Financial News Highlights

- The Federal Reserve hiked the fed funds rate 25 basis-points, a step down from six consecutive hikes of 50 or 75 bps.

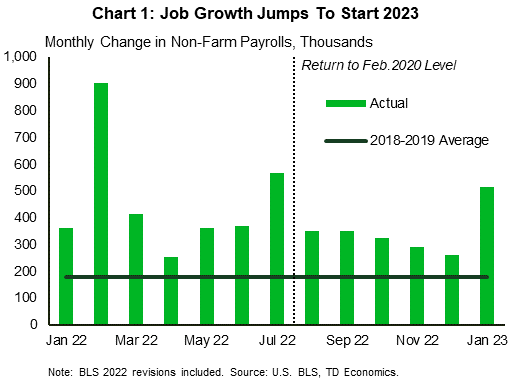

- Non-farm payrolls accelerated in January for the first time in five months, adding 517k jobs and nearly tripling market expectations.

- The ISM Manufacturing Index dropped to its lowest level since May 2020, with new orders declining at an accelerating rate, while the ISM Services Index returned to strong growth after contracting in December.

Until the Job Is Done

With the first month of 2023 in the books, the start of February was marked by the much anticipated (but widely expected) rate decision delivered by the Federal Reserve on Wednesday in major financial news. Coupled with a sizeable upside surprise in the January employment data on Friday, markets certainly had a lot to think about this week. The S&P 500 rose 2.6% for the week, while the ten-year Treasury yield was little changed at 3.5% as of the time of writing.

With the first month of 2023 in the books, the start of February was marked by the much anticipated (but widely expected) rate decision delivered by the Federal Reserve on Wednesday in major financial news. Coupled with a sizeable upside surprise in the January employment data on Friday, markets certainly had a lot to think about this week. The S&P 500 rose 2.6% for the week, while the ten-year Treasury yield was little changed at 3.5% as of the time of writing.

Labor markets began 2023 with a bang, breaking a five-month deceleration trend and adding 517k jobs (Chart 1). This brought the unemployment rate down by 0.1 percentage points (ppts) to a 53-year low of 3.4%. In addition, revisions to 2022 data added 311k jobs to last year’s tally. The labor force participation rate in January ticked up by 0.1 ppts to 62.4%. Average hourly earnings rose by 0.3% month-on-month (m/m) and hours worked increased by 0.9% m/m. On aggregate, this was an exceptionally strong jobs report, which when combined with the sustained downward trend in initial jobless claims and the increase in December job openings, will give the Federal Reserve plenty to contemplate over the coming weeks.

In contrast to the strong labor market data, the ISM Manufacturing Purchasing Managers’ Index (PMI) slipped further into contractionary territory in January, dropping 1 percentage point to 47.4 – its lowest level since May 2020. Economic activity in the sector contracted for the third consecutive month, as new orders continued to decline at an accelerating rate. This contrasts with the ISM Services PMI which showed the industry return to strong growth in January after briefly contracting in December, with new orders jumping up by 15.2 percentage points. While there have been positive developments in the manufacturing sector, such as reduced delivery times and lower price pressures, the robustness of the strength in the services sector will be a concern for the Federal Reserve as it seeks to put a lid on services price growth.

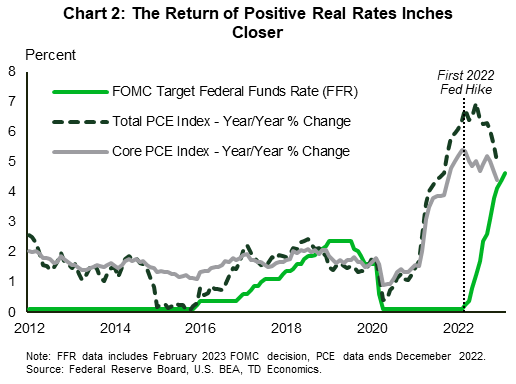

February began with a partial return to conventional monetary policy in the U.S., with the Federal Reserve raising rates by a more usual 25bps for the first time since last March (Chart 2). FOMC Chair Powell noted that it was gratifying to see progress on disinflation, but that further policy tightening would be required to ensure price growth sustainably returns to the Fed’s 2% target in financial news. During the press conference, Powell also pushed back against the idea of assuming the Fed could mitigate the risk of a binding debt limit in June, stating that the only way forward was for Congress to raise the debt ceiling.

February began with a partial return to conventional monetary policy in the U.S., with the Federal Reserve raising rates by a more usual 25bps for the first time since last March (Chart 2). FOMC Chair Powell noted that it was gratifying to see progress on disinflation, but that further policy tightening would be required to ensure price growth sustainably returns to the Fed’s 2% target in financial news. During the press conference, Powell also pushed back against the idea of assuming the Fed could mitigate the risk of a binding debt limit in June, stating that the only way forward was for Congress to raise the debt ceiling.

Markets expect another 25bps hike at the Fed’s next meeting in six weeks, at which time we will also receive an update on the Committee’s Summary of Economic Projections. The January employment report introduced fresh uncertainty to market expectations for the terminal rate, with May meeting expectations now evenly split between no change and a 25bps hike. Powell is in the hot seat in a Q&A next Tuesday, where he is likely to be pressed on his reading of the January jobs blowout. He is likely to confirm the hawkish bias of the press conference, and markets will be listening carefully for any hints of how high the Fed expects to raise rates now.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.