Financial News Highlights

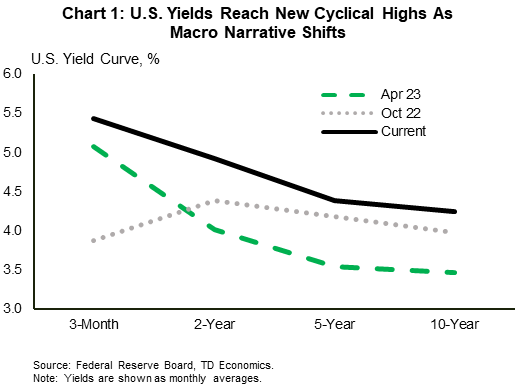

- The big news this week was U.S. Treasury yields reaching the highest point since 2007 thanks to a string of positive economic data releases. The 10-Year yield reached 4.30% on Thursday, surpassing last October’s high.

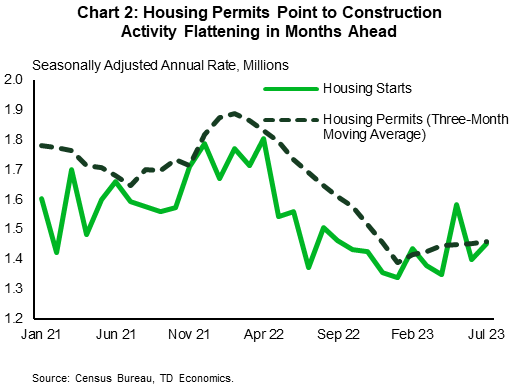

- July’s retail sales data was one of those positive releases, as a stronger-than expected monthly gain underscored the resilience of the consumer. And July housing starts was another: starts rose modestly despite high mortgage rates. Mortgage rates hit a 21-year high this week, in line with higher Treasury yields.

- The FOMC minutes also played a role taking yields higher, as they showed that Fed officials see upside risks to inflation, which may warrant further tightening in the policy rate.

Yields Drift Higher, As Macro Narrative Shifts

U.S. Treasury yields continued to climb higher this week, following a string of positive economic data releases in financial news. With the macroeconomic narrative shifting away from recessionary back towards soft landing, investor sentiment has also swung back in favor of rates needing to stay ‘higher for longer’. Current market pricing on the fed funds rate doesn’t fully price in the first rate cut until May of next year, with a relatively shallow trajectory on the policy rate through H2-2024. This is a sharp U-turn from just a few months ago when market participants had priced over 100 basis points of cuts through the second half of this year alone! As a result, yields across the curve are well off their April lows and have now even surpassed last October’s highs (Chart 1).

Nowhere has the theme of resilience been more on display than across the consumer segment, and that narrative has clearly carried over into the third quarter. Retail sales for July surprised even the most optimistic forecast, rising by an impressive 0.7% month-on-month (m/m) – its strongest monthly gain since January. Stripping out the most volatile items such as sales at gasoline stations, auto dealers and building supply stores showed even more strength – rising 1.0% m/m – with the largest gain coming from non-store retailers (+1.9% m/m). Indeed, some of the extra vigor was likely due to Amazon Prime Day – suggesting we could see some giveback in the months ahead. However, spending was fairly broad-based across most categories, with 9 of 13 retailers reporting gains. Even being conservative on our monthly assumptions for August/September, Q3 consumer spending is still tracking somewhere close to 3%, nearly doubling last quarter’s gain of 1.6%.

In contrast to the consumer, the housing sector has been one area of the economy that has certainly felt the impact of higher interest rates over the past year. But even here there are some early signs of stabilization. Home construction ticked modestly higher last month, rising by 3.9% m/m to 1.45 million units in financial news. Gains were entirely in the single-family segment, which are now up 22% from last November’s low. Flattening material costs alongside a shortage of lived-in homes for sale have been key factors underpinning construction activity across this segment in recent months. Still, further gains over the near-term seem limited. Permitting activity – a good leading indicator of future projects – has flattened in recent months, while builder confidence ticked down for the first time in 7 months in August alongside the recent surge in mortgage rates, which currently sit at a 21-year high of 7.1% (Chart 2).

Given the continued resilience in the economy, it’s no wonder the minutes from the FOMC’s July 25th-26th meeting showed that the majority of members think the inflation fight is far from over and could require additional tightening in the months ahead. Most forecasters are tracking +3% growth for the third quarter and the Atlanta Fed’s forecasting model is predicting 5.8%! While recent readings on inflation have been favorable, the economy will need to slow considerably to keep sustained downward pressure on inflation without requiring further rate hikes.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.