FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Financial markets this week were captivated by policy-related tweets and a mid-week press conference by President-elect Donald Trump that, while entertaining, proved to be short on policy detail.

- Retail trade data this week was broadly in line with market expectations, although the monthly advance was driven by increased purchases of autos and gasoline. Overall, the data remains consistent with our view that consumer spending will continue to support economic activity in 2017.

- Promises from policymakers are nothing new, and are an important driver of consumer and business expectations. However, the post-election euphoria may be premature. We remain hopeful that more policy certainty will materialize after the inauguration next week.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

RISING OPTIMISM BUT FEW DETAILS

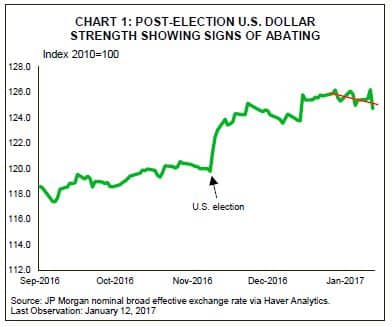

Financial markets this week had a fair bit of information to digest, mainly in the form of verbal communication from policymakers. Despite what was deemed a disappointing press conference by President-elect Trump this week given the lack of policy detail, equity markets are expected to end up on the week, while Treasuries round-tripped and should end the week roughly unchanged. The main story in financial markets this week was the volatility in the U.S. dollar index, which could mark the third consecutive week of declines.

The key economic data print this week was the December retail sales figure that showed a rise in consumer spending driven largely by autos and gasoline. While broadly in line with expectations, sales ex-autos and gasoline were virtually unchanged from the previous month. Overall, the data is consistent with our narrative that tightening labor markets and past gains in real income growth should support consumer spending in 2017.

Other data failed to garner as much attention this week. November data from the job openings and labor turnover survey didn’t affect the narrative of a recovering labor market. Somewhat more interesting was price data from surveys of producers and international trade, which showed a pick-up in price growth over the last twelve months, driven in large part by higher energy prices.

Given the lack of significant surprise in domestic economic data, markets focused their attention on what was being said by policymakers about the U.S. economy, particular concerning the outlook for monetary and fiscal policy. While market participants have long appreciated the power of central bankers to move financial markets with a few choice words, the dramatic market moves in reaction to recent policy proposals by elected officials has been noteworthy. Recent examples include the market’s swift reaction to tweets by President-elect Trump, and the market

volatility observed during his press conference this week.

The general optimism in the nation’s equity markets to the election result have been echoed in surveys of business and consumer confidence. This week, the NFIB optimism index surged, ending 2016 with the largest quarterly increase since 1980. The University of Michigan’s monthly survey of consumer sentiment, while pulling back ever so slightly in January, remained similarly upbeat, well above its pre-election level and at a rate that historically would suggest

some upside to the outlook for consumer spending.

While stories have always mattered, and economists have long emphasized the importance of expectations about the future, there is a risk is that at least some of this elation is premature. With limited details on the scope of policy changes or their economic effectiveness, there is a chance that the fiscal policy of the new administration will fail to achieve the economic outcomes promised. In the short-term the rise in confidence (or animal spirits) is a positive for the outlook, but any disappointment could lead expectations to pull back.

Hopefully some of this policy uncertainty will begin to fade after president-elect Trump is confirmed as President at next Friday’s inauguration. Still, if the events of the past week are any guide, expect financial market volatility to persist.

Fotios Raptis, Senior Economic

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.