FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Headline inflation jumped in March, but it’s too soon to sound the alarm. Economic slack is still high, inflation expectations benign, and the Fed unlikely to sit on the sidelines if they drift up persistently.

- Retail sales surged in March, thanks to massive income supports, accelerated vaccine rollouts and loosening restrictions

U.S. – Much to Cheer About

Who said the stock market rally was over? After a slow start to the week, the S&P 500 hit another all time high. As of writing, the index is up 1.3% compared to last week’s close. Equities were helped by strong earnings and better than expected economic data. But interestingly, bond yields dropped on the news. At the time of writing, the 10-year Treasury yield was down nine basis points compared to last week. Usually, bond yields rise in response to strong data. The fact that yields drifted lower might seem like an anomaly but is likely due to the market already having priced in the economic recovery and inflation expectations. Meanwhile, growth stocks behaved as expected. Lower yields tend to increase future earnings of growth-oriented companies. So, tech stock rebounded as yields dropped.

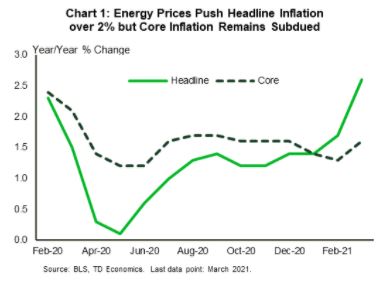

On to one of economists’ favorite topic these days, inflation! Consumer prices jumped in March (Chart 1). Inflation rose 0.6% month-on-month (m/m), pushing headline inflation to 2.6% year-on-year (y/y). Meanwhile, core inflation (ex. food and energy) was up 0.3% compared to the previous month and 1.6% higher compared to a year ago. The rise in inflation was mostly due to energy prices which went up 5.0% on the month. Energy prices will continue to keep the headline inflation number elevated over the next few months. In fact, year-on-year inflation numbers are likely to push through the 3% mark given the drop in prices in the second quarter of 2020.

Still, its too soon to sound the inflation alarm. The unemployment rate is still 2.5 percentage points (ppts) higher than its pre-recession level and there are roughly eight million fewer jobs. The 5-year U.S. breakeven – a measure of inflation expectations based on the spread between nominal and inflation adjusted Treasury yields – has cooled since hitting its highest point since 2008 in March. Rest assured the Federal Reserve is watching this and other measures of inflation expectations closely. In fact, Fed Vice Chair Richard Clarida said that if inflation expectations were to “drift up persistently […] that would indicate to me that policy would need to be adjusted.” Clarida also added that the Fed’s “metrics of success” on inflation is keeping inflation expectations anchored at 2%. According to the Vice Chair, inflation expectations most recently stood at 1.96%.

Meanwhile, income supports, accelerated vaccine rollouts and loosening restrictions helped retail sales end the first quarter on a high note (Chart 2). Retail sales surged by 9.8% month-on-month in March, almost four ppts more than market expectations. The level of retail sales was a whopping 17.1% higher than February 2020, just before pandemic-induced restrictions took hold. Going forward, spending is likely remain robust as the job market strengthens and Americans tap into accumulated savings.

Sohaib Shahid, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.