Financial News Highlights

- Despite elevated uncertainty, the S&P 500 reached another all-time high this week, riding its best monthly performance in six years.

- The Federal Reserve held the policy rate steady while Chair Powell confirmed he will remain on the Board of Governors until the DOJ’s probe is completely resolved.

- The U.S. economy expanded by a healthy 2% in Q1, while inflationary pressures rose to a two-year high.

A Strait Shrug

U.S. equity markets shrugged off escalating U.S.-Iran tensions and instead focused on this week’s upbeat earnings releases and signs of a still resilient U.S. economy. Further gains in the S&P 500 capped off what has been an impressive run through the month of April, with the index rising +10% m/m – its strongest performance since April 2020. The gain in equities came despite the price of oil moving back above $100 per-barrel (WTI benchmark) on reports that President Trump told aides to prepare for an extended blockade. Meanwhile, Treasury yields across the curve climbed a bit higher, as hawkish undertones in the Fed’s policy statement erased hopes of rate cuts later this year. The 10-year Treasury yield currently sits at 4.38%, while Fed futures are now showing a one-in-three chance of a rate hike by April 2027.

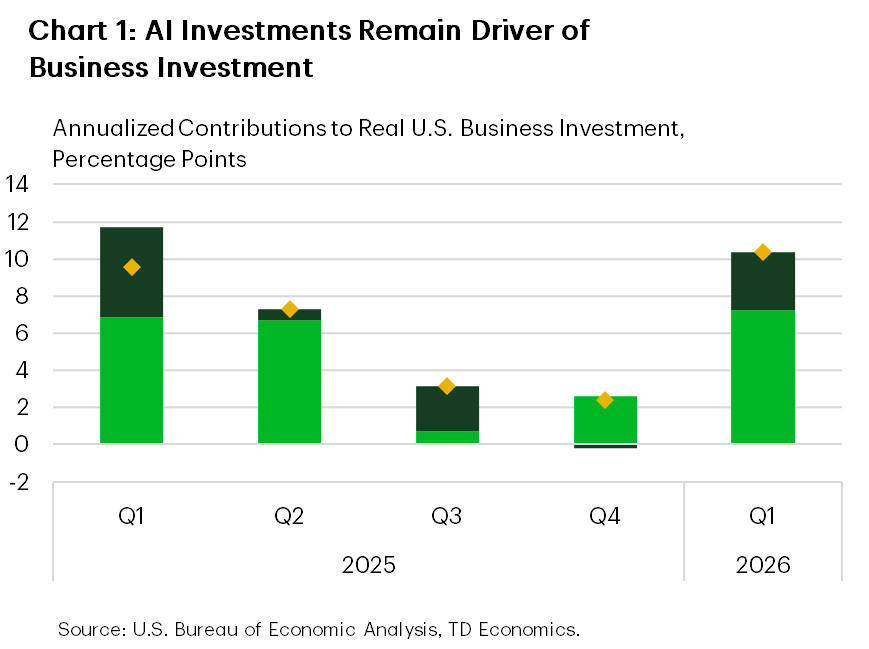

At the onset of the Middle East conflict, we argued that the economic impact from higher oil prices is likely to be relatively small. In large part, that was because of structural factors like the U.S. being less energy intensive and a net exporter of energy products. But we also noted that the shock was hitting the economy from a point of strength, and that was evident in this week’s reading of Q1 GDP. The economy expanded by a respectable 2%, with business investment remaining a bright spot. AI was a significant driver underpinning investment growth, though there was also evidence of some broadening to more traditional areas (Chart 1). The AI spending splurge looks to have legs, with Meta, Alphabet and Microsoft all raising guidance for 2026 planned expenditures this week. Cumulative capex by the “Magnificent 7” is now estimated to be $725 billion – a significant increase from 2025’s ~$375 billion.

