HIGHLIGHTS OF THE WEEK

- The New Year came with baggage from the old for thousands of federal employees caught in the middle of a budget tug-of-war between Congress and the White House that has led to a partial government shutdown.

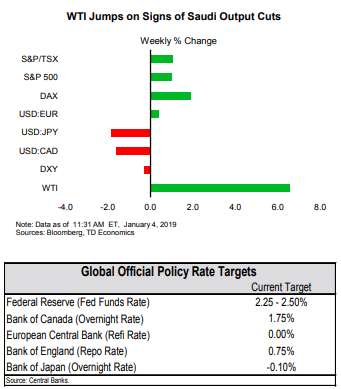

- The volatility in stock markets continued early in the week as a slew of weaker-than-expected economic data and signs of a slowing China roused investor concerns that global growth may be slowing faster than expected.

- Fortunately, a strong payrolls tally lifted investors’ spirits by week’s end. Employment rose 312k and the unemployment rate edged up to 3.9% as more people joined the workforce. Hourly earnings growth also topped 3% (year-on-year) for a third consecutive month.

The Shutdown Slowdown

Set to enter its third week, the shutdown is expected to negatively impact consumer spending and business activity. Assuming it ends soon, it is projected to lower first quarter GDP growth by 0.1 percentage points. Once resolved, federal employees will receive back pay, (though workers on contract will not), and this should boost economic activity in the second quarter. The question that remains is how long it will last. The longest government shutdown was for 21 days in 1995 (Chart 1), but workers and businesses who depend on their spending, are hopeful that such a scenario will not be repeated.

By the end of the week, a nod to “patience” by Fed Chair Powell and a strong December jobs report helped pull equity markets back into positive territory. Non-farm payrolls exceeded expectations, adding 312K jobs in December. This resulted in 99 straight months of expanding payrolls – the longest stretch on record. Even the uptick in the unemployment rate to 3.9% resulted from a labor force rising participation rate. Such dynamics suggest that even amid the tightest labor market in decades, the U.S. economy is still able to pull workers off the sideline and into the job mix. Wages also surprised to the upside, growing by 3.2% year-on-year (Chart 2) – the best full-year gain since 2008.

The employment data should serve to calm concerns that the American economy is quickly running out of steam. While growth in 2019 is projected to be lower (see forecast), we still expect it to remain above the economy’s trend pace. All in all, government showdowns aside, consumers remain on firm footing, supported by the most favorable labor market in decades.

Shernette McLeod, Economist | 416-415 0413

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.