Financial News Highlights

- A second reading on U.S. GDP showed that the economy expanded by an even more impressive 5.2% (annualized) last quarter, a 0.3 percentage point upgrade from the initial reading in financial news. Government spending and business investment were revised up, but consumer spending was revised down slightly.

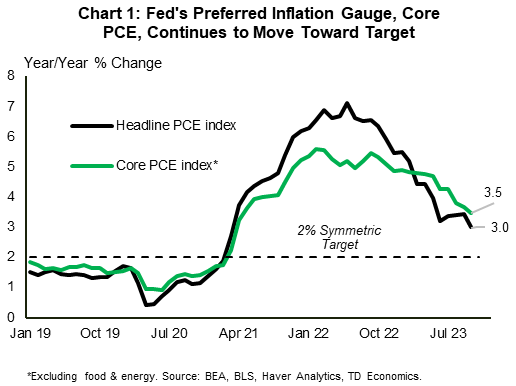

- October’s real consumer spending data showed that growth eased at the start of the fourth quarter. Core PCE inflation, the Fed’s preferred measure, also cooled to 3.5% year-on-year from 3.7% in September.

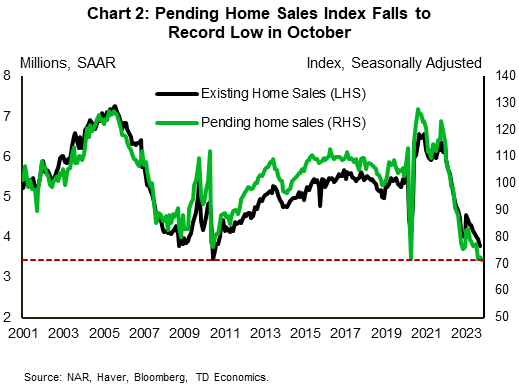

- The National Association of Realtors pending home sales index fell to a record low in October.

Moving Toward Target

The U.S. economy grew at an even better pace than initially reported in the third quarter. But, a moderation in consumer spending in October coupled with some progress on the inflation front, reinforced market expectations that the Fed has likely reached the end of its tightening cycle. That said, Fed speak out this week was somewhat mixed, with some suggesting that today’s policy rate is sufficiently restrictive while others still feel it’s too early to call it quits. In his speech on Friday, Chair Powell called talk of cutting rates ‘premature’.

The U.S. economy grew at an even better pace than initially reported in the third quarter. But, a moderation in consumer spending in October coupled with some progress on the inflation front, reinforced market expectations that the Fed has likely reached the end of its tightening cycle. That said, Fed speak out this week was somewhat mixed, with some suggesting that today’s policy rate is sufficiently restrictive while others still feel it’s too early to call it quits. In his speech on Friday, Chair Powell called talk of cutting rates ‘premature’.

The second reading on U.S. GDP showed that the economy grew by 5.2% (annualized) last quarter, an upgrade of 0.3 percentage points from the initial reading. The upward revision reflects improvements in government spending and fixed investment. One major category going against the grain was consumer spending, which was revised slightly lower to 3.6% from 4% previously. Stepping into the fourth quarter, the personal income and outlays report, added another layer of moderation for the consumer. Nominal spending rose 0.2% month-over-month (m/m) in October, a deceleration from 0.7% in September. The spending slowdown was less pronounced on an inflation-adjusted basis, with growth easing to 0.2% from 0.3% in the month prior.

Given a reduction in credit availability and the drawdown of pandemic era ‘excess savings’, the American consumer will have to rely more closely on income growth to fund its spending (see here). As such, any softness on the labor market should filter through to weaker spending. Peeking into the labor market, continuing jobless claims rose to 1.93 million in mid-November. This is the highest level since late 2021 and an added sign that the labor market is gradually cooling. Overall, we expect consumer spending to remain buoyant over the holiday period, but the momentum is likely to fade, with consumption growth likely to slow to around 2% this quarter.

Given a reduction in credit availability and the drawdown of pandemic era ‘excess savings’, the American consumer will have to rely more closely on income growth to fund its spending (see here). As such, any softness on the labor market should filter through to weaker spending. Peeking into the labor market, continuing jobless claims rose to 1.93 million in mid-November. This is the highest level since late 2021 and an added sign that the labor market is gradually cooling. Overall, we expect consumer spending to remain buoyant over the holiday period, but the momentum is likely to fade, with consumption growth likely to slow to around 2% this quarter.

The monthly personal income and outlays report also carried some good news on the inflation front. The highlight was a continued deceleration in core PCE – the Fed’s preferred inflation gauge – which slowed to 3.5% year-on-year in October from 3.7% in the month prior (Chart 1) in financial news. Interest rates have eased alongside this continued progress toward the Fed’s 2% target, and so have mortgage rates. The 30-year mortgage rate is currently hovering near 7.2% – some 80 basis points lower than the 8% peak in mid-October. This pullback appears to be providing some relief on housing, with mortgage purchase applications ticking higher for the fourth week in a row last week. But, the impact of interest rates tends to be felt with a lag, so this will take some time to be manifested in sales activity. To that end, pending home sales fell to an all-time low in October, indicating that things are likely to get worse before they get better (Chart 2).

All in all, higher interest rates are working as intended with inflation gradually easing toward target, but the Fed can’t let its guard down prematurely and is likely to maintain a hawkish tone until it is convinced that the inflation is decisively moving back towards 2%.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.