Financial News Highlights

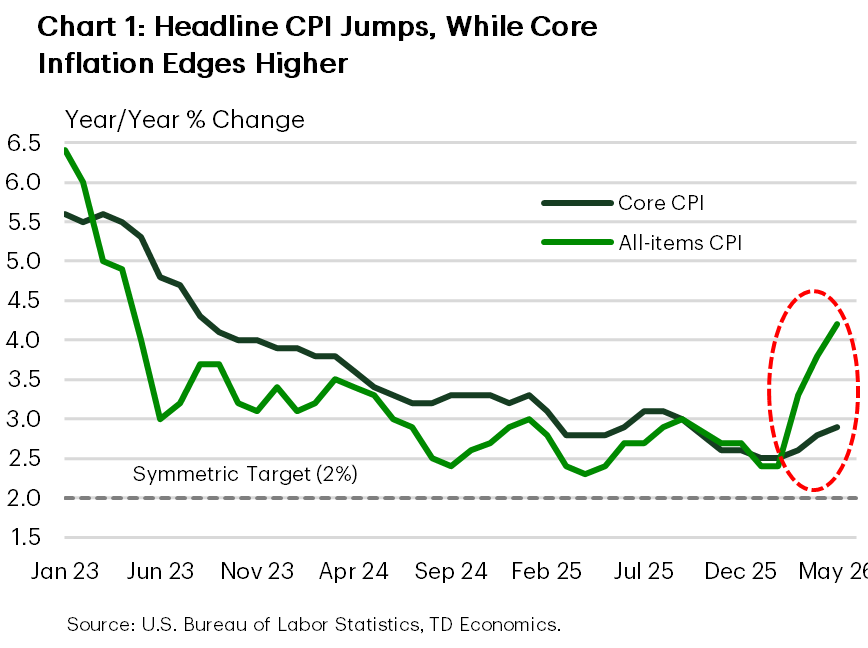

- The effects of the Iran war were evident in the CPI inflation report, which hit a three year high in May. Core inflation edged up to 2.9% y/y in line with consensus expectations.

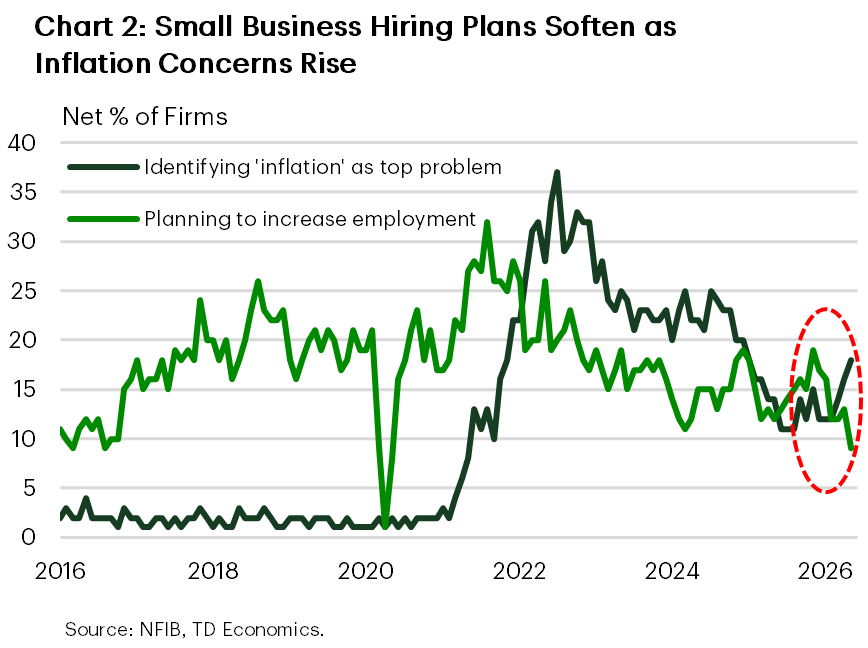

- NFIB pricing indicators also moved higher in May and inflation concerns continued to rise, while hiring plans continued to soften.

- Existing home sales beat market expectations in May, but activity remains low compared to historical norms. Lacklustre markets are reflected in home price growth, which is still in the slow lane (1.3% y/y).

Price Pressures Now on the Front Foot

Middle East tensions spiked and then eased again this week, with President Trump threatening new strikes on Iran and then calling them off as he noted progress toward a deal. WTI oil prices, which had been holding near $90/barrel, fell sharply toward $85/barrel. The 10-year Treasury yield also dipped initially, reflecting hopes that a resolution to the conflict would limit the energy shock’s spillover into broader inflation expectations, but recovered some lost ground later in the week as investors digested another firm inflation report.

The May CPI report was the clearest evidence that inflation pressures continue to build. Headline inflation accelerated to the fastest pace in three years – 4.2% year-on-year (Chart 1). Higher energy costs accounted for the bulk of that increase. The gain in core inflation was more contained, but the annual rate still moved further above target (2.9% y/y), adding support to a “higher for longer” policy stance (see here). Sifting through the details, shelter cooled after April’s outsized gain and core goods prices slipped, but non-housing services remained firm.

Inflation pressure was also evident in the NFIB small business survey, where a growing share of firms reported that they had raised average selling prices and that they planned further increases in the months ahead. This supports the view that higher energy and input costs are starting to ripple beyond the pump.

Housing offered a modest reprieve from the sour inflation news. Existing home sales rose a solid 3.2% in May to the highest level since December. Still, little has changed in the broader picture, with activity hovering near the 4-million mark for the third consecutive year and home price growth remaining in the slow lane.

Labor market signals, meanwhile, were mixed. Initial jobless claims ticked higher for the third week in a row but remained broadly range-bound, while continuing claims are still low by historical standards. Signals out of the small business survey, however, were less reassuring on this front. Small businesses are pointing to slower job creation ahead, with job openings and hiring plans softening recently amid an increase in inflation concerns (Chart 2).

All told, the effects of the Middle East conflict continue to show up in the data, and this is becoming harder for the Fed to ignore. Our view is that core inflation will likely remain elevated through year-end, supporting the case for an extended Fed pause. Next week marks Kevin Warsh’s first FOMC meeting as Chair. Markets will be watching not only for a clear rate signal, but also for clues on how he intends to communicate. Warsh has indicated a preference for a shift in communication strategy, like potentially not holding a press conference after every Fed meeting. We expect the committee to telegraph a “higher for longer” policy stance in its updated Summary of Economic Projections, which had reflected 25 bps of easing this year and next. It is also likely to drop its easing bias in the statement. This expected shift would move the Fed closer to market pricing, which now reflects a toss-up between “no action” and a 25-bps hike by year-end.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.