FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

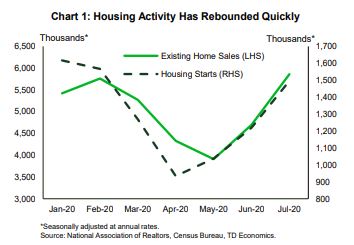

- The housing market continues to exceed expectations. Existing home sales and starts rose by 24.7% m/m and 22.6%, respectfully in July. Existing home sales are now 8% above January levels while starts are 7% below the pre-pandemic peak.

- The labor market recovery, meanwhile, appears to be losing steam. Initial and continuing jobless claims are settling at high levels suggesting more modest job gains in August compared to previous months.

- The Federal Reserve is wrapping up its comprehensive monetary policy framework review. Chairman Powell will provide an update next week at the Jackson Hole Symposium.

Markets Optimistic Despite No Deal Yet from Washington

On the economic data front, housing activity continued to exceed expectations. Both housing starts and existing home sales trounced market forecasts in July, rising by 22.6% and 24.7% month-on-month, respectfully. Starts are now just 7% below their pre-pandemic peak (January), while existing home sales are 8% above January levels (Chart 1).

The housing market has been a bright spot for the U.S. economy during this pandemic. Record-low mortgage rates have had a magnetic pull on prospective buyers, especially millennial who have held-off purchasing a home due to affordability constraints (see report). This has given homebuilders the confidence to resume construction at extraordinary speed.

Looking ahead, the housing outlook depends on the labor market recovery. Prospective buyers will need the income to take the plunge into homeownership, but a wobbling labor market could delay their plans.

With the labor market hitting speed bumps, the onus is on policymakers to provide additional support to households and businesses that are struggling due to the pandemic. Congress has been deadlocked on the next set of fiscal measures, with the Democrats pushing for more income support and Republicans arguing for less. It is clear, however, that more aid will be needed to avoid deepening the economic crisis.

This sentiment was the key discussion point among Federal Open Market Committee (FOMC) members. As noted in the minutes from July, participants zeroed in on the importance of fiscal policy in holding up spending, investment, and the labor market until a vaccine or effective treatment is found. A significant downside risk to the economic outlook is if fiscal support disappoints. At the current juncture, this seems to be a very real possibility.

In terms of monetary policy, several FOMC participants agreed that without convincing fiscal support, more stimulus may be needed to promote the economic recovery. They debated the use of forward guidance and yield curve control, with the former getting more attention among members. Fed Chairman Jerome Powell will likely provide more insight into these issues as well the broader wrap up of the comprehensive monetary policy framework review next week at the Fed’s annual Jackson Hole Symposium.

Sri Thanabalasingam, Senior Economist | 416-413-3117

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.