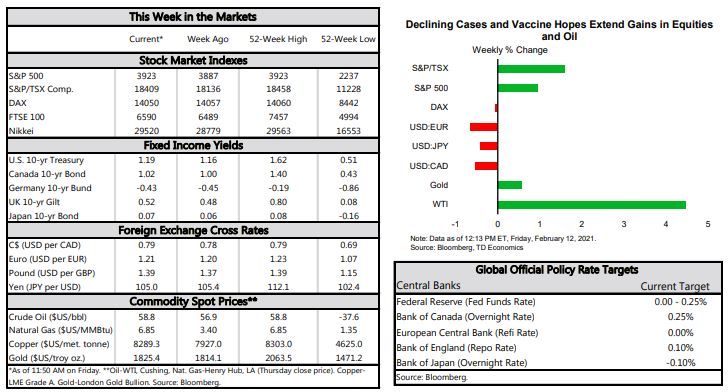

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

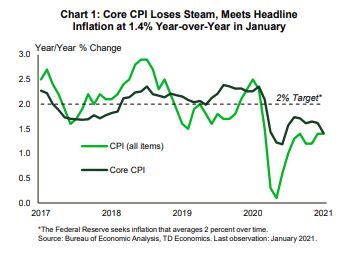

- The headline Consumer Price Index rose 0.3% in January and was up 1.4% year-on-year. Removing food and energy prices, the core index was flat on the month and slowed to 1.4% year-on-year from 1.6% in December.

- Small business optimism deteriorated for the third month in a row in January. Underneath the headline, the employment indicators remained broadly positive. Initial jobless claims also edged lower to 793k last week.

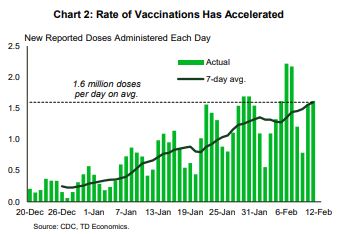

- Health metrics moved in the right direction this week. New COVID-19 cases continued to trend down, falling below 100k per day. Meanwhile, the vaccine rollout continued to pick up, averaging 1.6 million per day.

Moving In The Right Direction

Given the scope of fiscal and monetary policy supports to-date and the large fiscal package currently in the works, a lively debate is taking place in economic circles regarding the potential for inflation to accelerate beyond desirable levels. As we discuss in a recent report, a pickup in inflation is highly likely as economic restrictions are lifted. But, given where inflation stands today, there is some room for it to run before it reaches a concerning pace. Supporting the narrative of higher inflation is the fact that many small businesses plan to raise prices. According to NFIB data, the share of firms planning to do so rose by 6 points to 28% in January – among the highest levels in the post-Great Recession period.

Speaking of small businesses, the headline NFIB confidence measure ticked down modestly for the third consecutive month in January. Pullbacks in the expectations subcomponents were the biggest drags on the headline measure. But, in what can be viewed as a sign of underlying resilience, the employment metrics remained broadly positive. Hiring plans held steady in January, while job openings and the share of firms raising and planning to raise worker compensation ticked up.

While the U.S. labor market struggles to dig itself out of the winter slowdown, there appears to be a light at the end of the tunnel. New COVID-19 cases continued to trend down this week, falling below 100k per day recently for the first time this year. At the same time, the pace of vaccinations is accelerating, with daily jabs averaging 1.6 million in recent days (Chart 2). The vaccine rollout should continue to gather speed (see report released today), hastening the end of the pandemic.

With health metrics continuing to move in the right direction, a loosening of restrictions and stronger consumer confidence should follow. Coupled with another likely jolt of fiscal stimulus, this bodes for the U.S. economy to expand at a solid clip this year. If the full $1.9 trillion American Rescue Plan package is passed, real GDP growth could run as high as 6% through 2021, enough to bring the level of GDP back to its pre-crisis trend by the end of the year. New COVID-19 variants are the main downside risk to this positive outlook. For now, their spread remains low, but it is increasing in several key states. This is something that we’ll be keeping a close eye on.

Admir Kolaj, Economist | 416-380-1195

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.