Financial News Highlights

- Tariffs on Canada and Mexico have been put on hold for one month, but a 10% tariff was imposed on imports from China in financial news.

- Companies have ramped up inventories ahead of tariffs, leading to a sharp increase in the trade deficit in December. Activity has eased off in the services sector, but continued to reaccelerate in manufacturing.

- Hiring has slowed in January, however, the labor market remains solid overall. Significant upward revisions to the fourth quarter figures suggest that job growth was stronger at the end of last year than previously thought.

Canada-Mexico Tariffs on Hold

This week was anything but boring for financial news. On Monday, an 11th-hour deal was reached to delay tariffs on Canada and Mexico for a month. However, while Canada and Mexico were spared, China was not, as an additional 10% tariff was imposed on all imports from the country.

This week was anything but boring for financial news. On Monday, an 11th-hour deal was reached to delay tariffs on Canada and Mexico for a month. However, while Canada and Mexico were spared, China was not, as an additional 10% tariff was imposed on all imports from the country.

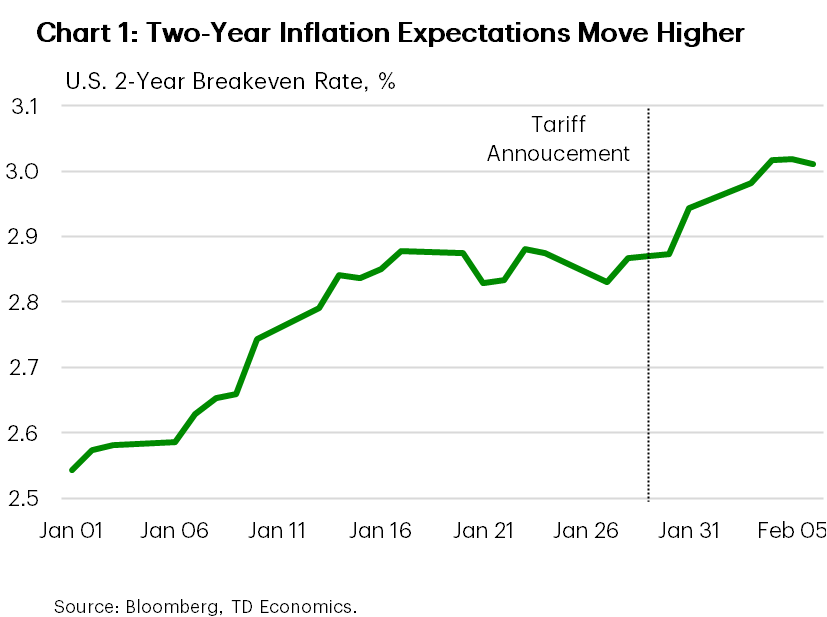

The prospect of tariffs being imposed on North America in a month, or in April when the review of current trade policies is completed, looms large. Financial markets have largely recovered from their initial knee-jerk reaction to the tariff announcement, with the S&P 500 paring back losses by the end of the week. However, inflation expectations over the next two years have risen (Chart 1) while bond yields have declined. This points to investors’ concerns that tariffs will accelerate inflation and slow economic growth.

Businesses’ uncertainty about the looming tariffs were reflected in the trade data. The U.S. trade deficit widened sharply in December – the largest one-month increase since the early 1990s. Imports surged as companies rushed to ramp up inventories ahead of potential tariffs. Last month’s sharp increase in the trade deficit is likely temporary, but trade policy uncertainty will continue to affect trade flows throughout the year. Uncertainty about tariffs also clouds the outlook in the manufacturing sector, particularly in industries such as auto manufacturing (report). Even though the ISM manufacturing index has continued to improve in January, rising for the third consecutive month and finally moving into expansionary territory, supply chain disruptions could dent the sector’s nascent progress.

Activity in the services sector continued to expand robustly in January, although it dialed back a notch. The services sector is less exposed to trade than manufacturing, but it is not immune. The prices paid subcomponent remains elevated, and any supply chain disruptions and higher input prices could reignite inflationary pressure.

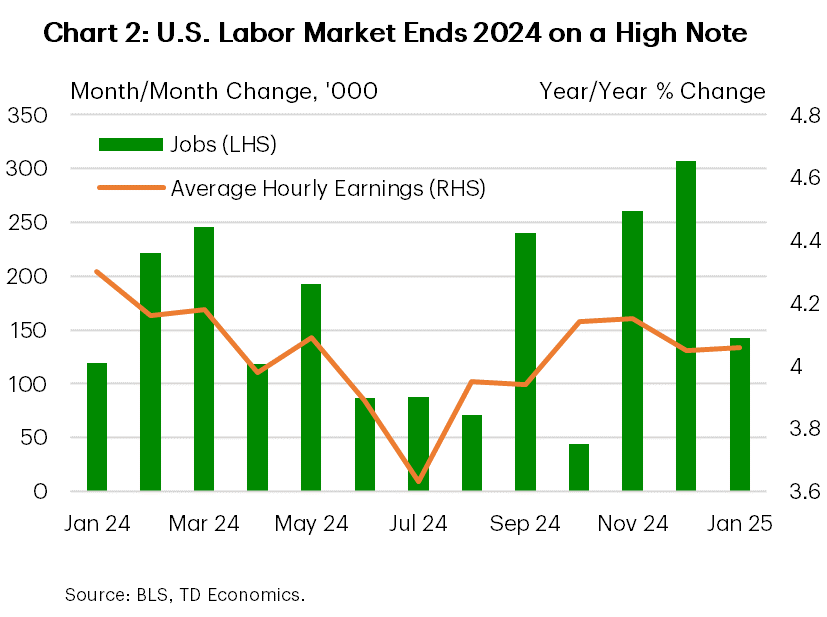

Additional inflationary impetus could also come from the labor market. Today’s employment report showed that the U.S. economy added 143k jobs in January. This is considerably less than December’s tally (+305k), but still a solid outturn, particularly when combined with a slight decline in the unemployment rate and an uptick in wage growth. Moreover, wildfires in Los Angeles and a cold weather spell nationwide could have also weighed on employment, suggesting a bounce-back next month could be in the cards. Lastly, revisions through the fourth quarter were notably higher, adding an extra 101k jobs to the previously reported figures and suggesting that hiring momentum was even stronger at the end of last year than previously thought (Chart 2).

Additional inflationary impetus could also come from the labor market. Today’s employment report showed that the U.S. economy added 143k jobs in January. This is considerably less than December’s tally (+305k), but still a solid outturn, particularly when combined with a slight decline in the unemployment rate and an uptick in wage growth. Moreover, wildfires in Los Angeles and a cold weather spell nationwide could have also weighed on employment, suggesting a bounce-back next month could be in the cards. Lastly, revisions through the fourth quarter were notably higher, adding an extra 101k jobs to the previously reported figures and suggesting that hiring momentum was even stronger at the end of last year than previously thought (Chart 2).

With inflation progress having stalled in recent months, wage growth showing staying power and heightened uncertainties on how far the new administration will go on its policies, the Fed is likely to remain more cautious. Next week’s inflation report will likely show that the Fed’s patience is justified, as inflation remains persistently above the Fed’s 2% target.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.