FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Last A holiday-shortened trading week light in economic data left markets to focus on communications from the Federal

Reserve. - U.S. existing home sales slumped in January, beleaguered by low inventories and deteriorating affordability.

- The FOMC minutes revealed a Fed busy revising up economic projections, suggesting that further gradual policy firming

is warranted.

More Rate Hikes Incoming

Existing home sales for January revealed a market that is still beleaguered by low inventory, which exacerbates deteriorating housing affordability in many U.S. cities. January’s decline in existing home sales was broad-based, and concentrated in the larger single-family segment (Chart 1). Unsurprisingly, rising prices and borrowing costs are deterring first-time buyers from buying, as they accounted for only 29% of sales in January, down from 33% a year ago. Looking ahead, job gains and an optimistic outlook for after-tax earnings growth should support a rebound in home sales. What’s more, housing starts ticked up in January, possibly providing some respite for buyers particularly in those markets with a low supply of existing homes.

The firmer U.S. growth outlook has raised questions about how tolerant a Powell-led Fed would be of above-target inflation. Perhaps one of the most surprising admissions this week was from FRB Philadelphia President Harker, who is not a voting member of the FOMC but a contributor to the quarterly economic projections. He mentioned in a speech on Wednesday that he was comfortable penciling in just two rate hikes for this year, but may adjust if the evolution of the data requires it. This is somewhat counter to what most economic models would suggest, and even an often pessimistic market has moved to price-in about three rate hikes for 2018. Some economic forecasters have penciled in four rate hikes for 2018 after fiscal stimulus was announced.

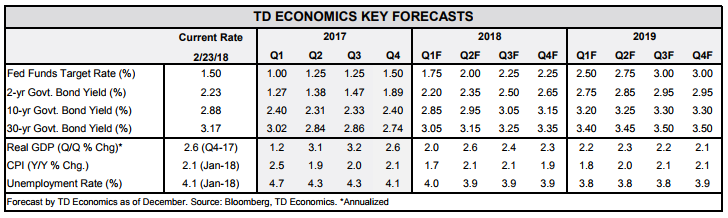

Nonetheless, the FOMC minutes from its January meeting revealed a Fed busy revising up economic projections for the U.S. economy, and therefore confident that further gradual policy firming is warranted. While there is a lot of room for interpretation on what “further” implies, it’s safe to conclude that rates will rise this year. To be clear, we have stuck with our view from this past December that the economic outlook and balance of risks are consistent with three rate hikes by the Fed this year. However, the additional stimulus from the recently announced fiscal program pushes up our rate hikes for 2019 to three from two. This places the fed funds rate at 3.0% at the end of 2019, and about 20 basis points above the FOMC’s longer-run expectation.

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.