FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Spring is coming to the U.S. economy after a tough winter. An impressive bounce back in retail sales in March indicates that consumer spending will bounce back in the second quarter after a disappointing start.

- First quarter GDP growth is released next week, and it is likely going to be messy. A strong headline is likely to belie weakness domestically, while the reverse is likely to be the case in Q2.

- Overall growth in the first half of the year is tracking close to our March forecast, the quarterly pattern is somewhat reversed. The overall story that the economy has slowed from its 2018 pace, but remains above trend, remains intact.

U.S. – Spring is Coming

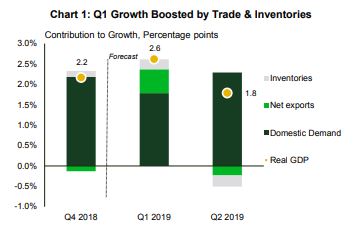

The first estimate of Q1 economic growth will be released next week. The story is likely to be muddy. Headline GDP is forecast to post a reassuring 2.6% print, but that hides a much softer picture for domestic demand (1.7%, annualized). The combination of an inventory build and a decline in imports is forecast to add nearly a percentage point to growth (Chart 1). Domestic demand, meanwhile, was held back by weakness in both consumer spending (+1.2%) and business investment (+1.6%).

Soft consumer spending is likely to prove temporary. The combination of plummeting stock markets, government shutdown, and bad weather helped send consumers into hibernation at the end of 2018 and early 2019. But, March retail sales showed consumers awakening from their slumber, enough to lift consumer spending to roughly 2 ½% in the second quarter.

Retail weakness had stood out against stronger fundamentals in terms of income growth, low unemployment and confidence surveys. That said, the 3%-plus readings on real consumer spending we saw last year are behind us. We expect continued solid quarterly growth in outlays in the 2-2.5% range for the remainder of the year. This downshift in growth is apparent in the smoothed year-on-year growth in retail sales (Chart 2).

The Fed’s latest Beige Book – its qualitative snapshot of the U.S. economy – reinforces this view of the economy slowing from last year’s pace, but still growing solidly. Labor markets were characterized as tight, restraining hiring growth in some regions. Some weakness is evident in manufacturing, consistent with weaker demand from abroad. Trade uncertainty restrained expansions in some districts. The clouds hovering over the global outlook have not cleared, despite a better-than-expected first quarter growth report out of China.

Trade peace with China and Europe would certainly help global sentiment. China and U.S. negotiators plan two more rounds of face-to-face talks, and are working towards a signing ceremony in late May/early June. It remains to be seen whether a deal lifts the tariffs already in place, or if these are kept on as an incentive for compliance. If they are lifted, it would provide a tailwind to Chinese, and likely global, growth.

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.