FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

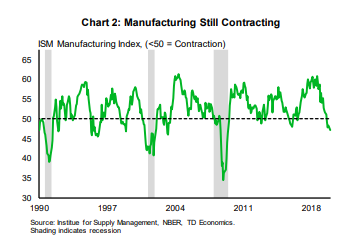

- It was a relatively light week on economic data. The merchandise trade deficit narrowed in November, suggesting some upside risk to real GDP growth in the fourth quarter. Still, activity in the manufacturing sector continues to come in on the weak side, with the ISM index falling again in December to its lowest level since 2009.

- The phase one trade deal between China and the U.S. looks to be signed later this month. Details are still scant and time lines around commitments uncertain.

- News that a U.S. airstrike in Iraq had killed a top Iranian military leader caused oil prices to spike, global stock markets to sell off and bonds to rally on Friday.

A Risk-Filled Start to the Year

Alas, this optimism did not last long. Markets were roiled on Friday by news that a U.S. airstrike in Iraq had killed Qassim Suleimani, a top Iranian military leader. Fears of retaliation and further escalation caused oil prices to spike, global stock markets to sell off and bonds to rally, with the 10-year yield falling seven basis points to 1.81% as of writing.

Outside of the torrid developments in the Middle East, the U.S. and China appear to be moving forward on signing ‘phase one’ of their trade deal. Earlier in the week, President Trump announced that he would sign the deal on January 15th. Details of the final deal are expected in the next several days. Early indications are that the text of the deal could remain vague on the exact amount and timing of China’s commitments to purchase additional agricultural and other U.S. goods for fears that specific details could distort markets.

Elsewhere on the economic front, global manufacturing activity continued to struggle through the end of last year. In the U.S., the ISM manufacturing index fell to 47.2 in December from 48.1 in November. The decline was contrary to the median economist forecast for an increase in the index. The ISM index has now been in contractionary territory for five consecutive months and at its lowest point since the recession in 2009. Manufacturing sectors remain weak the world over. The Markit PMI index in Germany edged lower in December as well. While still above its trough, it remains in contractionary territory where it has been through all of 2019.

The data flow will pick up next week with the release of the ISM non-manufacturing index and December employment data. So far, the troubles in the manufacturing sector have remained contained therein while broader services expansion has remained unharmed and, importantly, has provided enough support to the job market to support ongoing consumer spending. We will be watching for any developments on this front in the jobs data next week, as well as the impact of new (and old) geopolitical flare ups.

James Marple, Senior Economist | 416-982-2557

Financial News- January 3, 2020

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.