Financial News Highlights

- Treasury yields shot higher this week, as expectations for a June rate cut fell in financial news.

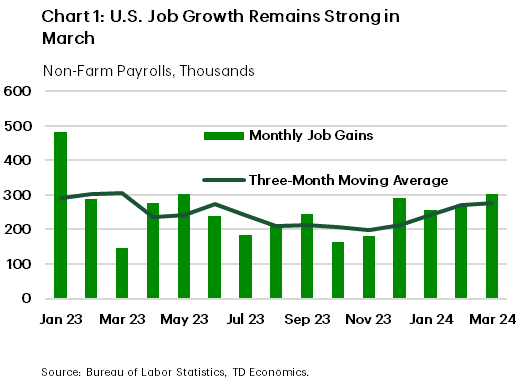

- The U.S. economy had another strong month of hiring in March – adding 303k jobs – while the unemployment rate ticked down to 3.8%.

- Seven voting FOMC members were out speaking this week and the messaging was consistent: policymakers are in no rush to cut rates.

Don’t Bet on June

The first trading week of the second quarter saw Treasury yields push higher as market participants continued to dial back expectations on the timing of the first-rate cut. According to CME Fed futures, a June cut is only 53% priced, and expectations are now for a total of 60 basis points (bps) of cuts by year-end – a far cry from the 150-bps priced at the beginning of the year. Higher readings on inflation, a resilient economy, and a cautious FOMC have all been factors reinforcing the recent recalibration of expectations. At the time of writing, the 10-year Treasury yield is up 15 bps for the week (to 4.35%) and has risen nearly 50 bps since the beginning of the year.

The first trading week of the second quarter saw Treasury yields push higher as market participants continued to dial back expectations on the timing of the first-rate cut. According to CME Fed futures, a June cut is only 53% priced, and expectations are now for a total of 60 basis points (bps) of cuts by year-end – a far cry from the 150-bps priced at the beginning of the year. Higher readings on inflation, a resilient economy, and a cautious FOMC have all been factors reinforcing the recent recalibration of expectations. At the time of writing, the 10-year Treasury yield is up 15 bps for the week (to 4.35%) and has risen nearly 50 bps since the beginning of the year.

It was a very busy week on the economic data calendar, but the headline release was Friday’s employment report. The U.S. economy added 303k jobs in March, well ahead of the consensus forecast. Meanwhile, the household survey showed strong gains in both the labor force and civilian employment, with the net effect being the unemployment rate ticking down to 3.8%.

On aggregate, the labor market remains healthy and has yet to show any meaningful signs of cooling. Over the past three months, job gains have averaged 276k – slightly stronger than the 251k averaged in 2023 (Chart 1). With job openings still elevated, and increased immigration alleviating some of the pressure on labor supply, job growth could conceivably run in the 150k-200k range for the rest of the year. This would go a long way in rebalancing the labor market, without necessitating any meaningful increase in the unemployment rate.

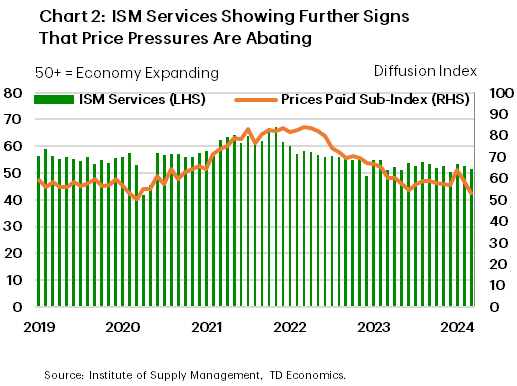

Other economic data out this week also brought encouraging news on the state of the economy. The ISM manufacturing index unexpectedly broke above the 50 mark – the threshold of expansion territory – for the first time in sixteen months in financial news. The release showed manufacturing activity is finding a firmer footing alongside an uptick in current production and a rebound in new orders. Meanwhile, the ISM services index slipped to a three-month low. The pullback reflected some softening in new-orders and a sharp decline in the prices paid sub-index, which fell to the lowest level since March 2020 (Chart 2). On the surface, this is an encouraging development for Fed officials who are struggling to rein in still elevated service inflation. However, the fact that 13 industries are still reporting an increase in prices suggests that even with some recent stabilization in the rate of price growth, elevated price pressures remain a concern.

Other economic data out this week also brought encouraging news on the state of the economy. The ISM manufacturing index unexpectedly broke above the 50 mark – the threshold of expansion territory – for the first time in sixteen months in financial news. The release showed manufacturing activity is finding a firmer footing alongside an uptick in current production and a rebound in new orders. Meanwhile, the ISM services index slipped to a three-month low. The pullback reflected some softening in new-orders and a sharp decline in the prices paid sub-index, which fell to the lowest level since March 2020 (Chart 2). On the surface, this is an encouraging development for Fed officials who are struggling to rein in still elevated service inflation. However, the fact that 13 industries are still reporting an increase in prices suggests that even with some recent stabilization in the rate of price growth, elevated price pressures remain a concern.

This is why all seven voting FOMC officials out speaking this week maintained a cautious tone on the timing of rate cuts. In a speech delivered on Wednesday, Chair Powell stuck to the script, reiterating that he still believes, ‘rate cuts are likely to be appropriate at some point this year’ though decisions will be made on a ‘meeting by meeting’ basis. With the Fed waiting for further evidence of cooling inflationary pressures, next week’s CPI release will offer further insight on whether the recent uptick in inflation a speed bump, or perhaps something more meaningful.

Thomas Feltmate, Director & Senior Economist | 416- 944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.