FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The U.S. economy kicked off the New Year with an unprecedented surge in COVID-19 cases. While a return to lockdowns is not expected, rising cases could lead to greater absenteeism, as workers self-isolate due to exposure, putting pressure on already-tight labor supply.

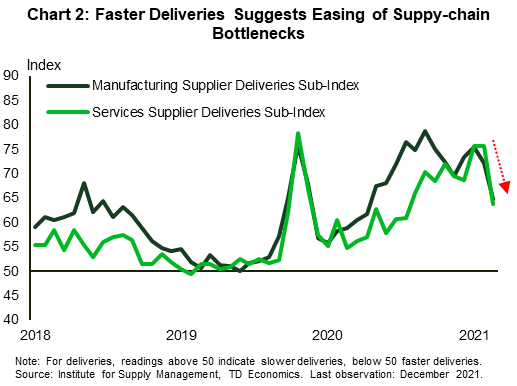

- On the upside, several metrics suggests that the supply chain bottlenecks are beginning to ease. Specifically, supplier deliveries in both the manufacturing and services sector were faster in December than they have been in recent months.

- On the labor front, employment came in softer than expected with 199k jobs added in December. The unemployment rate however continued to trek lower, hitting 3.9% (from 4.2%) while the labor force participation rate held steady at 61.9%.

U.S. – Supply Chain Strains Show Signs of Easing

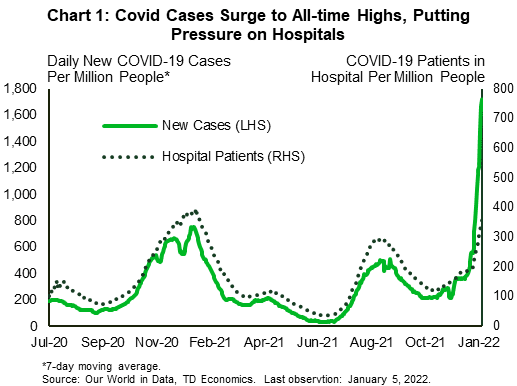

The economic calendar was jammed packed to start the new year in financial news. First up, a rapid increase in COVID-19 cases is quickly dwarfing all previous waves (Chart 1). Fortunately, hospitalization rates are not rising as swiftly, but are still ticking up at the same time that healthcare capacity is constrained by staffing shortages. The surge in cases has prompted airlines to cancel flights and companies to cut services and reduce hours as infected workers self-isolate (though for fewer days than past waves). With worker shortages already a pressing issue, the current wave is likely to weigh on near-term business performance and slow the recovery in high-contact services.

Adding to business challenges, workers are quitting their jobs at record rates, while job openings remain near all-time highs. Employers continue to add jobs, but job growth in December came in notably shy of the 450k anticipated by the market, at 199k. The disappointment was softened somewhat by a net 141k upward revision to the two previous months. The unemployment rate also fell from 4.1% to 3.9%, narrowing in on its pre-pandemic level of 3.5%. With high demand for workers and increasingly limited supply, it is little surprise that wage growth remains hot. Average hourly wages were up 4.7% from year ago levels in December, slowing slightly from 5.1% in November.

Such strength in the labor market, combined with more persistent inflationary pressures has added urgency to the Federal Reserve’s task of curtailing pandemic-induced support measures. Minutes from the most recent FOMC meeting showed that more members are inclined to accelerate the pace of policy normalization. This culminated in the Fed’s decision to speed up the taper of their Quantitative Easing program and possibly faster rate increases.

On the production side, there was some good news on easing supply constraints. The ISM manufacturing index slipped to 58.7 in December from 61.1 in November. Despite the slip, manufacturing activity is still expanding at a healthy clip. More encouragingly, there were hints that supply-chain problems could be easing as the supplier delivery sub-index fell to 64.9 in December from 72.2 the previous month (Chart 2). The decline suggests that delivery times are improving, which is a relief given the severe bottlenecks that manufacturers have been facing.

There was also a pullback in the ISM services index to 62 from 69.1 in November. The outturn however was not unexpected, given that the previous reading hit a record. The service sector also saw improvement in supplier delivery times as the index fell by 11.8 percentage points to 63.9 – the lowest reading in the past eight months.

Further good financial news saw vehicle production levels in December improve from their September lows – inching back closer to the 1.1M recorded in November. While still well below the pre-pandemic level, the improvement points to further easing in supply constraints in this key economic sector. Unfortunately, all of this data is for a time before the latest pandemic wave, and we could very well see a reversal in the months ahead. Still, with evidence this wave is progressing even faster than past waves, its peak should also not be too far in the future, allowing with any luck for the continued return to economic normalcy.

Shernette Mcleod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.