Financial News Highlights

- The Federal Reserve cut its policy rate by 25 basis points to 4.25-4.5%, as expected in financial news. But, updated forecasts showed that FOMC members now expect inflation to be a bit hotter next year, and as a result expect to make only 50 basis points in cuts next year, down from 100 bps in September.

- Economic growth was revised upwards in the third quarter. Real GDP rose 3.1%, up from 2.8% previously.

- There was also good news on the Fed’s preferred inflation gauge. The Core PCE Deflator held steady at 2.8% in year-on-year terms in November, but cooled noticeably on a month-to-month basis.

Fed Signals a More Cautionary Stance on Rate Cuts Next Year

The Federal Reserve delivered some sour candy to cap off 2024, cutting its policy rate by 25 basis points, but signaling a more moderate pace of cuts next year. This hawkish tilt sent Treasury yields higher, with the 10-year rising from just under 4.4% to briefly over 4.6%. Equity markets took the news hard, with the S&P 500 down roughly 3.5% from pre-meeting levels at time of writing. Part of the weak equity market performance may also have to do with a looming government shutdown. Washington has only a few hours to pass a funding bill into law. Failure to do so will lead to a partial government shutdown. Essential services would continue, but most federal workers wouldn’t receive a paycheck. In addition, some workers would be furloughed until Congress passes new funding. The Bipartisan Policy Center estimates that some 875 thousand federal workers would be furloughed.

The Federal Reserve delivered some sour candy to cap off 2024, cutting its policy rate by 25 basis points, but signaling a more moderate pace of cuts next year. This hawkish tilt sent Treasury yields higher, with the 10-year rising from just under 4.4% to briefly over 4.6%. Equity markets took the news hard, with the S&P 500 down roughly 3.5% from pre-meeting levels at time of writing. Part of the weak equity market performance may also have to do with a looming government shutdown. Washington has only a few hours to pass a funding bill into law. Failure to do so will lead to a partial government shutdown. Essential services would continue, but most federal workers wouldn’t receive a paycheck. In addition, some workers would be furloughed until Congress passes new funding. The Bipartisan Policy Center estimates that some 875 thousand federal workers would be furloughed.

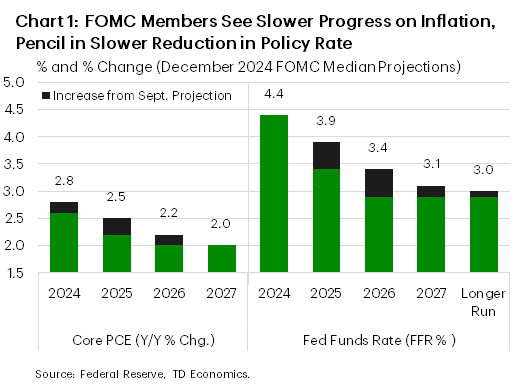

The Fed’s quarter point interest rate cut was as expected, but the accompanying Summary of Economic Projections (SEP) raised a few eyebrows. While the median forecasts for economic growth and the unemployment rate were little changed, the outlook for inflation and the policy rate were raised noticeably (Chart 1). Focusing on the year ahead, the median projection now has the Fed Funds Rate ending next year 50 basis points higher than expected in September. This is in tune with a firmer outlook for core inflation. Asked about the more cautious stance on rate cuts, Fed Chair Powell listed several reasons. These included the economy growing at a better pace and inflation coming in a bit hotter than expected recently. Powell also highlighted an elevated uncertainty around the inflation projections – a theme that was visible in the SEP document, with uncertainty and upside risks to core PCE inflation both up noticeably since September. Pressed on how much of the difference could be explained by the evolving data versus potential policy changes from the new Trump administration, the Fed Chair acknowledged that some policymakers did take preliminary steps to incorporate “highly conditional estimates of economic effects of policies into their forecast at this meeting”.

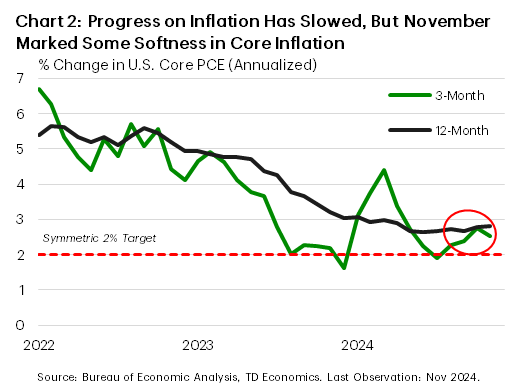

This week’s economic data buttressed several of Powell’s comments. The third estimate of Q3 GDP indicated that the economy grew at an improved pace of 3.1% annualized, up from 2.8% previously. At the same time, the November personal income and spending report indicated that consumer spending should end the year on solid footing. Consumer spending is on track for a solid 3% pace in the fourth quarter of 2024. That is only a small downshift from 3.5% pace in the third quarter. The November report also carried some better news on inflation, with the Fed’s preferred inflation gauge – core PCE – cooling noticeably in November, up a modest 0.1% month-over-month. While the annual pace remained at 2.8%, this latest cooldown helped reverse near-term trends lower (Chart 2).

This week’s economic data buttressed several of Powell’s comments. The third estimate of Q3 GDP indicated that the economy grew at an improved pace of 3.1% annualized, up from 2.8% previously. At the same time, the November personal income and spending report indicated that consumer spending should end the year on solid footing. Consumer spending is on track for a solid 3% pace in the fourth quarter of 2024. That is only a small downshift from 3.5% pace in the third quarter. The November report also carried some better news on inflation, with the Fed’s preferred inflation gauge – core PCE – cooling noticeably in November, up a modest 0.1% month-over-month. While the annual pace remained at 2.8%, this latest cooldown helped reverse near-term trends lower (Chart 2).

Overall, with the economy remaining on decent footing and inflation seemingly having resumed its downward path, there is room for further policy normalization next year. But, the potential for major policy changes from the new U.S. administration remains a wildcard.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.