FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Economic data released this week was balanced enough to re-ignite optimism in financial markets without calling into question the next fiscal support package.

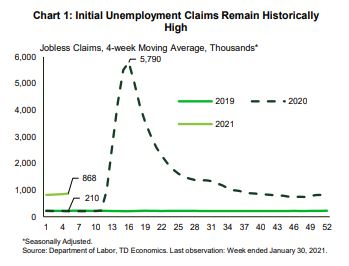

- Job market data showed a third consecutive decline in the weekly jobless claims as well as moderate progress in payrolls and an unexpected drop in the unemployment rate.

- Assuming continued progress on the health front, another round of substantial fiscal supports could push the American economy from stall speed to an outright sprint in the second half of this year.

A Cautiously Optimistic Week

At present, the job market shows tepid signs of improvement. On Thursday, the Department of Labor reported a third consecutive decline in the weekly number of Americans seeking unemployment benefits. Recent reports come with the caveat of considerable revisions due to difficulties in adjusting the historically-high level for seasonal factors. Even when smoothed over four weeks, claims remain around 650 thousand higher than a year ago (Chart 1).

Likewise, today’s employment report for January showed moderate progress, with payrolls rising by 49 thousand, while the unemployment rate unexpectedly fell to 6.3% from 6.7% in December. Despite this progress, the economy has thus far recovered just over half of jobs lost during the initial lockdown period. The pandemic continues to inflict disproportional pain on the services sector, deepening inequality (see report). One particularly dire spot remains the leisure & hospitality sector, which reported another month of losses in January. With the setback, employment in the sector is now 22.9% below its pre-pandemic level (Chart 2).

On the financial front, economic data was balanced enough to re-ignite optimism in financial markets without calling into question the next fiscal support package. The S&P 500 index ended the week 4.7% higher than the previous week and the 10-year U.S. Treasury rose to 1.15% from 1.08%.

This week, a report by the Congressional Budget Office estimated that the recently passed $900 billion stimulus package (signed into law at the end of December) would raise the level of GDP by 1.5% in 2021 and 2022, with most of that boost occurring this year. At $1.9 trillion, the next proposed round of fiscal support is even bigger. The income supports in the package will go a long way to bridging the gap to the other side of the health crisis and, with additional funding for vaccine distribution and testing, hopefully speed it along. Assuming continued progress on the health front, there is a good chance that the economy moves from stall speed to an outright sprint in the second half of this year (see report).

Maria Solovieva, CFA, Economist | 416-380-1195

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.