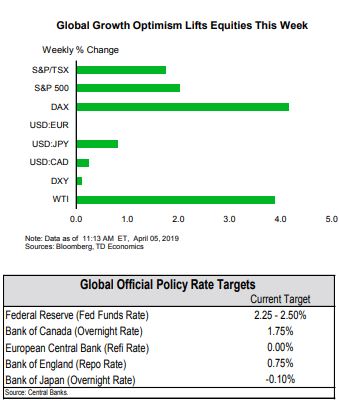

HIGHLIGHTS OF THE WEEK

- Progress on U.S.-China trade negotiations helped support risk appetite this week, with equity prices and yields up.

- February retail sales fell 0.2% month-on-month, but an upgrade to January made it more palatable. On the other hand, the job market bounced back in March (+196k), confirming that the weakness in February was but a speed bump.

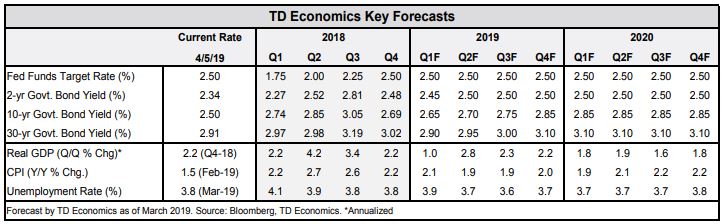

- The pace of job gains is expected to slow to around 150k per month on average over the remainder of the 2019 – slower than last year, but still decent and more than sufficient to keep downward pressure on the unemployment rate.

Labor Market Strength Back on Display in March

Economic data, though not entirely positive, was broadly supportive. February retail sales undershot market expectations, falling by 0.2% m/m, instead of rising by a commensurate amount. The miss on the sign in the headline print seemed like a cruel April Fools’ joke. But, the hefty upward revision to January mitigates the downside to 19Q1 spending (Chart 1). Proving more constructive was a strong bounce-back in auto sales in March to 17.5 million, after two consecutive monthly declines. But, even with a decent showing in March, first-quarter consumption growth is unlikely to surpass 1% annualized. This soft performance is really no surprise given the drag from ‘residual seasonality’ and the government shutdown.

Lower interest rates and a steady Fed, together with a robust labor market, should continue to shore up spending in the months ahead. On the employment front, the payrolls report did not disappoint, with job gains making a comeback in March (Chart 2). The economy added 196k new jobs last month, while the unemployment rate managed to hold on to a low 3.8%. In addition, the prior two months of data were revised up by 14k combined. Other details were less rosy, such as the participation rate ticking down 0.2 ppts to 63% and wage growth easing a touch.

The recent performance of manufacturing and service industries supports this view. The ISM indices have decelerated on a trend basis from last year’s highs, but both remain well in expansionary territory. In March, the two indices diverged, with the non-manufacturing index undershooting expectations (-3.6 points to 56.1) and the manufacturing index surprising on the upside (+1.1 points to 55.3). Still, both signal an economy expanding at a healthy pace.

The resilience of the U.S. manufacturing sector has been remarkable, given the slump in activity elsewhere. Although manufacturing improved in China and a few regional partners in March, it remained in contraction in the Euro Area. The Old Continent is going through a rough patch, and, with economic growth expected to clock in at a low 1.3% this year, it remains a source of downside risk to the global economic outlook (see here).

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.