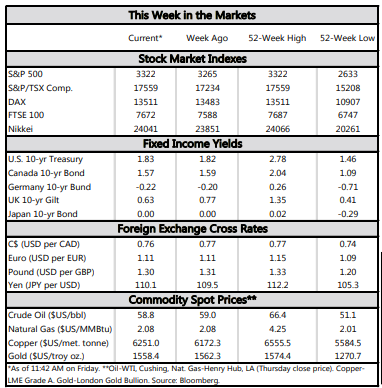

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Data releases over the week reinforce the main themes in the U.S. economy: solid consumption, housing market recovery, faltering business investment and soft inflation.

- The phase one trade deal was formally signed, committing China to increase its imports of U.S. goods and services to $200 billion more than the 2017 level. Reaching this target will be a difficult task

- While the agreement gives short-term relief, this is only the first phase. The likely difficulty in implementing the current accord combined with the more-difficult issues still to be discussed, mean that trade uncertainty is likely to continue to be a factor in the outlook.

Phase One Complete, But Can It Hold?

From a data perspective, 2019 ended with more of the same for the U.S. economy. Consumption likely remained solid in the fourth quarter, as evidenced by the healthy rise in retail sales in December. Retail sales advanced by 0.3% month-on-month, and November’s figure was also revised higher. There were gains in nearly every category, underlining the robust nature of the increase.

The housing market also continued its good run, with housing starts surging last month. Construction in both singles and multifamily units picked up in December, sending the overall level to its highest point in 13 years (Chart 1). Taking together, housing data for the fourth quarter implies that residential investment is on track to continue its upward climb heading into 2020.

On the flipside, we saw the NFIB’s small business optimism index move in the other direction in December. The decline is likely attributable to heightened policy uncertainty, a theme that has plagued businesses, big and small, throughout 2019 (see report).

Despite the increasing pressure on economic capacity, inflation remains stubbornly soft. December’s core consumer price index, which strips out the impact of energy and food prices, remained at 2.3% year-over-year, unchanged since October. On an annual basis, core CPI inflation was only a tick higher in 2019 at 2.2%. Looking ahead, price pressures may continue to be subdued especially with the U.S.-China phase one trade deal effectively cutting the existing tariff rate, while also removing the threat of additional tariffs at least for the time being.

This takes us to the big headline for the week, the U.S.-China phase one trade deal. On the face of it, the agreement could be a positive for U.S. growth as it commits China to purchasing an additional $200 billion worth of U.S. goods and services over the next two years (see commentary). But the big question is: can China adequately ramp up its imports to reach this target? The answer is probably not. Quarterly import growth would have to average above 10% for every quarter from now until the fourth quarter of 2021 to reach this goal (Chart 2).

The agreement also included a dispute mechanism. In the event China doesn’t meet its import commitments, the U.S. can resort back to imposing tariffs and if China responds, the deal would be nullified. Indeed, the agreement gives short-term relief, but its sustainability is still an open question.

Sri Thanabalasingam, Economist | 416-413-3117

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.