FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Bonds sold off for the fourth consecutive week, while equity markets are set to decline for the first time since the U.S. elections.

- Investors have likely engaged in some profit taking in advance of next week’s events which could trigger increased market volatility. Sunday will see Italians voting on constitutional amendments and Austria’s Presidential election. But, the main event is set for Thursday, with the ECB widely expected to announce a tapering plan.

- Domestic data this week remained supportive of the narrative of continued U.S. economic recovery in the second half of this year. This morning’s payrolls data was less rosy than expected, but is unlikely to dissuade the Fed from raising its policy interest rate when it meets in a couple weeks.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

BOND MARKET SELLOFF CONTINUES FOR FOURTH CONSECUTIVE WEEK

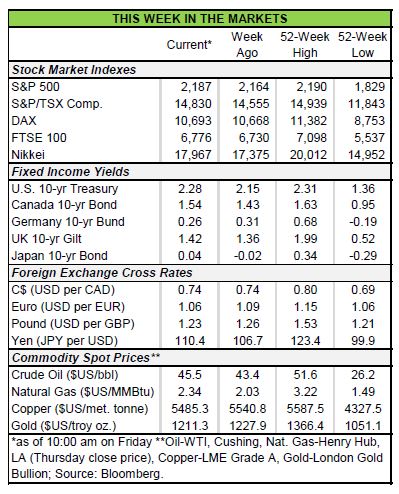

The sell-off in global bonds continued through this week, marking the fourth consecutive week of sizeable losses for bond investors. The U.S. 10-yr Treasury yield hit 2.44% earlier this morning – a level not seen since mid-2015. European bond markets also sold off, with yields rising to early-2016 levels. The stock market failed to benefit from the exodus from bonds this week however, with

After some post-election euphoria, and with much uncertainty still remaining, investors look to have taken some profits and are repositioning themselves ahead of some important international events next week which risk triggering another bout of market volatility. Things will kick-off on Sunday, when Italians vote on constitutional amendments that would remove much of the legislative authority of the Senate, credited with creating legislative gridlock often blamed for delaying necessary economic reforms. Whatever the outcome of the referendum – which could result in the resignation of the pro-EU Prime Minister Matteo Renzi should it be rejected – isn’t likely to have material implications on financial markets outside of Italy. On the same day, Austria will hold Presidential elections for the second time this year after election irregularities were found in the May round. Although there are concerns about the potential election victory of the candidate from the far right FPO party, the election outcome is unlikely to have much impact on financial markets, with much of the authority in the office of the Austrian Chancellor rather than the President. The main market moving event is scheduled to occur next Thursday when the ECB is expected to reveal a plan to taper the pace of bond purchases alongside their interest rate decision.

Together with higher inflation expectations due to firmer oil prices, the anticipated tapering as early as the second quarter of 2017 accounts for much of the bond selloff this week.

The selloff was further supported by strong domestic data, which continue to support the narrative of an economic recovery in the second half of 2016. This week, the second estimate of GDP growth was revised up to 3.2% (q/q annualized), up from the initial estimate of 2.9%. Moreover, although consumer spending in October was somewhat disappointing – partly owing to warmer weather – but strong income growth over the past several months should contribute to a bright holiday season.

All told, given the inflow of positive data for the second half of 2016, even a large miss in this morning’s payroll report would have likely failed to dissuade the FOMC from voting to raise its interest rate target in a couple weeks. Although non-farm payrolls increased by 178k in November, well above trend, although the underlying details were not overly optimistic. Private sector payrolls disappointed, while the participation rate ticked down to a six month low, and wage growth slowed. While not a cause for alarm, today’s report highlights that the Fed will seek to tighten at a gradual pace, especially given the significant tightening already embedded in the recent run-up in rates and the dollar.

Fotios Raptis, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.