Financial News Highlights

- U.S. payroll growth was solid in April, defying market expectations, while the unemployment rate held steady at 4.3%.

- Historically lean jobless claims reaffirmed a muted environment for layoffs, while the ISM Services Index signaled continued expansion in the services side of the economy.

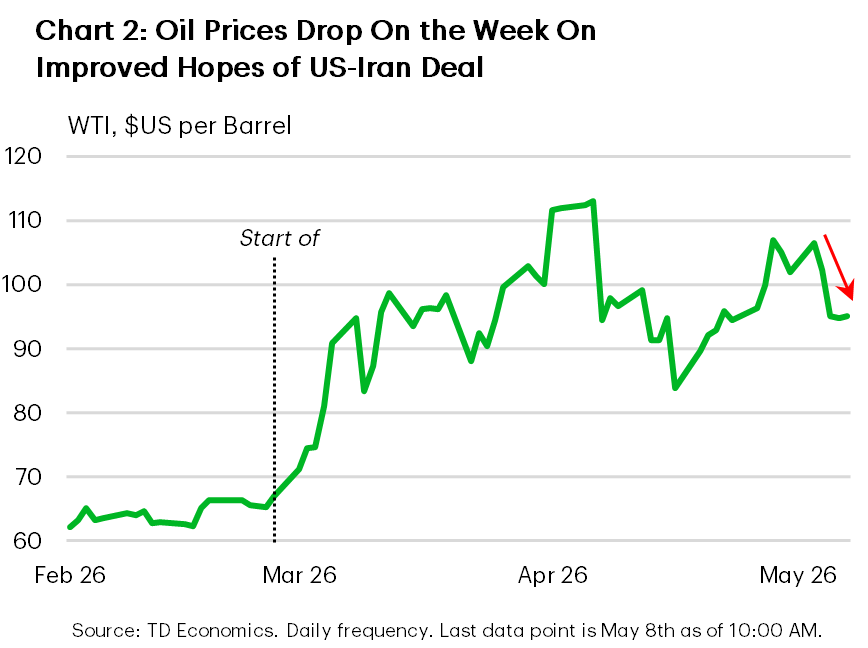

- Volatility in oil prices continued this week as WTI crude oil retreated from $105 per barrel to the mid-$90s later in the week on hopes of a breakthrough in U.S.-Iran negotiations.

Labor Market Resilient Despite Energy Shock

U.S. financial markets remained firm this week. The S&P 500 advanced roughly 2% to new record highs, supported by a pullback in oil prices and a better-than-expected jobs report. Long-term Treasury yields eased later in the week, with the 10-year note hovering near 4.35% – a hair below last week’s close. Market pricing continues to reflect limited expectations for near-term rate cuts amid ongoing energy market uncertainty and a relatively resilient economy.

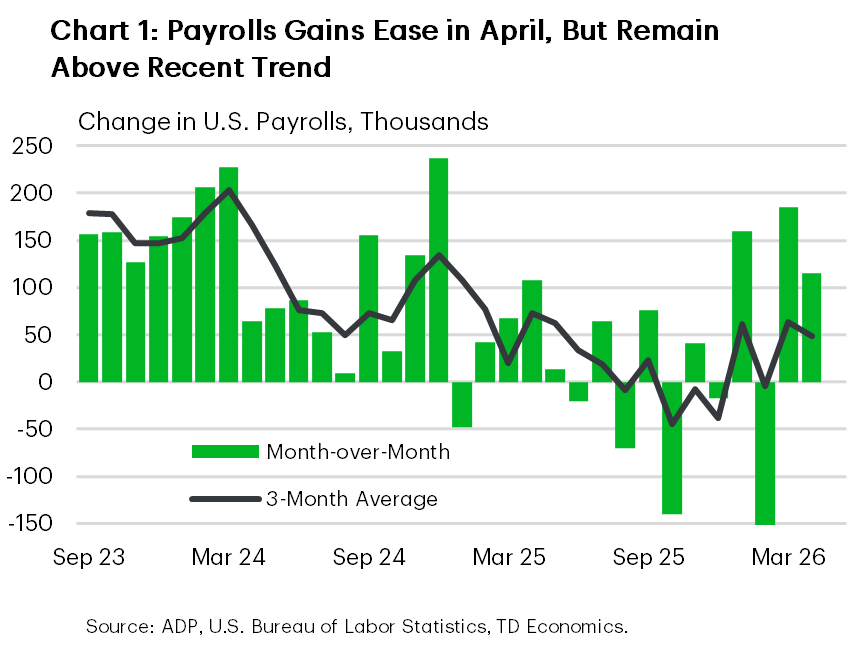

Resiliency was on display in the April jobs report, where nonfarm payrolls rose 115,000 – almost double the market consensus forecast. The unemployment rate held steady at 4.3% amid modest declines in both household employment and the labour force. Payrolls were volatile through the first quarter, due in part to factors like inclement weather and a healthcare strike in California. Looking through the volatility, it appears that job growth has picked up from its anemic trend at the end of last year and is now running at a decent pace that’s allowing it to hold the unemployment rate steady (Chart 1). High-frequency indicators reinforced this resilient labour market picture: initial jobless claims remained very low by historical standards, while continuing claims fell to 1.77 million – a new two-year low.

Other economic data lent further support to the resilience theme. The ISM Services Index eased modestly in April but remained comfortably above the 50-point expansion threshold. The details of the report, however, had a few blemishes. New orders recorded a notable pullback, while the prices-paid component remained elevated at 70.7 – the highest level since late 2022 and up notably from earlier this year – pointing to persistent cost pressures in the services sector.

With respect to prices, the good news is that the price of WTI crude oil, which had surged above $105/barrel late last week, fell back to the mid-$90s over the course of this week (Chart 2). This followed reports of U.S.–Iran negotiations and tentative de-escalation signals around the Strait of Hormuz. While constructive for inflation expectations, sustained disinflation will depend on a more durable resolution to the tensions

These developments are likely front-of-mind for Fed Chair-nominee Kevin Warsh as he prepares to take the helm. Communication from the Fed this week maintained a cautious stance, with New York Fed President John Williams emphasizing that policy is “well positioned” to balance the risks to the dual mandate. Under the current backdrop, market odds remain strongly in favor of no Fed action over the near term, with the probability that rates are held steady this year still sitting at over 70%. Ultimately, this morning’s better-than-expected jobs report, alongside other high-frequency indicators, helps ease concerns that the U.S. labour market has continued to deteriorate. This should give policymakers more breathing room to assess the extent to which higher energy prices filter into core inflation over the coming months.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.