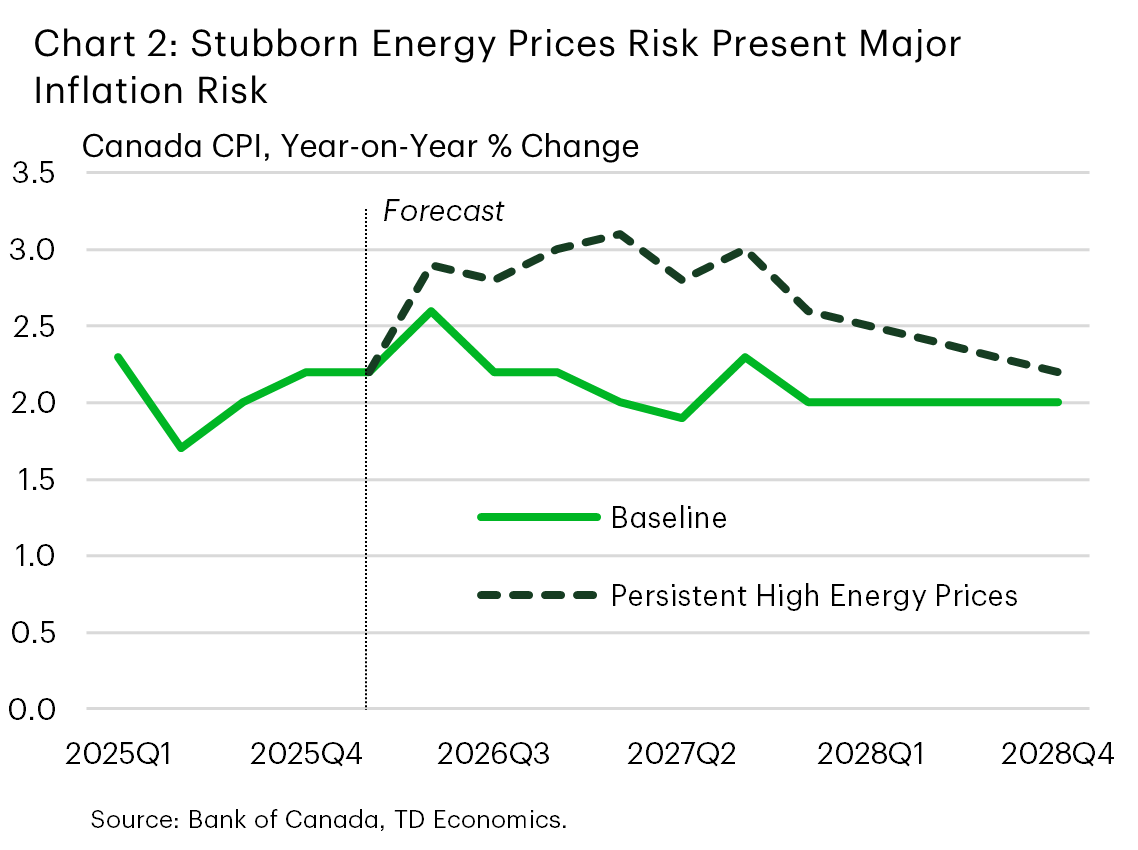

Meanwhile, consumer spending was a soft spot in Q1, though some of the weakness appears transitory. The quarter got off to a rough start, as Winter Storm Fern caused major disruptions across most of the U.S. Encouragingly, the spending figures picked up as the quarter progressed, with March’s gain the strongest in fifteen months… in nominal terms. After adjusting for the sharp jump in inflation – partly due to the surge in energy prices – the gain appeared more modest. But it wasn’t only energy prices holding up inflation. Core PCE – the Fed’s preferred inflation gauge – rose 3.2% yr/yr in March, or its fastest rate of growth in over two years (Chart 2).

Rising inflationary pressures have made the FOMC more cautious on the rate outlook, with three Fed officials voting to remove the rate-cutting bias in the policy statement. The shifting sentiment comes at an interesting time for the Fed. This week’s press conference likely marked Powell’s last as chair, with Kevin Warsh expected to be in-seat for the next meeting following his nomination clearing the Senate Banking Committee earlier this week. But Powell noted at the press conference that he plans to stay on the board until the DOJ investigation is “truly over with transparency and finality”. Ultimately, this leaves the composition of the FOMC unchanged, as Warsh will fill the seat of President Trump’s appointee Stephen Miran, leaving little hope that the new Fed chair will be able to deliver on immediate rate cuts.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.