HIGHLIGHTS OF THE WEEK

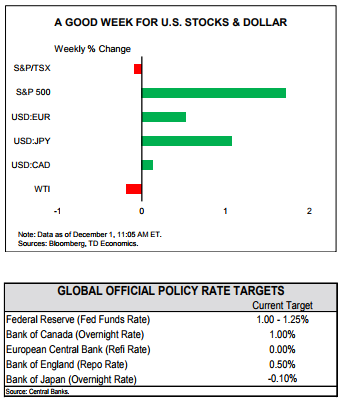

- The prospect of corporate tax cuts led both the Dow Jones Industrial Average and the S&P 500 to record highs this week, with financial stocks outperforming substantially.

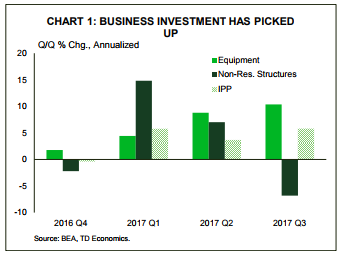

- Economic data was supportive, with third quarter real GDP being revised up to 3.3% annualized, as business investment came in stronger than initially thought.

- Incoming Fed Chairman Jerome Powell stated that “conditions are supportive” of a December rate hike, and we expect the Fed to proceed with one, followed by two more in 2018.

Tax Cuts Just Around The Corner

Economic data released this week also supported investor sentiment, with third quarter real GDP revised up to an impressive 3.3% as business investment accelerated (even more than previously estimated), with firms ramping up expenditures on equipment notably (Chart 1). This marks the strongest two consecutive quarters of growth for the American economy in three years. Momentum in business investment is expected to continue, with shale oil production likely to be a key contributor. Producers have ramped up activity this year in response to a rising price of WTI crude oil. OPEC’s commitment to extend supply cuts through 2018, announced this week, should maintain this momentum. As a result, the upside for the price of crude oil will be limited; we expect the price of WTI crude to sit in the US$50-55 range as the market balances out.

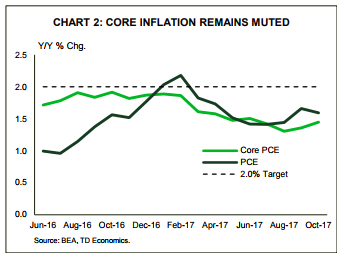

Incoming Fed Chairman Jerome Powell stated that “conditions are supportive” of a December rate hike at his confirmation hearing on Tuesday. Mirroring this view were Yellen and Kaplan in their speeches this week, in contrast to Kashkari who would like to see firmer evidence of inflationary pressures building before proceeding with a hike. At this point, markets are fully pricing in a December hike and we expect the Fed to proceed with one, followed by two more in 2018. Making this scenario increasingly likely is progress on the tax reform front which will require faster monetary policy normalization in order to temper the potential inflationary pressures

Katherine Judge, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.