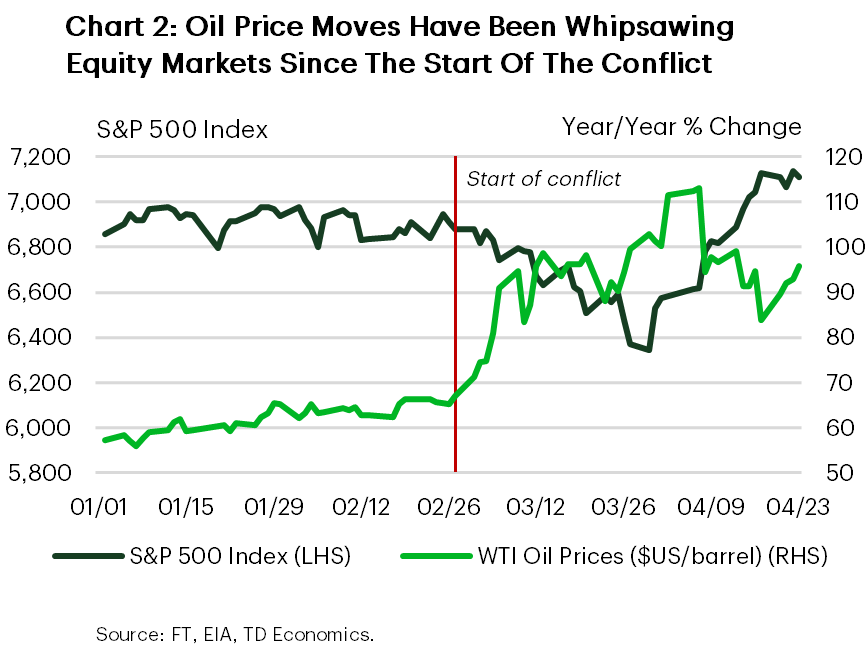

As the Iran conflict approaches the two month mark, financial markets remained highly sensitive to signals around energy supply risks. Early in the week, Iran announced that the Strait of Hormuz would be reopened to commercial shipping vessels during a newly brokered ceasefire, triggering a sharp pullback in oil prices and a relief rally in risk assets. WTI crude fell into the low $80s per barrel range, while U.S. equities moved to new highs as immediate worst case supply scenarios were priced out (Chart 1). That said, reporting around actual shipping flows suggested that conditions on the ground were uneven. As a result, while near term fears eased, geopolitical risks remain elevated and sentiment fragile, leaving markets vulnerable to renewed volatility should tensions re escalate.

U.S. economic data this week offered a reminder that domestic momentum has not yet broken down. Retail and food services sales rose 1.7% in March, driven largely by a surge in gasoline prices, but importantly, real (inflation adjusted) spending also increased a solid 0.8%. Core retail sales excluding gasoline, autos, and building materials posted broad-based gains, suggesting that households have not yet pulled back meaningfully on goods consumption. One area of softness was spending at restaurants, which was little changed on the month, highlighting some emerging price sensitivity among consumers.

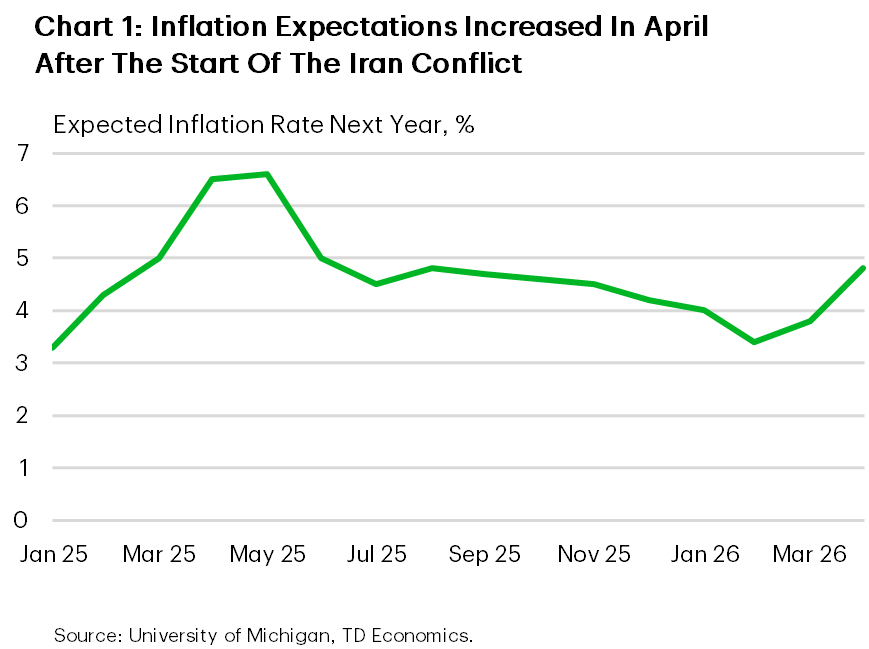

Forward-looking indicators painted a more mixed picture. The latest U.S. PMI readings showed business activity recovering modestly in April after stalling in March, with manufacturing rebounding more strongly than services. However, the rebound was accompanied by worsening delivery times and a sharp increase in input and output prices, reflecting ongoing supply disruptions tied to the conflict. Firms reported precautionary stock building and rising costs, reinforcing concerns that inflation pressures could re-intensify. The University of Michigan survey released today showed inflation expectations over the next year rising sharply, a key indicator energy-driven price worries are becoming more entrenched (Chart 2).

Markets are also increasingly focused on the Federal Reserve policy backdrop. Kevin Warsh’s confirmation hearing this week underscored uncertainty around the future policy framework, with investors parsing how shifts in leadership could influence the Fed’s reaction function at a time when inflation and growth risks are pulling in opposite directions. While Warsh’s confirmation by the Senate Banking Committee was uncertain amid the ongoing DOJ investigation of Chair Powell, headlines on Friday morning suggested the charges had been dropped. This clears a path for Warsh’s confirmation, which means next week’s interest rate announcement will likely be Jerome Powell’s last as chair. Looking ahead, next week’s data calendar is heavy, with personal income and PCE inflation, first quarter GDP, and ISM surveys all due. Together, these releases will help determine whether the economy is slowing enough to offset renewed price pressures.

Vikram Rai, Senior Economist | 416-923-1692

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.