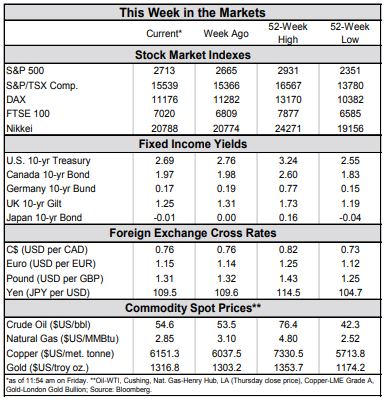

HIGHLIGHTS OF THE WEEK

- Financial markets extended their gains this week. The re-opening of the U.S. government, the dovish FOMC statement, progress in the U.S.-China trade talks and a strong January payroll report all helped to boost sentiment.

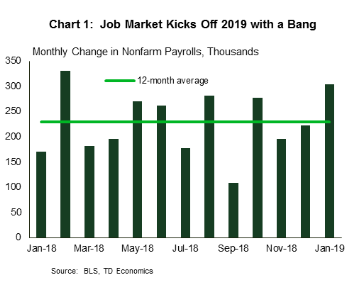

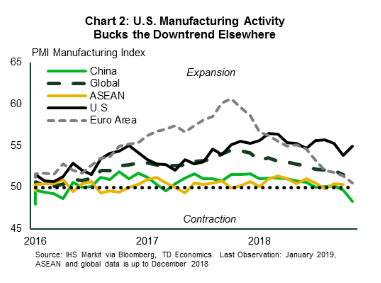

- Global growth concerns persisted this week, but the U.S. economy continued to move along nicely. The labor market added 304k new jobs in January, and the ISM manufacturing index improved after a sharp decline in December.

- Even as domestic economic performance remains solid, global growth slowdown did not go unnoticed by the FOMC. The Committee left the fed funds rate unchanged, and went to great lengths to emphasize patience.

The Fed’s Rate Hikes: A Pause or A Stop?

Concerns about slowing global growth continued to linger this week. Even so, financial markets had a lot to be cheerful about: the U.S. government re-opened, the FOMC was dovish, the U.S.-China talks made progress and January payroll report showed blockbuster job growth. After a brutal December, this week’s trading capped the best monthly performance for the S&P 500 since October 2015.

Top of the list, the longest shutdown in U.S. history has ended – for now. A short-term spending bill keeps the government funded until February 15th. Still, the damage has been done. Various estimates suggest that the shutdown has shaved between 0.2-0.4 percentage points off first quarter GDP growth, which is tracking 1.6% (annualized). While most of the lost economic activity will be recouped in the following quarter, some of the loss will be permanent.

Global growth slowdown considerations did not go unnoticed by the FOMC. As widely expected, the Committee left the target range for the fed funds rate unchanged at 2.25%-2.5%, but the statement itself was very dovish. In particular, the committee acknowledged that, while domestic economic activity has been “rising at a solid rate”, risks to the outlook have increased, which would necessitate patience and flexibility on the Fed’s behalf. Any mention of “gradual” rate increases has been removed, suggesting the Fed is prepared to be patient for some time until the fog clears and its gets a better reading on global and domestic economic conditions.

Ksenia Bushmeneva, Economist | 416-308-7392

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.