FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Federal Reserve Chairman Powell reassured markets that there will be no early tightening of monetary policy or drawdown of asset purchases even with a brighter economic outlook.

- Consumers remain at the forefront of the recovery, as personal income surges and spending rebounds on the back of income support measures.

- Jobless claims fell more than expected this week but remain three times higher than pre-pandemic levels.

The American Consumer is Back

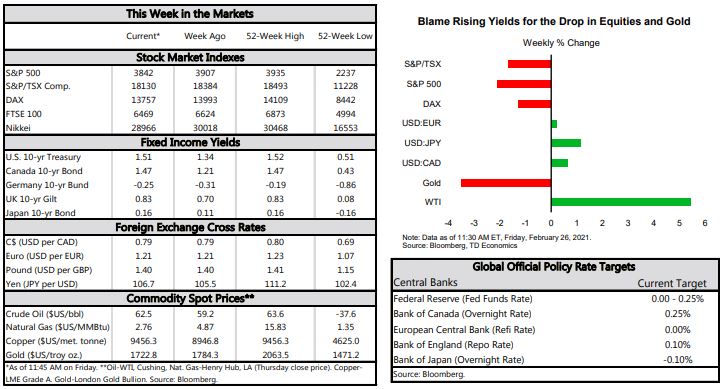

For a change, the S&P 500 did not have the best week. As of writing, it was down 2.4% compared to last week’s close. Blame the Treasury yield. The 10-year Treasury yield hit the highest point in a year amid a more upbeat global economic outlook and rising concerns over inflation. The decline in equities was primarily led by large cap technology stocks, which have so far made major gains during the crisis. Still, the S&P 500 is 3% higher than where it was at the start of this year.

On the monetary policy front, the Federal Reserve’s Chairman Powell probably had the most optimistic assessment of the economy since the start of the pandemic. He told Congress that there was “hope for a return to more normal conditions”. Still, Powell signaled he is in no rush to tighten monetary policy or drawdown asset purchases even with a brighter economic outlook. The Chairman also reassured markets on the inflation front. He said that inflation dynamics do “not change on a dime” and that “the economy is a long way from our employment and inflation goals”.

In terms of economic data, personal income surged by 10% month-on-month in January, in line with market expectations. The strength was primarily due to the 52.6% increase in social benefits which include stimulus checks and expanded unemployment insurance benefits. Meanwhile, personal spending rose by 2.4% and was led primarily by goods which went up 5.8% (Chart 1). The rise in goods spending was seen across the board, with recreational goods and vehicles driving most of the gains. The services sector also showed resilience, eking out a 0.7% growth in spending. Gains were mostly led by food services and accommodation, the industry which has been in the line of fire right from the outset of this pandemic.

Turning to the labor market, jobless claims fell far more than expected (Chart 2). Initial claims came in at 730k, down 111k from the prior week, and beating the consensus of 825k. This was the largest weekly drop since the end of August. But not all states performed the same. California and Ohio registered the biggest declines while Illinois and Missouri recorded notable growth. Continuing claims came in at 4.4 million, 41k less than the consensus and down 0.1 million from the week before. Still, both claims are almost three times higher than their pre-pandemic levels. The labor market remains the weak link in an otherwise stronger-than-expected start to the new year for the economy.

Meanwhile, revisions to the second GDP release were relatively minor. The economy grew 4.1% annualized in the final quarter of last year, slightly higher than the initial estimate of 4.0%. Government and household spending were both revised down 0.1 ppts. Meanwhile, non-residential fixed investment was adjusted up 0.2 ppts, driven by stronger spending on equipment and intellectual property products. Residential investment was also revised higher by 0.1 ppts. Given the relatively minor adjustments to the quarterly data, there were no changes to the annual GDP, which shrank 3.5%.

Sohaib Shahid, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.