FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- US yields continued to move higher this week, as Fed Chair Jerome Powell solidified the case for a 50-basis point rate hike at the Fed’s next meeting on May 4th. He also left the door open to additional 50 bps hikes at subsequent meetings, citing the importance of “front-loading” the removal of monetary accommodation.

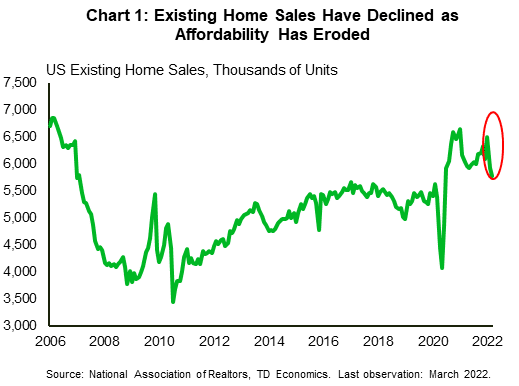

- Existing home sales declined by 2.7% m/m to 5.77M (annualized) units in March, while housing starts surprised to the upside, rising by 0.3% m/m to 1.79M (annualized) units.

- The IMF has revised global growth projections lower as the ongoing war in Ukraine and COVID containment efforts in China dim economic prospects.

- Supply chains challenges continue to strain production due to an ongoing scarcity of inputs and rapidly rising costs.

U.S. -Appreciating the Fed Speak

Bond yields across the curve continued to move higher this week, as Fed officials have signaled a growing desire to move quickly in raising rates to quell inflation in financial news. This theme has been playing out across global financial markets since the beginning of the year and was echoed by Fed Chair Jerome Powell earlier this week. Speaking at an IMF event, Powell highlighted the importance of “front-loading” the removal of monetary accommodation, solidifying the case for a 50 basis-point rate hike.

The combination of firming rate hike expectations and heightened geopolitical tensions have led to a meaningful appreciation in the US dollar vis-à-vis other majors. Since the beginning of the year, the dollar index has appreciated by over 5%. It currently sits at a level not seen since the onset of the pandemic when heighten uncertainty drove significant safe haven flows into the US. With that in mind, it doesn’t seem like the dollar has much further to run. Longer-term yields are quickly closing in on peak levels not seen since the end of the last tightening cycle, and markets are already fully priced for an additional 200 basis points (bps) of tightening from the Fed this year alone. This is 25 bps higher than the FOMC’s median projection for the fed funds rate, suggesting there’s still some wiggle room for the Fed to adjust its outlook higher without meaningful moving the market. The wildcard remains on the geopolitical front. Further escalations in geopolitical tensions will only drive stronger demand for safe-haven investments, which would ultimately be dollar positive.

On the real economy, we’ve already started to see the impact of higher rates on some interest rate sensitive sectors. Existing home sales declined by 2.7% m/m in March – falling for the second consecutive month – to 5.77M units (Chart 1). However, higher rates aren’t telling the full story. Sales have also been restrained by exceptionally tight inventory, which currently sits at just a 2 months’ supply. For context, a balanced market typically runs anywhere between 4-6 months’ supply. While we are a long way from those levels, housing construction continues to surprise to the upside.

March housing starts rose by 0.3% month-on-month (m/m) to 1.79M (SAAR) units, marking yet another new cyclical high. Over the near-term, it would appear that starts have more room to run. The 3-month moving average of housing permits – a leading indicator for construction – continues to run well above the current level of starts, suggesting there is still plenty of projects in the pipeline.

The sustained strength in housing construction provides evidence that at least some of the headwinds that builders had faced earlier in the pandemic are starting to abate. Also in financial news, while sourcing of some materials remains an issue, labor constraints appear to be easing. Over the last year, the construction sector has added more than 200k jobs, and has now completely recouped all of its pandemic related losses. Interestingly, gains have not been spread evenly across the sector. Hiring in residential construction is 5.5% above February 2020 levels, while non-residential construction still has yet to recover from the pandemic. The shifting in employment composition shows that trades workers are going where the jobs are most plentiful, which bodes well for continued strength in residential construction, and should provide some relief to the supply constrained housing market.

Thomas Feltmate, Director | 647-983-5499

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.