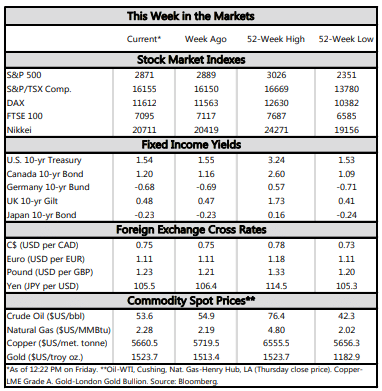

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

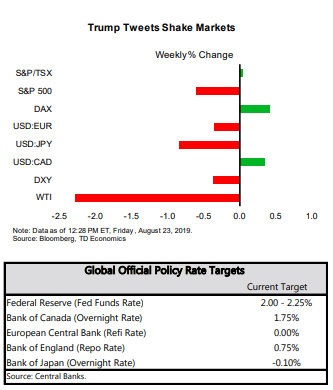

- This week may have been short on economic data, but the fireworks were lit on Friday as the President lashed out against China’s decision to impose tariffs on $75 billion of U.S. imports, sending stock markets into a tailspin.

- Risks increased, and global outlook has darkened since the Fed’s last meeting in July. Chair Powell acknowledged this at Jackson Hole, saying the Fed “will act as appropriate to sustain the expansion.” We anticipate two additional cuts will be needed this year to cushion the economy.

- The lone data release, existing home sales, was positive, with sales rising 2.5% in July and up 9.9% since January’s trough.

Markets on Edge as Recession Risks Rise

Earlier this week, the Fed’s minutes revealed that while the majority of the FOMC members supported the July rate cut as a “prudent step from a risk-management perspective,” there was a diversity of views among members. We already knew that two voting members dissented, but the minutes showed that those in favor of cuts citing different reasons for monetary easing ranging from low inflation to headwinds from trade tensions and insurance against slowing global growth.

Rather than abating, those risks have increased since July. Today, China responded to the U.S.’s latest tariff escalation by announcing 5%-10% on the remaining $75 billion of the U.S. imports. While the 10% tariff doesn’t seem like it would kick the chair out from under the global economy, as we argue in our recent report, this recent tit-for-tat escalation between China and the U.S. may be the last straw that damages business and market confidence beyond the point of no-return.

In concert, the global outlook has darkened since the Fed’s last meeting. Global growth is now tracking 2.9% – the slowest pace in a decade (Chart 1). Global manufacturing PMIs have remained weak, and geopolitical risks, such as the no-deal Brexit, have intensified. Consumer sentiment levels in Europe are also low, consistent with levels that have historically preceded a recession. All in all, there is little surprise bond markets continue to flash warning signs, with the spread between the 10-year and 2-year Treasuries briefly turning negative again this week.

In the one economic footnote to a week that is ending dramatically, the existing home sales data was positive. Sales rose 2.5% to 5.42 million in July and are now up 9.9% from their trough in January, evidence that the more than 100 basis point decline in mortgage rates is helping to revive demand (Chart 2).

Ksenia Bushmeneva, Economist | 416-308-7392

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.