FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The government shutdown extended to its 28th day, making it the longest on record with no clear end in sight.

- The White House upped its estimate of the impact of the government shutdown to a 0.5ppt drag on 19Q1 growth after

four weeks.This is much higher than private sector estimates of between -0.1 to -0.2 ppts. - As expected, the Brexit withdrawal agreement was soundly rejected by UK parliament. With the March 29th deadline

fast approaching, it looks increasingly likely that the UK will have no choice but to seek an extension from the EU.

Dysfunctional Governments on Parade

The shutdown is exacting a toll on those least responsible for it. Anecdotes continue to highlight the hardships that furloughed federal employees are experiencing. These include workers turning to payday loan companies and food banks, while also taking on side hustles, such as driving for Uber, in order to make ends meet. Although federal employees will eventually be paid for lost wages, the near-term pain is clearly taking a toll.

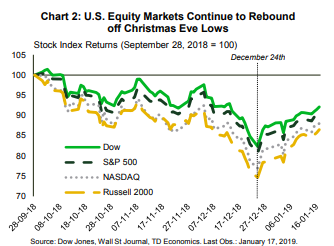

Despite the government dysfunction on display on both sides of the Atlantic, financial markets were largely unfazed. U.S. equity indexes have soared since the New Year, and are now back at levels seen in early December (Chart 2). There’s good reason for optimism. Data still being reported, such as weekly initial jobless claims, continued to signal a healthy economy. Trade talks with China are ongoing, with the next round set to take place on January 30th in Washington. Although little progress has been announced so far, news that U.S. officials were discussing ratcheting back some of the tariffs on Chinese imports in order to encourage an agreement helped to stoke a global rally in risk assets. Perhaps more importantly, Federal Reserve Presidents were out delivering speeches that reinforced the Fed’s willingness to be patient before the next rate hike. Indeed, patience is warranted given uncertainty about the economic impact of the government shutdown, and ongoing concerns about the health of the global economy.

Fotios Raptis, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.