FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

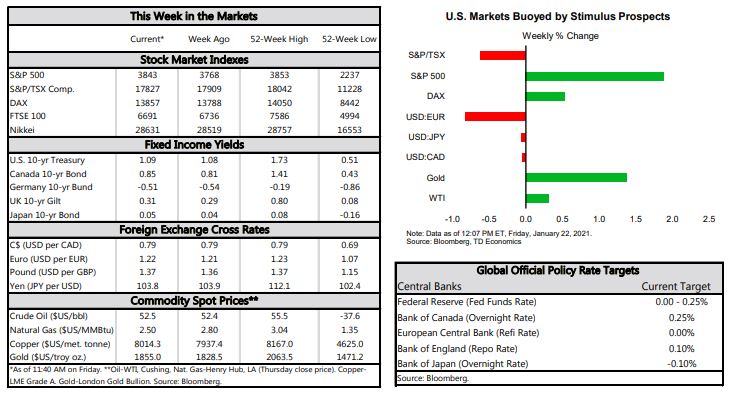

- President Biden’s inauguration was the marque event this week. Previous market optimism on the stimulus potential of the new administration seemed to run out of steam at week’s end.

- The current administration has ambitious plans for further Covid-19 relief, but it remains uncertain what Congress will agree to. In our recent report, we outline some potential scenarios for upside risks to economic growth.

- The housing market hasn’t run out of steam, with starts activity rising to new heights. It will be clearer in the coming months if the pandemic’s race for space and low mortgage rates have kicked off the next leg up in the housing market.

Biden’s Stimulus Would Boost Growth

President Biden’s inauguration was the marque event this week. Since the Georgia Senate run-off elections gave the Democrats a razor thin majority in Congress, equity markets have cheered the changeover in power. However, towards week end, sentiment soured a bit, perhaps as investors question how far the rally has gone.

Equity markets had been pricing in greater optimism on the American economy, hopeful that Democratic control in Congress would mean more fiscal stimulus and a faster recovery. However, it is still too early to determine what size of package will get through Congress. In a recent report we looked at three different scenarios for the next round of Covid-19 relief ranging from $500 billion to $1.9 trillion, and estimate the potential growth responses of each. The range of forecasts is shown in Chart 1.

These scenarios do not include a larger plan that the administration could pursue later in the year encompassing spending on campaign commitments such as infrastructure, and health and education, funded by higher taxes. These could have further implications on medium-term growth, particularly infrastructure spending, which has been shown to have some of the highest growth multipliers, particularly when the economy is weak.

The area of the economy that has rebounded most strongly from the pandemic-driven weakness in the spring is the housing market. Housing starts beat expectations in December, rising 5.8% to 1.67 million units (annualized), the highest level in 14 years. Once again, single family starts led the way, as demand for space has intensified since the pandemic, and inventory in the resale market remains drum-tight.

It is uncertain how long the current pace of construction can be sustained. In the 12 months prior to the pandemic, housing starts averaged 1.36 million. In the March through June period they ran well below that level, creating a backlog of pent-up demand. Since then, housing starts have been mainly above this trend, but have not quite yet made up for the ground lost in the spring. Once the backlog has been made up, we would expect starts to move toward their previous trend level.

Still, it is also possible that rock-bottom interest rates, increased confidence among homebuilders, and price pressures in the resale market will lead to a higher level of construction than we had anticipated pre-pandemic. The demographic fundamentals are certainly a positive factor as the largest segment of millennials is 25-29 years old, just starting to enter the peak phase of household formation. The next few months will be key to see if the construction industry can keep up the current pace.

Thankfully, infections have been trending down. The pace of the vaccine rollout has fallen short of the initial goal, but the country is doing well relative to its advanced economy peers. Regardless of what is achieved in terms of further stimulus from Congress, we expect the U.S. economy will see a much faster pace of growth come the second quarter, as people are able to resume more of their pre-pandemic behaviors.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.